of

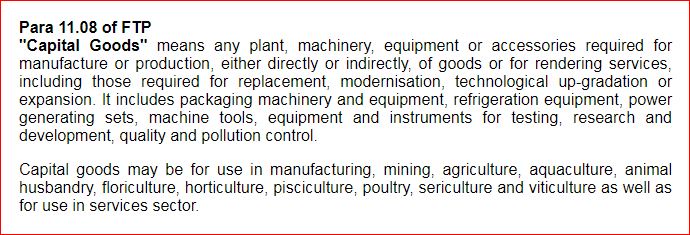

capital goods

of

capital goods

for producing quality goods and

services

for producing quality goods and

services

and enhance India’s manufacturing competitiveness.

and enhance India’s manufacturing competitiveness.Foreign Trade Policy 2023

CHAPTER 5

Export Promotion Capital Goods (EPCG) Scheme

(Relevant Procedure Chapter 5)

5.00 Objective

The objective of the EPCG Scheme is to facilitate

import

of

capital goods

for producing quality goods and

services

and enhance India’s manufacturing competitiveness.

*5.01 EPCG Scheme

(a)

EPCG Scheme allows import of capital goods (except those

specified

in negative list in

Appendix 5 F) for pre- production, production and post-production at zero customs duty. Capital goods imported under EPCG Authorisation for physical exports are also exempt from IGST and Compensation Cess, leviable thereon under the subsection (7) and subsection (9) respectively, of

section 3 of the Customs Tariff Act, 1975 (51 of 1975), as provided in the notification issued by Department of Revenue. Alternatively, the

Authorisation

in negative list in

Appendix 5 F) for pre- production, production and post-production at zero customs duty. Capital goods imported under EPCG Authorisation for physical exports are also exempt from IGST and Compensation Cess, leviable thereon under the subsection (7) and subsection (9) respectively, of

section 3 of the Customs Tariff Act, 1975 (51 of 1975), as provided in the notification issued by Department of Revenue. Alternatively, the

Authorisation

holder may also procure Capital Goods from indigenous sources in accordance with provisions of paragraph 5.07 of FTP. Capital goods

for the purpose of the EPCG

scheme shall include:

holder may also procure Capital Goods from indigenous sources in accordance with provisions of paragraph 5.07 of FTP. Capital goods

for the purpose of the EPCG

scheme shall include:

(i) Capital Goods as defined in Chapter 11 including in CKD/SKD condition thereof;

(ii)

Computer systems and software which are a

part

of the Capital Goods being imported;

of the Capital Goods being imported;

*(iii)

Spares

, moulds, dies, jigs, fixtures, tools & refractories; and

, moulds, dies, jigs, fixtures, tools & refractories; and

*(iv) Catalysts for initial charge plus one subsequent charge.

(b)

Import under EPCG Scheme shall be subject to an

Export Obligation

(EO) equivalent to 6 times of duties, taxes and cess saved on capital goods, to be fulfilled in 6 years reckoned from date of issue of Authorisation.

(EO) equivalent to 6 times of duties, taxes and cess saved on capital goods, to be fulfilled in 6 years reckoned from date of issue of Authorisation.

*(c) Import/procurement under EPCG scheme shall also be subjected to Average Export Obligation (AEO) as given in para 5.04(c) of FTP.

(d) Authorisation shall be valid for import for 24 months from the date of issue of Authorisation. Revalidation of EPCG Authorisation shall not be permitted.

*(e) In case Integrated Tax and Compensation Cess are paid in cash on imports under EPCG, incidence of the said Integrated Tax and Compensation Cess would not be taken for computation of net duty saved provided Input Tax Credit is not availed.

(f)

Import of items which are

restricted

for import shall be permitted under EPCG Scheme only after approval from Exim Facilitation Committee (EFC) at DGFT Headquarters.

for import shall be permitted under EPCG Scheme only after approval from Exim Facilitation Committee (EFC) at DGFT Headquarters.

(g)

If the goods proposed to be exported under EPCG Authorisation are restricted for

export

, the EPCG Authorisation shall be issued only after approval for issuance of Export Authorisation from Exim Facilitation Committee (EFC) at DGFT Headquarters.

