Foreign Trade Policy 2023

CHAPTER 6

Export Oriented Units (EOUs), Electronics Hardware Technology

Parks (EHTPs), Software

Technology Parks (STPs) and Bio-Technology Parks (BTPs)

(Relevant Procedure Chapter

6)

*6.00

Introduction and Objective

(a) Units undertaking to export their entire production of goods and

services

(except permissible sales in DTA), may be set up under the Export

Oriented Unit (EOU) Scheme, Electronics Hardware Technology Park (EHTP) Scheme,

Software Technology Park(STP) Scheme or Bio-Technology Park (BTP) Scheme for

manufacture

(except permissible sales in DTA), may be set up under the Export

Oriented Unit (EOU) Scheme, Electronics Hardware Technology Park (EHTP) Scheme,

Software Technology Park(STP) Scheme or Bio-Technology Park (BTP) Scheme for

manufacture

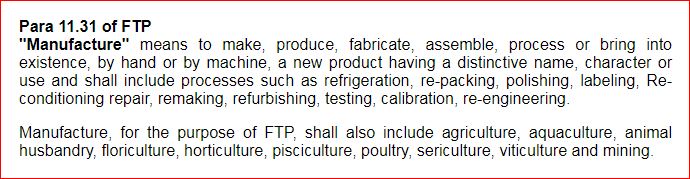

of goods, including repair, re-making, reconditioning, re-

engineering, rendering of services, development of software, agriculture

including agro-processing, aquaculture, animal husbandry, bio-technology,

floriculture, horticulture, pisciculture, viticulture, poultry and sericulture.

Trading units are not covered under these schemes.

of goods, including repair, re-making, reconditioning, re-

engineering, rendering of services, development of software, agriculture

including agro-processing, aquaculture, animal husbandry, bio-technology,

floriculture, horticulture, pisciculture, viticulture, poultry and sericulture.

Trading units are not covered under these schemes.

(b) Objectives of these schemes are to promote exports, enhance foreign

exchange earnings, attract investment for export production and employment

generation.

*6.01

Export

and

Import

and

Import

of Goods

of Goods

(a) An

EOU

/ EHTP / STP / BTP unit may export all kinds of goods and

services except items that are

prohibited

/ EHTP / STP / BTP unit may export all kinds of goods and

services except items that are

prohibited

in ITC (HS). However export of gold jewellery, including partly processed jewellery, whether plain or studded, and

articles, containing gold of 8 carats and above up to a maximum limit of 22

carats only shall be permitted. The export of findings like posts, push backs,

locks which help in collating the jewellery pieces together, containing gold of

3 carats and above up to a maximum limit of 22 carats only shall be allowed.

in ITC (HS). However export of gold jewellery, including partly processed jewellery, whether plain or studded, and

articles, containing gold of 8 carats and above up to a maximum limit of 22

carats only shall be permitted. The export of findings like posts, push backs,

locks which help in collating the jewellery pieces together, containing gold of

3 carats and above up to a maximum limit of 22 carats only shall be allowed.

(b) Export of

Special Chemicals, Organisms, Materials, Equipment and

Technologies (SCOMET)

shall be subject to fulfillment of conditions contained in

the Chapter 10 of the FTP (new Chapter for SCOMET). In respect of an EOU,

permission to export prohibited item(s) may be considered by

BOABoard of Approval on a case to

case basis, provided the input(s) used for the export item(s) is/are imported

and there is no procurement of such inputs from DTA.

shall be subject to fulfillment of conditions contained in

the Chapter 10 of the FTP (new Chapter for SCOMET). In respect of an EOU,

permission to export prohibited item(s) may be considered by

BOABoard of Approval on a case to

case basis, provided the input(s) used for the export item(s) is/are imported

and there is no procurement of such inputs from DTA.

(c) Procurement and supply of export promotion material like

brochure/literature, pamphlets, hoardings, catalogues, posters etc. upto a

maximum value limit of 1.5% of FOB value of previous year’s exports shall

also be allowed.

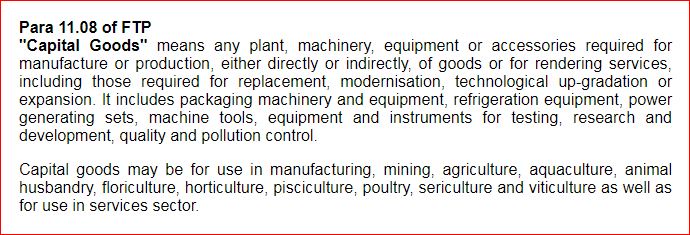

(d) (i) An EOU / EHTP/ STP/ BTP unit may import and / or procure, from

DTA or bonded warehouses in DTA / international exhibition held in India,

all types of goods, including

capital goods

, required for its activities,

provided they are not prohibited items of import in the ITC (HS) subject to

conditions given at para (ii) & (iii) below. Any permission required for import under any other law shall

be applicable. Units shall also be permitted to import goods including

capital goods required for approved activity,

free

, required for its activities,

provided they are not prohibited items of import in the ITC (HS) subject to

conditions given at para (ii) & (iii) below. Any permission required for import under any other law shall

be applicable. Units shall also be permitted to import goods including

capital goods required for approved activity,

free

of cost or on loan /

lease from clients. Import of capital goods will be on a self-certification

basis. Goods imported by a unit shall be with

actual user

of cost or on loan /

lease from clients. Import of capital goods will be on a self-certification

basis. Goods imported by a unit shall be with

actual user

condition and

shall be utilized for export production.

condition and

shall be utilized for export production.

