from India Schemes

from India SchemesForeign Trade Policy 2015-20

CHAPTER- 3

EXPORTS FROM INDIA SCHEMES

(Relevant Procedure Chapter 3)

3.00 Objective

The objective of schemes under this chapter is to provide rewards to exporters to offset infrastructural inefficiencies and associated costs.

3.01

Exports

from India Schemes

There shall be

following two schemes for exports of Merchandise and Services

respectively:

respectively:

(i) Merchandise Exports from India Scheme (MEIS).

(ii) Service Exports from India Scheme (SEIS).

3.02 Nature of Rewards

Duty Credit Scrips shall be granted as rewards under MEIS Merchandise Exports from India Scheme and SEIS Service Exports From India Scheme. The Duty Credit Scrips and goods imported / domestically procured against them shall be freely transferable. The Duty Credit Scrips can be used for :

(i) Payment of Basic Customs Duty and Additional Customs Duty specified under sections 3 (1), 3 (3) and 3 (5) of the Customs Tariff Act, 1975 for import

of inputs or goods, including capital goods

, as per DoR Department of Revenue Notification, except items listed in Appendix 3A.

(ii) Payment of Central excise duties on domestic procurement of inputs or goods,

(iii) Deleted

(iv) Payment of Basic Customs Duty and Additional Customs Duty specified under Sections 3 (1), 3 (3) and 3 (5) of the Customs Tariff Act, 1975 and fee as per paragraph 3.18 of this Policy.

Merchandise Exports from India Scheme (MEIS)

3.03 Objective

Objective

of the Merchandise Exports from India Scheme (MEIS) is to promote the

manufacture

and export

of notified goods/ products.

and export

of notified goods/ products.

3.04 Entitlement under MEIS Merchandise Exports from India Scheme

Exports of notified goods/products with ITC[HS] code, to notified markets as listed in Appendix 3B, shall be rewarded under MEIS Merchandise Exports from India Scheme. Appendix 3B also lists the rate(s) of rewards on various notified products [ITC (HS) code wise]. The basis of calculation of reward would be on realised FOB value of exports in free foreign exchange, or on FOB value of exports as given in the Shipping Bills in freely convertible foreign currencies, whichever is less, unless otherwise specified .

.6[3.04A Entitlement under MEIS Merchandise Exports from India Scheme

11[The total reward which may be granted to an IEC holder under the Merchandise Exports from India Scheme (MEIS) shall not exceed Rs. 2 Crore per IEC on exports made in the period 01.09.2020 to 31.12.2020 [period based on Let Export Order (LEO) date of shipping bill(s)]. Any IEC holder who has not made any export with LEO date during the period 01.09.2019 to 31.08.2020 or any new IEC obtained on or after 01.09.2020 would not be eligible for submitting any claim for benefits under MEIS Merchandise Exports from India Scheme for exports made with effect from 01.09.2020.]old[The total reward which may be granted to an IEC holder under the Merchandise Exports from India Scheme (MEIS) shall not exceed Rs. 2 Crore per IEC on exports made in the period 01.09.2020 to 31.12.2020 [period based on Let Export Order (LEO) date of shipping bilks)]. Any IEC holder who has not made any export with LEO date during the period 01.09.2019 to 31.08.2020 or any new IEC obtained on or after 01.09.2020 would not be eligible for submitting any claim for benefits under MEIS Merchandise Exports from India Scheme for exports made with effect from 01.09.2020. The aforesaid ceiling may be subject to further downward revision to ensure that the total claim under the Scheme for the period (01.09.2020 to 31.12.2020) does not exceed the allocation prescribed by the Government, which is Rs 5,000 Cr.]

3.04B Entitlement under MEIS Merchandise Exports from India Scheme

Benefits under MEIS Merchandise Exports from India Scheme shall not be available for

export

made with effect from 01.01.2021.]