, the EPCG Authorisation shall be issued only after approval for issuance of Export Authorisation from Exim Facilitation Committee (EFC) at DGFT Headquarters.

*5.02 Coverage

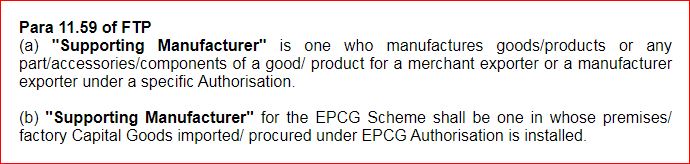

(a)

EPCG scheme covers

manufacturer exporters

with or without

supporting manufacturer

with or without

supporting manufacturer

(s),

merchant exporters

(s),

merchant exporters

tied to supporting manufacturer(s) and

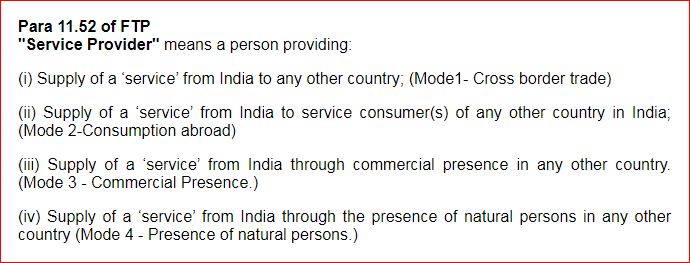

service providers

tied to supporting manufacturer(s) and

service providers

. Name of supporting manufacturer(s)

shall

be

endorsed

on

the

EPCG

Authorisation

before installation of the

capital goods

in the factory /

premises of the supporting manufacturer(s). In case of any change in supporting manufacturer(s), the

RARegional Authority shall intimate such change to jurisdictional Customs Authority of existing as well as changed supporting manufacturer(s) and the Customs at port of registration of Authorisation.

. Name of supporting manufacturer(s)

shall

be

endorsed

on

the

EPCG

Authorisation

before installation of the

capital goods

in the factory /

premises of the supporting manufacturer(s). In case of any change in supporting manufacturer(s), the

RARegional Authority shall intimate such change to jurisdictional Customs Authority of existing as well as changed supporting manufacturer(s) and the Customs at port of registration of Authorisation.

(b) Export Promotion Capital Goods (EPCG) Scheme also covers a service provider who is certified as a Common Service Provider (CSP) by the DGFT - HQs, Department of Commerce in a Town of Export Excellence or Prime Minister Mega Integrated Textile Region and Apparel Parks (PM MITRA) subject to provisions of Foreign Trade Policy/Handbook of Procedures with the following conditions:

(i) Common utility services like providing Electricity, Water, Gas, Sanitation, Sewerage, Telecommunication, Transportation etc. shall not considered for benefit of CSP;

(ii) Export by users of the common service shall be counted towards fulfillment of EO of the CSP provided the EPCG Authorisation details of the CSP is mentioned in the respective Shipping bills and concerned RA must be informed about the details of the users prior to such export;

(iii) Such export will not count towards fulfillment of specific export obligation in respect of other EPCG Authorisations of the user;

(iv)

Authorisation

holder shall be required to submit Bank Guarantee (BG) which shall be equivalent to the duty saved. BG can be given by CSP or by any one of the users or a combination thereof, at the option of the

CSPCommon Service Provider; and

(v) Capital goods shall be installed within a Town of Export Excellence or PM MITRA.

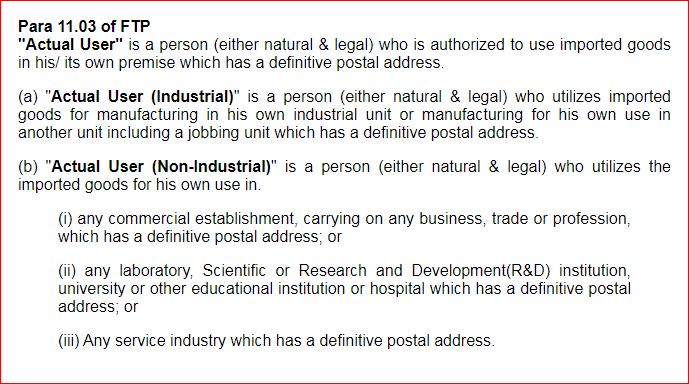

5.03

Actual User

Condition

Condition

Imported capital goods shall be subject to Actual User condition till export obligation is completed and Export Obligation Discharge Certificate (EODC) is granted.