(ii) The imports and/ or procurement from bonded warehouse in DTA or

from international exhibition held in India shall be without payment of duty

of customs leviable thereon under the First Schedule to the Customs Tariff

Act, 1975 and additional duty, if any, leviable thereon under

Section 3(1),

3(3) and 3(5) of the said Customs Tariff Act. Such imports and/ or

procurements shall be made without payment of integrated tax and

compensation cess leviable thereon under

section 3(7) and

3(9) of the

Customs Tariff Act, 1975 as per notification issued by the Department of

Revenue.

(iii) The procurement of goods covered under GST from

DTA would be on

payment of applicable GST and compensation cess. The refund of GST paid on

such supply from DTA to

EOUExport Oriented Unit would be available to the supplier subject to

such conditions and documentations as

Specified

under GST rules and

notifications issued there under. EOUs can also procure

excisable goods

under GST rules and

notifications issued there under. EOUs can also procure

excisable goods

falling under the Fourth Schedule of Central Excise Act, 1944 from DTA

without payment of applicable duty of excise.

falling under the Fourth Schedule of Central Excise Act, 1944 from DTA

without payment of applicable duty of excise.

(e) State Trading regime shall not apply to EOU manufacturing units.

However, in respect of Chrome Ore/Chrome concentrate, State Trading Regime as stipulated in export

policy of these items will be applicable to EOUs.

(f) EOU/EHTPElectronic Hardware

Technology Park/STP/BTPBiotechnology Park units may import/procure from DTA, with or without

payment of duties/taxes as provided at Para 6.01 (d) (ii) and 6.01(d) (iii)

above, certain specified goods for creating a central facility. Software EOU/DTA

units may use such facility for export of software.

(g) An EOU engaged in agriculture, animal husbandry, aquaculture,

floriculture, horticulture, pisciculture, viticulture, poultry or

sericulture may be permitted to remove specified goods in connection with

its activities for use outside the premises of the unit.

(h) Gems and jewellery EOUs may source gold / silver / platinum through nominated agencies on loan / outright purchase basis.

Units obtaining gold / silver / platinum from nominated agencies, either on loan basis or outright

purchase basis shall export gold / silver / platinum within 90 days from

date of release of such metals by the nominated agencies.

(i) EOU/EHTP/STP/BTP units, other than service units, may export to

Russian Federation in Indian Rupees against repayment of State Credit/

Escrow Rupee Account of buyer subject to RBI clearance, if any.

(j) Procurement and export of

spares

/

components

/

components

, upto 5% of

FOB

value of exports, may be allowed to same consignee / buyer of the export

article, subject to the condition that it shall not count for

NFENet Foreign Exchange and direct

tax benefits.

, upto 5% of

FOB

value of exports, may be allowed to same consignee / buyer of the export

article, subject to the condition that it shall not count for

NFENet Foreign Exchange and direct

tax benefits.

(k)

Development Commissioner

/Designated Officer in

EOU

/EHTP/STP/BTP

units may allow, on a case to case basis, EOU / EHTP / STP/ BTP units in

sectors other than Gems & Jewellery, for consolidation of goods related to

manufactured articles and export thereof along with manufactured article.

Such goods may be allowed to be imported / procured from DTA by EOU with or

without payment of duty and/ or taxes as provided at Para 6.01(d) (ii) and

(iii) above, as the case may be to the extent of 5% FOB value of such

manufactured articles exported by the unit in preceding financial year.

Details of procured / imported goods and articles manufactured by the EOU will be listed

separately in the export documents. In such cases, value of procured /

imported goods will not be taken into account for calculation of NFE and DTA

sale entitlement. Such procured / imported goods shall not be allowed to be sold in DTA. Development Commissioner

/Designated Officer may also specify any other conditions.

/Designated Officer in

EOU

/EHTP/STP/BTP

units may allow, on a case to case basis, EOU / EHTP / STP/ BTP units in

sectors other than Gems & Jewellery, for consolidation of goods related to

manufactured articles and export thereof along with manufactured article.

Such goods may be allowed to be imported / procured from DTA by EOU with or

without payment of duty and/ or taxes as provided at Para 6.01(d) (ii) and

(iii) above, as the case may be to the extent of 5% FOB value of such

manufactured articles exported by the unit in preceding financial year.

Details of procured / imported goods and articles manufactured by the EOU will be listed

separately in the export documents. In such cases, value of procured /

imported goods will not be taken into account for calculation of NFE and DTA

sale entitlement. Such procured / imported goods shall not be allowed to be sold in DTA. Development Commissioner

/Designated Officer may also specify any other conditions.

6.02

Second hand

Capital Goods

Second hand capital goods, without any age limit, may also be imported

with or without payment of duty/ taxes as provided under Para 6.01(d)(ii) above.

6.03

Leasing of Capital Goods

(a) An

EOUExport Oriented Unit /

EHTP/STP/BTP unit may, on the basis of a

firm contract between parties, source capital goods from a domestic / foreign

leasing company with or without payment of duties/taxes as provided at Para 6.01 (d) (ii) and (iii) above, as the case may be in such a case, EOU /

EHTP/STP/BTP unit and domestic / foreign leasing company shall jointly file documents to enable

import

/

procurement of capital goods.