3.05 2[Entitlement under MEIS Merchandise Exports from India Scheme for Export of goods through courier or foreign post offices] old[Export of goods through courier or foreign post offices using e-Commerce]

Exports of goods through courier or foreign post office, as notified in Appendix 3C, of FOB value upto Rs 5,00,000 per consignment shall be entitled for rewards under MEIS Merchandise Exports from India Scheme. If the value of exports, is more than Rs 5,00,000 per consignment then MEIS Merchandise Exports from India Scheme reward would be calculated on the basis of FOB Value of Rs 5,00,000 only.]3.06 Ineligible categories under MEIS Merchandise Exports from India Scheme

The following exports categories /sectors shall be ineligible for Duty Credit Scrip entitlement under MEIS Merchandise Exports from India Scheme

through trans-shipment, meaning thereby exports that

are originating in third country but trans-shipped through India; /EHTP Electronic Hardware Technology Park/ BTP Biotechnology Park /FTWZ Free Trade and Warehousing Zone products exported through DTA

units;

/EHTP Electronic Hardware Technology Park/ BTP Biotechnology Park /FTWZ Free Trade and Warehousing Zone products exported through DTA

units;(vii) Exports made by units in FTWZ Free Trade and Warehousing Zone.

Service Exports from India Scheme (SEIS)

3.07 Objective

Objective of Service Exports from India Scheme (SEIS) is to encourage and maximize export of notified Services from India.3.08 Eligibility

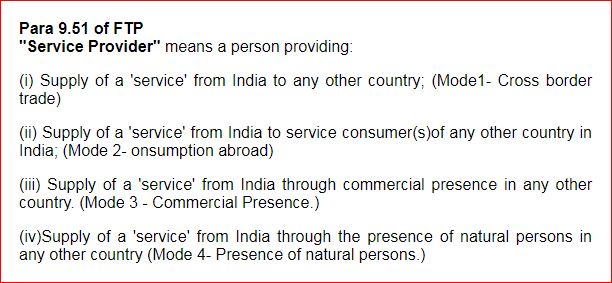

(a) Service Providers of notified services, located in India, shall be

rewarded under SEIS Service Exports From India Scheme. Only Services

rendered in the manner as per Para

9.51(i) and Para 9.51(ii) of this policy shall be eligible. The notified

services and rates of rewards are listed in Appendix 3D.

of notified services, located in India, shall be

rewarded under SEIS Service Exports From India Scheme. Only Services

rendered in the manner as per Para

9.51(i) and Para 9.51(ii) of this policy shall be eligible. The notified

services and rates of rewards are listed in Appendix 3D.

8[3.08 (aa)

For SETS claims on services rendered in the FY 2019-20, the notified

services and rates are listed in Appendix 3X as per Annexure to this

Notification.]

1[(b) Such service provider

should have minimum net free foreign exchange earnings of US$15,000 in

year of rendering service to be eligible for Duty Credit Scrip. For

Individual Service Providers and sole proprietorship, such minimum net

free foreign exchange earnings criteria would be US$10,000 in year of

rendering service.]

5[However, the service categories eligible under the scheme and the rates of reward on such services as rendered w.e.f. 1st April, 2019 to 31st March, 2020 shall be notified separately in Appendix 3 X. For the services rendered w.e.f. 1st April, 2020, decision on continuation of the scheme will be taken subsequently and notified accordingly]

old[(b)

Such service provider should have minimum net free foreign exchange

earnings of US$15,000 in preceding financial year to be eligible for

Duty Credit Scrip. For Individual Service Providers and sole

proprietorship, such minimum net free foreign exchange earnings criteria

would be US$10,000 in preceding financial year.]

(c) Payment in Indian Rupees for service charges earned on specified

services, shall be treated as receipt in deemed foreign exchange as per

guidelines of Reserve Bank of India. The list of such services is

indicated in Appendix 3E.

8[However, there shall be no such

specified services under Appendix 3E for exports

made in the financial

year 2019-20]

(d) Net Foreign exchange earnings for the scheme are defined as under:

Net Foreign Exchange = Gross Earnings of Foreign Exchange minus Total

expenses / payment / remittances of Foreign Exchange by the IEC holder,

relating to service sector in the Financial year.