5.04

Export obligation

Following conditions shall apply to the fulfillment of Export obligation:-

(a)

Export obligation shall be fulfilled by the Authorisation holder through export of goods which are manufactured by him or his

supporting manufacturer

/

services

rendered by him, for which the EPCG authorisation has been granted.

*(b) For export of goods, EPCG Authorisation holder may export either directly or through third party(ies).

*(c)

EOExport Obligation under the scheme shall be, over and above, the average level of exports achieved by the

applicant

in the preceding three

licensing years

in the preceding three

licensing years

for the same and similar products within the overall EO period including extended period, if any; except for categories mentioned in paragraph 5.12(a). Such average would be the arithmetic mean of export performance in the preceding three licensing years for same and similar products. The Average Export Obligation (AEO) shall be fulfilled every financial year, till export obligation is completed. Exports/supplies made over and above AEO shall only be considered for fulfillment of Export Obligation.

for the same and similar products within the overall EO period including extended period, if any; except for categories mentioned in paragraph 5.12(a). Such average would be the arithmetic mean of export performance in the preceding three licensing years for same and similar products. The Average Export Obligation (AEO) shall be fulfilled every financial year, till export obligation is completed. Exports/supplies made over and above AEO shall only be considered for fulfillment of Export Obligation.

*(d)

In case of indigenous sourcing of

Capital Goods

, specific EO shall be 25% less than the EO stipulated in Para 5.01. There shall be no change in average EO imposed, if any, as stipulated in Para 5.04(c).

(e)

Exports

under Advance Authorisation,

DFIADuty Free Import

Authorisation, Duty Drawback, RoSCTL and RoDTEP Schemes would also be eligible for fulfilment of EO under EPCG Scheme.

(f)

Export obligation may be fulfilled both by physical exports as well as

deemed exports

. Deemed export supplies shall also be eligible for benefits available under

paragraph 7.03 of FTP.

. Deemed export supplies shall also be eligible for benefits available under

paragraph 7.03 of FTP.

*(g) Exports made from DTA units shall only be counted for calculation and/or fulfillment of AEO and/or EO.

(h)

EO can also be fulfilled by the supply of ITA-I items to provided under GST Rules under the category of deemed

DTA,

provided realization is in

free

foreign exchange.

foreign exchange.

(i) Royalty payments received by the Authorisation holder in freely convertible currency and foreign exchange received for R&D services shall also be counted for discharge under EPCG.

*(j) Payment received in rupee terms for such Services as notified in Appendix 5D shall also be counted towards discharge of export obligation under the EPCG scheme.

*(k) Export proceeds realized in Indian Rupees as per para 2.52(d)(ii) are also counted towards fulfillment of export obligation.

(l) Only one benefit specified in paras 5.04(d), 5.09, 5.10 and 5.11 shall be admissible.

*(m) Extension of EO period shall be permitted as prescribed in Handbook of Procedures.

5.05 Provision for companies admitted under the provisions of Insolvency and Bankruptcy Code 2016

A company holding EPCG authorizations and having been admitted under the provisions of Insolvency and Bankruptcy Code 2016 for commencement of insolvency proceedings and in respect of whom the resolution plan has been approved under Section 31 of IBC 2016 by Adjudicating Authority may be permitted to relief, concessions and waivers in accordance with the resolution plan approved/ finalised by Adjudicating Authority/Appellate Authorities as the case may be.

5.06 LUTLegal Undertaking/Bond/BG in case of Agro units

LUT/Bond or 15% BG, as applicable, may be furnished for EPCG Authorisation granted to units in Agri-Export Zones provided EPCG Authorisation is taken for export of primary agricultural product(s) notified or their value added variants.