(b) An EOU/ EHTP/STP/BTP unit may sell capital goods and lease back the

same from a Non Banking Financial Company (NBFC), subject to the following

conditions:

(i) The unit should obtain permission from the jurisdictional

Deputy/Assistant Commissioner of Customs for entering into transaction of ‘Sale

and Lease Back of Assets’, and submit full details of the goods to be sold and

leased back and the details of NBFC;

(ii) The goods sold and leased back shall not be removed from the unit’s

premises;

(iii) The unit should be NFE positive at the time when it enters into

sale and lease back transaction with NBFC;

(iv) A joint undertaking by the unit and NBFC should be given to pay duty

on goods in case of violation or contravention of any provision of the

notification under which these goods were imported or procured, read with

Customs Act, 1962 or Central Excise Act, 1944, and that the lien on the goods

shall remain with the Customs Department, which will have first charge over the

said goods for recovery of sum due from the unit to Government under provision

of Section 142(b) of the Customs Act, 1962 read with the Customs (Attachment of

Property of Defaulters for Recovery of Govt. Dues) Rules, 1995.

6.04 Net Foreign Exchange Earnings

EOU/EHTP/STP/BTPBiotechnology Park unit shall be a positive net foreign exchange earner. In

addition sector specific provision of Appendix 6B of Appendices &

ANFs, where a

higher value addition and other conditions are given, shall be required to be

followed.

NFENet Foreign Exchange Earnings shall be calculated cumulatively in blocks of five years,

starting from commencement of production. Whenever a unit is unable to achieve

NFE due to prohibition / restriction imposed on

export

of any product mentioned

in

LoPLetter of Permit, the five year block period for calculation of NFE earnings may be

suitably extended by

BoABoard of Approval. Further, wherever a unit is unable to achieve NFE due

to adverse market condition or any grounds of genuine hardship having adverse

impact on functioning of the unit, the five year block period for calculation of

NFE earnings may be extended by BoA for a period of upto one year, on a case to

case basis. The method of calculation of NFE in detail is given in

para 6.10 of

current Handbook of Procedures.

6.05

Applications & Approvals/Letter of Permission / Letter of Intent and Legal

Undertaking

(a) (i) Application for setting up an

EOU shall be considered by Unit

Approval Committee (UAC)/ Board of Approval (BoA) as the case may be, as

detailed in the Hand Book of Procedure. The powers of

DCDevelopment Commissioner are defined in

para

6.34 of HBP.

(ii) In case of units under

EHTPElectronic Hardware

Technology Park / STP schemes, necessary approval /

permission under relevant paras of this Chapter shall be granted by officer

designated by Ministry of Electronics & Information Technology, instead of DC,

and by Inter- Ministerial Standing Committee (IMSC) instead of BOA.

(iii) Bio-Technology Parks (BTP) would be notified by

DGFT on

recommendations of Department of Biotechnology. In case of units in BTP,

necessary approval / permission under relevant provisions of this chapter will

be granted by designated officer of Department of Biotechnology.

(iv) On approval, a Letter of Permission (LoP) / Letter of Intent (LoI)

shall be issued by DC / Designated officer to EOU/EHTP/STP/BTP unit. The

validity of LoP/LoI shall be given in the Hand Book of Procedures.

(b) LoP / LoI issued to EOU/EHTP/STP/BTP units by concerned authority, subject to compliance of provision in Para 6.01

above, would be construed as an

Authorisation

for all purposes.

for all purposes.

(c) Unit shall execute an

LUTLegal Undertaking with DC concerned. Failure to ensure

positive NFE or to abide by any of the terms and conditions of LoP / LoI /

ILIndustrial Licensing / LUT shall render the unit liable to penal action under provisions of

the FT (D&R) Act, as amended, and Rules and

Orders

made thereunder, without

prejudice to action under any other law / rules and cancellation or

revocation of LoP/IL.

made thereunder, without

prejudice to action under any other law / rules and cancellation or

revocation of LoP/IL.

6.06

Investment Criteria

Only projects having a minimum investment of Rs.1 Crore in plant &

machinery shall be considered for establishment as EOUs. However, this shall

not apply to existing units, units in EHTP / STP/

BTPBiotechnology Park, and EOUs in

Handicrafts/Agriculture/ Floriculture/Aquaculture/Animal

Husbandry/Information Technology,

Services

, Brass Hardware and Handmade jewellery sectors. BoA may allow establishment of EOUs with a lower

investment criteria.

6.07

DTA Sale of Finished Products/Rejects/ Waste/Scrap/Remnants and

By- products

Entire production of EOU/EHTP/STP/BTP units shall be exported. However,

the following are allowed as exceptions subject to the conditions

specified

.

(a) (i) Units, other than those of gems and jewellery may sell finished

goods manufactured by them as specified in

LoPLetter of Permit (including by-products,

rejects, waste and scraps arising in the course of production,

manufacture

,

processing or packaging of such goods) which are freely importable under FTP

in DTA, subject to fulfillment of positive

NFENet Foreign Exchange, on payment of excise duty,

if applicable, and/ or payment of GST and compensation cess along with

reversal of duties of Custom leviable under First Schedule to the Customs

Tariff Act, 1975 availed as exemption, if any on the inputs utilized for the

purpose of manufacturing of such finished goods (including by-products,

rejects, waste and scraps arising in the course of production, manufacture,

processing or packaging of such goods). No DTA sale shall be permissible in

respect of, pepper & pepper products, marble and such other items as may

notified from time to time. This reversal of Customs Duty would be as per prevailing SION norms or norms fixed by Norms

Committee (where no SION norms are fixed).