*5.07 Indigenous Sourcing of Capital Goods and benefits to Domestic Supplier

A

person

holding an EPCG Authorisation may

source capital goods from a

domestic manufacturer either through Invalidation Letter or through Advance Release

Order. Such

domestic manufacturer shall be eligible for

deemed export

benefits under

paragraph 7.03 of FTP, and as may be provided under GST Rules under the category

of deemed exports. Such domestic sourcing shall also be permitted from

EOU

holding an EPCG Authorisation may

source capital goods from a

domestic manufacturer either through Invalidation Letter or through Advance Release

Order. Such

domestic manufacturer shall be eligible for

deemed export

benefits under

paragraph 7.03 of FTP, and as may be provided under GST Rules under the category

of deemed exports. Such domestic sourcing shall also be permitted from

EOU

s and

these supplies shall be counted for purpose of fulfillment of positive

NFENet Foreign Exchange by

said EOU as provided in Para 6.08 (a) of FTP.

s and

these supplies shall be counted for purpose of fulfillment of positive

NFENet Foreign Exchange by

said EOU as provided in Para 6.08 (a) of FTP.

5.08 Calculation of

Export Obligation

In case of direct

imports

,

EOExport Obligation shall be

reckoned with reference to actual

duty /Taxes/Cess saved amount. In case of domestic sourcing, EO shall be reckoned with reference to notional Customs duty /Taxes/Cess saved on

FORFreight on Road and Rails value as indicated in

AROAdvance Release Order / Invalidation letter.

*5.09 Incentive for early EO fulfillment

With a view to accelerating

exports

, in cases

where

Authorisation

holder has

fulfilled 75% or more of specific

export obligation and 100% of Average Export Obligation till date, if any, in half or less than half the original export obligation period

specified

, remaining export obligation shall be condoned and the Authorisation redeemed by

RARegional Authority concerned.

*5.10 Reduced EO for Green Technology Products

For

exporters

of Green Technology Products,

Specific EO shall

be 75% of EO as stipulated in Para 5.01(b). There shall be no change in average EO imposed, if any, as stipulated in Para 5.04(c). The list of Green Technology Products is given in

Para 5.26 of HBP.

of Green Technology Products,

Specific EO shall

be 75% of EO as stipulated in Para 5.01(b). There shall be no change in average EO imposed, if any, as stipulated in Para 5.04(c). The list of Green Technology Products is given in

Para 5.26 of HBP.

5.11 Reduced EO for North East Region and UTs of Jammu & Kashmir and Ladakh.

For manufacturing units located in Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Jammu & Kashmir and Ladakh, specific EO shall be 25% of the EO, as stipulated in Para 5.01(b). There shall be no change in average EO imposed, if any, as stipulated in Para 5.04(c).

*5.12 Exemption from maintenance of average export obligation

(a) In case of export of goods relating to the following, the EPCG Authorisation holder shall not be required to maintain average export obligation.

(i) Handicrafts, (ii) Handlooms, (iii) Industries covered under Khadi and Village Industries Commission (KVIC) (iv) Agriculture (v) Aquaculture (including Fisheries),Pisciculture, (vi) Animal husbandry and Dairying, (vii) Floriculture & Horticulture, (viii) Poultry, (ix) Viticulture, (x) Sericulture, (xi) Carpets, (xii) Coir, and (xiii) Jute

(b)

However, this exemption from maintenance of average export obligation shall not be allowed for import of fishing trawlers, boats,

ships

and other similar items.

and other similar items.

(c) Goods, excepting tools imported under EPCG scheme\

by sectors specified in sub-paragraph (a) above, shall not be allowed to be transferred for a period of five years from date of imports even in cases where export obligation has been fulfilled.

5.13 Transitional Arrangements:

Authorisations issued during various policy periods viz., 2002-07, 2004-09, 2009-14, 2015-20 issued prior to 05.12.2017 and 2015-20 RE 2017 shall be governed by corresponding Foreign Trade Policy provisions and Handbook of Procedures, unless otherwise specifically stated.