(ii) Such DTA sale shall also not be permissible to units engaged in

activities of packaging / labeling / segregation / refrigeration / compacting / micronisation / pulverization

/ granulation / conversion of monohydrate form of chemical to anhydrous form

or vice-versa.

(iii) Sales made to a unit in SEZ shall also be taken into account for

purpose of arriving at FOB value of

export

by

EOUExport Oriented Unit provided payment for such

sales are made from Foreign Currency Account of SEZ unit. Sale to DTA would

also be subject to mandatory requirement of registration of pharmaceutical

products (including bulk drugs).

(iv) An amount equal to Anti Dumping duty under

section 9A of the

Customs Tariff Act, 1975 leviable at the time of

import

, shall be payable on

the goods used for the purpose of manufacture or processing of the goods

cleared into DTA from the unit.

(v) Such DTA sale shall also be subject to refund of any benefits

under Chapter 7 of FTP availed by the

EOU

/supplier as per FTP, on the goods

used for manufacture of the goods cleared into the DTA.

(b) For services, including software units, sale in DTA in any mode,

including on line data communication, shall also be permissible up to 50% of

FOB value of exports and /or 50% of foreign exchange earned, where payment

of such services is received in foreign exchange. However, sale in DTA in

respect of services classified under Chapter Heading 9988 and 9989 under

GST, but covered in LOP/para 11.31 of FTP as manufacturing of goods, will

continue to be covered under para 6.07(a) above. At the time of DTA

clearance, applicable GST and compensation cess as per GST classification

would apply.

(c) Gems and jewellery units may sell upto 10% of FOB value of exports

of the preceding year in DTA, subject to fulfillment of positive NFE. The

unit shall pay applicable GST and compensation cess along with reversal of

duties of Customs leviable under First Schedule of the Customs Tariff Act,

1975 availed as exemption, on inputs used in such jewellery.

(d) Unless specifically

prohibited

in

LoPLetter of Permit, rejects may be sold in DTA on payment of excise duty, if applicable, and/or payment of

GST and compensation cess along with reversal of duties of Customs leviable

under First Schedule of the Customs Tariff Act, 1975 availed as exemption on

inputs on prior intimation to Customs authorities. Sale of rejects upto 5%

of FOB value of exports shall not be subject to achievement of

NFENet Foreign Exchange.

(e) Scrap / waste / remnants arising out of production process or in

connection therewith may be sold in DTA, as per SION notified under Duty

Exemption Scheme, on payment of applicable duties and/ or taxes and

compensation cess. Such sales of scrap / waste / remnants shall not be

subject to achievement of positive NFE. In respect of items not covered by

norms,

DCDevelopment Commissioner may fix ad- hoc norms for a period of six months and within this

period, norms should be fixed by Norms Committee. Ad-hoc norms will continue

till such time norms are fixed by Norms Committee. Scrap

/ waste / remnants may also be exported.

(f) There shall be no duties / taxes on scrap / waste / remnants, in

case same are destroyed with permission of Customs authorities. The

expression “no duties/ taxes” shall not include applicable taxes and cess

under the GST laws.

(g) By-products included in LoP may also be sold in DTA subject to

achievement of positive NFE, on payment of excise duty, if applicable,

and/or payment of GST and compensation cess along with reversal of duties of

Custom leviable under First Schedule to the Customs Tariff Act, 1975, if

availed on inputs.

(h) In case of units manufacturing electronics hardware and software,

NFE and DTA sale entitlement shall be reckoned separately for hardware and

software.

(i) In case of new EOUs, advance DTA sale will be allowed not

exceeding 50% of its estimated exports for first year, except pharmaceutical

units where this will be based on its estimated exports for first two years.

(j) Procurement of

spares

/

components

, up to 2% of the value of

manufactured articles, cleared into DTA, during the preceding year, may be

allowed for supply to the same consignee / buyer for the purpose of

after-sale-service. The same can be cleared in DTA on payment of applicable

GST and compensation cess along with reversal of duties of Customs leviable

under First Schedule of the Customs Tariff Act, 1975 availed as exemption if

any.

1[(k) Exemption from applicability of mandatory Quality Control Orders (QCOs)

issued under the BIS Act, 2016, shall be provided to EOU on import of inputs

which are required for export production. An undertaking to that effect will be

submitted to the Customs authorities by the EOU at the time of importation and a

copy of the same shall also be submitted to the Development Commissioner

concerned. No DTA clearance of such inputs or goods manufactured made out of

such inputs, are allowed. The exemption from QCO will be available for physical

exports only and such exemption will not be allowed for deemed exports. This

exemption is further subjected to para 2.03 (c) of FTP."]

6.08 Other Supplies counted for fulfilment

of NFE

Following supplies effected from

EOU /

EHTPElectronic Hardware

Technology Park / STP /

BTPBiotechnology Park units will be

counted for fulfillment of positive NFE. Such supplies shall not include

“marble”, except if such supply of marble is an inter unit supply as

provided at Sub-Para(c) below:

(a) Supplies effected in

DTA to holders of Advance Authorization /

Advance Authorization for annual requirement /

DFIADuty Free Import

Authorisation under duty exemption /

remission scheme / EPCG scheme. However, printing sector EOUs (or any other

sector that may be notified in HBP), can’t supply goods, where basic customs

duty and CVD is nil or exempted otherwise, to holders of Advance

Authorization / Advance Authorization for annual requirement.

(b) Supplies effected in DTA against foreign exchange remittance

received from overseas.

(c) Supplies to other

EOU

/ EHTP / STP / BTP / SEZ units, provided

that such goods are permissible for procurement in terms of Para 6.01 of

FTP.

(d) Supplies made to bonded warehouses set up under FTP and / or under

section 65 of Customs Act and

free

trade and warehousing zones, where

payment is received in foreign exchange.

(e) Supplies of goods and

services

to such organizations which are

entitled for duty free import of such items in terms of general exemption

notification issued by

MoFMinistry of Finance, as may be provided in HBP.

(f) Supplies of Information Technology Agreement (ITA- 1) items and

notified zero duty telecom / electronics items.

(g) Supplies of items like tags, labels, printed bags, stickers, belts,

buttons or hangers to DTA unit for

export

.

(h) Supply of LPG produced in an EOU refinery to Public Sector

domestic oil companies for being supplied to household domestic consumers at

subsidized prices under the Public Distribution System (PDS) Kerosene and

Domestic LPG Subsidy Scheme, 2002, as notified by the Ministry of Petroleum

and Natural Gas vide notification No. E-20029/18/2001-PP dated 28.01.2003

(hereinafter referred to as PDS Scheme) subject to the following

conditions:-

(i) Only supply of such quantity of LPG would be eligible for which

Ministry of Petroleum and Natural Gas declines permission for export and requires the LPG to be

cleared in DTA; and

(ii) The Ministry of Finance by a notification has

permitted duty free imports of LPG for supply under the aforesaid PDS

Scheme.

6.09

Export through

others

An EOU /EHTPElectronic Hardware

Technology Park/STP/BTP unit may export goods manufactured/ software developed

by it through another

exporter

or any other EOU/EHTP/STP/BTP/SEZ unit

subject to conditions mentioned in Para 6.19 of HBP.

or any other EOU/EHTP/STP/BTP/SEZ unit

subject to conditions mentioned in Para 6.19 of HBP.

6.10

Entitlement for

Supplies from the DTA

(a) Supplies from DTA to EOU/EHTP/STP/

BTPBiotechnology Park units for use in their

manufacture

for exports will be eligible for “benefits under Chapter 7 of

FTP”. DTA supplier shall be eligible for relevant entitlements under chapter

7 of FTP, besides discharge of

export obligation

, if any, on the supplier.

The refund of GST paid on such supply from DTA to EOU would be available to

the supplier subject to such conditions and documentations as

specified

under GST rules and notifications issued there under.

, if any, on the supplier.

The refund of GST paid on such supply from DTA to EOU would be available to

the supplier subject to such conditions and documentations as

specified

under GST rules and notifications issued there under.

(b) Suppliers of precious and semi-precious stones, synthetic stones

and processed pearls from DTA to EOU shall be eligible for grant of

Replenishment Authorizations at rates and for items mentioned in HBP.

(c) In addition, EOU/EHTP/STP/BTP units shall be entitled to following

:-

(i) Reimbursement of Central Sales Tax (CST) on goods manufactured

in India, wherever applicable. Simple interest @ 6% per annum will be

payable on delay in refund of CST, if the case is not settled within 30 days

of receipt of complete application (as in Para 11.10 of HBP).

(ii) Exemption from payment of Central Excise Duty on goods, falling

in Fourth Schedule of Central Excise Act, procured from DTA on such goods

manufactured in India.

6.11

Other

Entitlements

Other entitlements of EOU/EHTP/STP/BTP units are as under:

(a) Exemption from industrial licensing for manufacture of items

reserved for micro and small enterprises.

(b) Export proceeds will be realized within nine months.

(c) Units will be allowed to retain 100% of its export earnings in the

EEFCExchange Earners" Foreign

Currency account.

*(d) Unit will not be required to furnish bank guarantee at the time of

import

or going for job work in DTA, where:

(i) the unit has turnover of Rs. 5 crore or above; and

(ii) the unit is in existence for at least three years; and

(iii) the unit has achieved positive

NFENet Foreign Exchange / export obligation wherever

applicable; and has not been issued a show cause notice or a confirmed

demand, during the preceding 3 years, on grounds other than procedural

violations, under the penal provision of the Customs Act, CGST/ SGST/UTGST//IGST

Acts, the Central Excise Act, the Foreign Trade (Development & Regulation)

Act, 1992, the Foreign Exchange Management Act, the Finance Act, 1994

covering Service Tax or any allied Acts or the rules made thereunder, on

account of fraud / collusion / willful mis- statement / suppression of facts

or contravention of any of the provisions thereof.

(e) Unit will also not be required to furnish bank guarantee at the

time of import or going for job work in DTA, if it has achieved necessary

certification as an Authorised Economic Operator (AEO) and has not been

issued a show cause notice or a confirmed demand, during the preceding 3

years, on grounds other than procedural violations, under the penal

provision of the Foreign Trade (Development & Regulation) Act, 1992 and the

Foreign Exchange Management Act.

(f) 100% FDI investment permitted through automatic route similar to

SEZ units.

(g) The Units Approval Committee may consider on a case-to-case basis

request for sharing of infrastructural facilities among

EOU

s and it shall

forward its recommendation to the Board of Approval for its consideration.

While accepting such proposals, the NFE obligations of the units shall not

be altered. Such facilities will be available to units in

EHTPElectronic Hardware

Technology Park / STP after

getting approval from

IMSCInter-Ministerial Standing

Committee. However, sharing of facilities between EOUs and

SEZ Units shall not be permitted.

6.12

Inter Unit Transfer

(a) Transfer of manufactured goods from one EOU/ EHTP/STP/BTPBiotechnology Park unit to

another EOU / EHTP/ STP/ BTP unit is allowed on payment of applicable GST and compensation cess with

prior intimation to concerned

Development Commissioners

of the transferor

and transferee units as well as concerned Customs authorities, as per

following procedure for movement of goods:

i. The supplier unit shall endorse on usual commercial documents,

such as, tax invoice and delivery challan, the amount of duties of Custom

leviable under First Schedule to the Customs Tariff Act, 1975 availed as

exemption on inputs used in the

manufacture

of such finished goods

(including by- products, rejects, waste and scraps arising in the course of

production, manufacture, processing or packaging of such goods) supplied to

another unit. The recipient unit shall pay such endorsed Customs duty

besides his own liability of reversal of Customs duty as provided in Para

6.07 above, before clearance of such finished goods in DTA and as provided

under

DoRDepartment of Revenue

notifications/ circulars/ guidelines in this regard.

ii. Upon receipt of goods, the recipient unit shall submit endorsed

copies of tax invoice to their jurisdictional Customs authority as well as

to the jurisdictional Customs authorities of the supplier unit.

(b)

Capital goods

may be transferred or given on loan to other EOU/EHTP/STP/BTP/SEZ

units, with prior intimation to concerned

DCDevelopment Commissioner and Customs authorities on

payment of applicable GST and compensation cess. Such transferred goods may

also be returned by the second unit to the original unit in case of

rejection or for any reason on payment of applicable GST and compensation

cess.

(c) Goods supplied by one unit of EOU/EHTP/STP/ BTP to another unit

shall be treated as imported goods for second unit for payment of duty, on

DTA sale by second unit.

(d) In respect of a group of EOUs/EHTPs/STPs/BTP units which source

inputs centrally in

order

to obtain bulk discount and / or reduce cost of

transportation and other logistics cost and / or to maintain effective

supply chain, inter unit transfer of goods and

services

may be permitted on

a case-to-case basis by the Unit Approval Committee. In case inputs so

sourced are imported and then transferred to another unit, then value of the

goods so transferred shall be taken as inflow for the unit transferring these goods and as outflow for the unit

receiving these goods, for the purpose of calculation of

NFENet Foreign Exchange.

6.13

Sub–Contracting

(a) (i) EOU/EHTPElectronic Hardware

Technology Park/STP/BTP units, including gems and jewellery units, may be

on the basis of annual permission from Customs authorities, sub- contract

production processes to DTA through job work which may also involve change

of form or nature of goods, through job work by units in DTA.

(ii) These units may sub–contract upto 50% of overall

production of previous year in value terms in DTA with permission of Customs

authorities.

(b) (i) EOU may, with annual permission from Customs authorities, under

take job work for

export

, on behalf of DTA

exporter

, provided that goods are

exported directly from EOU and export document shall jointly be in name of

DTA/ EOU. For such exports, DTA units will be entitled for refund of duty

paid on inputs by way of brand rate of duty drawback. However, such brand

rate of drawback shall be as per Customs and Central Excise Duties Drawback

Rules, 2017 and shall be limited to Customs duties and Central Excise Duties

(in respect of eligible items covered under Schedule IV of Central Excise

Act, 1944).

(ii)

Import

of goods for execution of export order placed on EOU by

foreign supplier on job work basis, would be allowed with or without payment

of duties and/or taxes as provided under Para 6.01(d)(ii) above subject to

condition that no DTA clearance shall be allowed.

(iii) Sub-contracting of both production and production processes may

also be under taken without any limit through other

EOU

/EHTP/STP/

BTPBiotechnology Park/SEZ

units, on the basis of records maintained in unit.

(iv) EOU/EHTP/STP/BTP units may sub-contract

part

of production

process abroad and send intermediate products abroad as mentioned in

LoPLetter of Permit. No

permission would be required when goods are sought to be exported from

sub-contractor premises abroad. When goods are sought to be brought back,

prior intimation to concerned

DCDevelopment Commissioner and Customs authorities shall be given.

of production

process abroad and send intermediate products abroad as mentioned in

LoPLetter of Permit. No

permission would be required when goods are sought to be exported from

sub-contractor premises abroad. When goods are sought to be brought back,

prior intimation to concerned

DCDevelopment Commissioner and Customs authorities shall be given.

(c)

Scrap/waste/remnants generated through job work may either be cleared from

job worker’s premises on payment of applicable duty and/or taxes, as

provided under Para 6.07 above on transaction value or destroyed in presence

of Customs authority or returned to unit. Destruction shall not apply to

gold, silver, platinum, diamond, precious and semi-precious stones.

(d) Sub-contracting/ exchange by gems and jewellery EOUs through other

EOUs or SEZ units or units in DTA, shall be as per procedure indicated in

HBP.

6.14

Sale of Unutilized Material and Capital Goods

(a) In case an EOU / EHTP/ STP/BTP unit is unable to utilize goods and

services imported or procured from DTA, it may be:

(i) Transferred to another

EOUExport Oriented Unit/EHTPElectronic Hardware

Technology Park/STP/BTP/ SEZ unit; or

(ii) Disposed of in DTA with intimation to Customs authorities on

payment of applicable duties and/ or taxes and compensation cess. In

addition, exemption of duties of Customs leviable under First Schedule of

the Customs Tariff Act, 1975 availed, if any on the goods , at the time of

import will also be payable. This sale would be further subject to

compliance of applicable import conditions such as requirement of import

Authorisation; or

(iii) Exported.

(iv) Such transfer from EOU/EHTP/STP/BTP unit to another such unit

would be treated as import for receiving unit.

(b)

Capital goods

and

spares

that have become obsolete/ surplus, may be

exported or transferred to SEZ unit, transferred to another EOU/EHTP/STP/BTP/on

payment of applicable GST and compensation cess or disposed of in DTA on

payment of applicable GST and compensation cess and duties of Customs

leviable under First Schedule of the Customs Tariff Act, 1975. Benefit of

depreciation will be available in case of disposal in DTA only when the unit

has achieved positive

NFENet Foreign Exchange

taking into consideration the depreciation allowed. No duty shall be payable

other than the applicable taxes under GST laws incase capital goods,

raw material

consumables

consumables

, spares, goods manufactured,

processed or packaged, and scrap/ waste/remnants /rejects are destroyed

within unit after intimation to Customs authorities or destroyed outside

unit with permission of Customs authorities. Destruction as stated above

shall not apply to gold, silver, platinum, diamond, precious and semi-

precious stones.

, spares, goods manufactured,

processed or packaged, and scrap/ waste/remnants /rejects are destroyed

within unit after intimation to Customs authorities or destroyed outside

unit with permission of Customs authorities. Destruction as stated above

shall not apply to gold, silver, platinum, diamond, precious and semi-

precious stones.

(c) In case of textile sector, disposal of left over material/ fabrics

upto 2% of CIF value or quantity of

import

, whichever is lower, on payment

of duty on transaction value, may be allowed, subject to certification of

Central Excise/Customs officers that these are left over items.

(d) Disposal of used packing material will be allowed on payment of

duty on transaction value.

6.15

Reconditioning/Repair and Re- engineering

(a)

EOU

s shall be set up with approval of

UACUnits Approval Committee to carry out

reconditioning, repair, remaking, testing, calibration, quality improvement,

upgradation of technology and re-engineering activities for

export

in

foreign currency. Provisions of paragraphs 6.07, 6.08, 6.09, 6.12, 6.13of

FTP and para 6.29(a), (b), (c) and (d) of HBP shall not, however, apply to

such activities.

(b) EHTP/STP/BTPBiotechnology Park units shall be set up with approval of

IMSCInter-Ministerial Standing

Committee to carry

out reconditioning, repair, remaking, testing, calibration, quality

improvement, upgradation of technology and re-engineering activities for

export in foreign currency. Provisions of paragraphs 6.07, 6.08, 6.09, 6.12,

6.13of FTP and para 6.29(a), (b),

(c) and (d) of HBP shall not, however, apply to such activities.

6.16

Replacement / Repair of Imported / Indigenous Goods

(a) General provisions of FTP relating to export /import of

replacement/repair of goods would also apply equally to

EOUExport Oriented Unit/EHTPElectronic Hardware

Technology Park/STP/BTP

units. Cases not covered by these provisions shall be considered on merits

by

DCDevelopment Commissioner.

(b) Goods sold in DTA and not accepted for any reasons, may be brought

back for repair/replacement, under intimation to concerned jurisdictional

customs authorities.

(c) Goods or

parts

thereof, on being imported / indigenously procured

and found defective or After payment of

duty and clearance of all dues, unit shall obtain “No Dues Certificate” from

Customs

otherwise unfit for use or which have been damaged

authorities. On the basis of “No Dues Certificate” or become defective subsequently, may be returned against refund of

purchase value/ against replacement or destruction. In the event of

replacement, goods may be received from foreign suppliers or their

authorized agents in India or indigenous suppliers. The unit can take

free

of cost replacement (duty paid) from the authorized agents in India of

foreign suppliers, provided the defective part is re–exported or destroyed.

However, destruction shall not apply to precious and semi-precious stones

and precious metals.

6.17

Exit from the Scheme

(a) With approval of DC/Designated officer of EHTP/ STP/BTP, an EOU/EHTP/STP/BTP

unit may opt out of scheme. Such exit shall be subject to payment of

applicable Excise and Customs duties and on payment of applicable IGST/

CGST/ SGST/ UTGST and compensation cess, if any, and industrial policy in

force.

(b) If unit has not achieved obligations, it shall also be liable to

penalty at the time of exit.

(c) In the event of a gems and jewellery unit ceasing its operation,

gold and other precious metals, alloys, gems and other materials available

for

manufacture

of jewellery, shall be handed over to an agency nominated by

DoCDepartment of Commerce, at price to be determined by that agency.

(d) An EOU / EHTP / STP / BTP unit may also be permitted by DC to exit

from the scheme at any time on payment of applicable duties and taxes and

compensation cess on

capital goods

under the prevailing EPCG Scheme for DTA

Units. This will be subject to fulfillment of positive

NFENet Foreign Exchange criteria under

EOU scheme, eligibility criteria under EPCG scheme and standard conditions

indicated in HBP.

(e) Unit proposing to exit out of the scheme shall intimate DC of

EOU/Designated

officer of EHTP/STP/BTPBiotechnology Park and Customs authorities in writing. Unit shall

assess duty liability arising out of exit and submit details of such

assessment to Customs authorities. Customs authorities shall confirm duty

liabilities on priority basis, subject to the condition that the unit has

achieved positive NFE, taking into consideration the depreciation allowed.

After payment of duty and clearance of all dues, unit shall obtain “No Dues

Certificate” from Customs authorities. On the basis of “No Dues Certificate” so issued by the Customs authorities, unit shall apply to DC/Designated

officer for final exit. In case there is no proceeding pending under FT(D&R)

Act, as amended, DC/Designated officer shall issue final exit

order

within a

period of 7 working days. Between “No Dues Certificate” issued by Customs

authorities and final exit order by DC/Designated officer, unit shall not be

entitled to claim any exemption for procurement of capital goods or inputs.

However, unit can claim Advance Authorization /

DFIADuty Free Import

Authorisation/ Duty Drawback as per

its eligibility. In case the duty calculations and dues are disputed and

take a long time, a BG / Bond / Installment processes backed by BG shall be

provided for expediting the exit process.

(f) In cases where a unit is initially established as

DTA unit with

machines procured from abroad after payment of applicable Import duty, or

from domestic market after payment of excise duty/GST, and unit is

subsequently converted to

EOU

, in such cases removal of such capital goods

to DTA after exit would be without payment of duty. Similarly, in cases

where a DTA unit imported capital goods under EPCG Scheme and after

completely fulfilling

export obligation

gets converted into EOU, unit would

not be charged customs duty on capital goods at the time of removal of such

capital goods in DTA upon exit.

(g) An EOU /

EHTPElectronic Hardware

Technology Park / STP / BTP unit may also be permitted by

DCDevelopment Commissioner to exit

under Advance Authorisation as one time option. This will be subject to

fulfillment of positive NFE criteria.

(h) A simplified procedure may be provided to fast track the

De-bonding/ Exit of the STP / EHTP Unit which has not availed any duty

benefit on procurement of

raw material

, capital goods etc.

6.18

Conversion

(a) Existing DTA units may also apply for conversion into an EOU /

EHTP / STP/ BTP unit.

(b) Existing EHTP / STP units may also apply for conversion / merger to EOU unit and vice-versa. In such cases, units will avail

exemptions in duties and taxes as applicable.

(c) Applications for

conversion into an EOU / EHTP / STP / BTP unit from existing DTA units, having

an investment of Rs. 50 crores and above in plant and machinery or exporting Rs.

50 crores and above annually, shall be placed before

BOABoard of Approval for a decision.

6.19

Monitoring of

NFENet Foreign Exchange

Performance of EOU/EHTP/STP/

BTPBiotechnology Park units shall be monitored by Units

Approval Committee as per guidelines in HBP.

6.20

Export

through Exhibitions/ Export Promotion Tours/ Showrooms

Abroad /Duty Free Shops

EOU / EHTP /

STP / BTP are permitted to:

(i) Export goods for holding/participating in Exhibitions abroad with

permission of DC /Designated officer.

(ii) Personal carriage of gold / silver / platinum jewellery, precious,

semi-precious stones, beads and articles.

(iii) Export goods for display / sale in permitted shops set up abroad.

(iv) Display / sell in permitted shops set up abroad, or in showrooms of

their distributors / agents.

(v) Set up showrooms / retail outlets at International Airports.

6.21

Personal Carriage of

Import

/ Export Parcels including through Foreign Bound

Passengers

Import/ export through personal carriage of gems and jewellery items may

be undertaken as per Customs procedure. However, export proceeds shall be

realized through normal banking channel. Import/ export through personal

carriage by units, other than gems and jewellery units, shall be allowed

provided goods are not in commercial quantity. An authorized

person

of Gems & Jewellery

EOU

may also import gold in primary form, upto 10 Kgs in a financial

year through personal carriage, as per guidelines

prescribed

of Gems & Jewellery

EOU

may also import gold in primary form, upto 10 Kgs in a financial

year through personal carriage, as per guidelines

prescribed

by RBI and

DoRDepartment of Revenue.

by RBI and

DoRDepartment of Revenue.

6.22

Export /Import by Post/

Courier

Goods including

free

samples, may be exported/imported by air freight or

through foreign post office or through courier, as per Customs procedure.

6.23

Administration of EOU / EHTP / STP / BTP units and Powers of

DCDevelopment Commissioner/Designated

Officer of EOU/EHTPElectronic Hardware

Technology Park/STP/SEZ

Details of administration of EOUs / EHTP / STP / BTP units and powers of

DC/Designated Officer are given in HBP.

1.

Inserted Vide:- Notification No. 69/2023 dt. 08.03.2024