(e) If the IEC holder is a manufacturer of goods as well as service

provider, then the foreign exchange earnings and Total expenses /

payment / remittances shall be taken into account for service sector

only.

(f) In order to claim reward under the scheme, Service provider shall

have to have an active IEC at the time of rendering such services for

which rewards are claimed.

3.09 Ineligible categories under SEIS Service Exports From India Scheme

Foreign exchange remittances other than those earned for rendering of notified services would not be counted for entitlement. Thus, other sources of foreign exchange earnings such as equity or debt participation, donations, receipts of repayment of loans etc. and any other inflow of foreign exchange, unrelated to rendering of service, would be ineligible.

3.10

Entitlement under SEIS Service Exports From India Scheme

Service Providers

of eligible services

shall

be entitled to Duty Credit Scrip at notified rates (as given in Appendix

3D) on net foreign exchange earned.

8[3.10A For SEIS Service Exports From India Scheme claim for FY 2019-20, service providers of eligible services shall be entitled to Duty Credit Scrip at notified rates (as given in Appendix 3X) on net foreign exchange earned, with the total entitlement capped at Rs 5 Crore per IEC for FY 2019-20.

3.10 B For SEIS Service Exports From India Scheme claim for FY 2019-20, the deadline for filing the online application as per ANF 3B shall be 31.12.2021. Provision of late cut under para 9.02 of HBP 2015-20 shall not apply for SEIS Service Exports From India Scheme applications for FY 2019-20 and such applications shall get time-barred after 31.12.2021.]

3.11 Remittances through Credit Card and other instruments for MEIS Merchandise Exports from India Scheme and SEIS Service Exports From India Scheme

Free Foreign Exchange earned through

international credit cards and other instruments, as permitted by RBI Reserve Bank of India

shall also be taken into account for computation of value of exports

.

3.12 Effective date of schemes (MEIS Merchandise Exports from India Scheme and SEIS Service Exports From India Scheme)

The schemes shall come into force with effect from the date of notification of this Policy, i.e. the rewards under MEIS Merchandise Exports from India Scheme/SEIS Service Exports From India Scheme shall be admissible for exports made/services rendered on or after the date of notification of this Policy.

3.13 Special Provisions

(a) Government reserves the right in public interest, to specify export products or services or markets, which shall not be eligible for computation of entitlement of duty credit scrip.

(b) Government reserves the right to impose restriction / change the

rate/ceiling on Duty Credit Scrip under this chapter.

(c) Government may also notify goods in Appendix 3A which shall not be

allowed for debiting through Duty Credit Scrips in case of import

.

(d) Government may prescribe value cap of any kind for a product(s) or limit total reward per IEC holder under this chapter at any time.

Common Provisions for Exports from India Schemes (MEIS Merchandise Exports from India Scheme and SEIS Service Exports From India Scheme)

7[3.13A Last Date of Submitting Applications for Scrip based Schemes

12[The last date for submission of online

applications under MEIS Merchandise Exports from India Scheme for exports

made in the period 01.09.2020 to 31.12.2020

, and applicable late cut as in Para 9.02 of HBP would be as below:

| Scheme | Last date of submission of Application | Late Cut if

submitted till the last date as in column 2 (as % age of Entitlement under the scheme) |

| (1) | (2) | (3) |

| MEIS Merchandise Exports from India Scheme (for exports in the period 01.09.2020 to 31.12.2020) | 31.08.2022 | Nil |

No further MEIS Merchandise Exports from India Scheme

applications would be allowed to be submitted after the prescribed

last

date (as above) and such applications would become time-barred. Late cut

provisions shall also not be available for submitting claims at a later

date.]

last

date (as above) and such applications would become time-barred. Late cut

provisions shall also not be available for submitting claims at a later

date.]

old[11[a.With effect from 07.03.2022, the last date for submission of online applications for certain scrip based Schemes and applicable late cut on such applications would be :

| Scheme |

Last date of submission of Application |

Late Cut if submitted till the last date as in column 2 (as % age of Entitlement under the scheme) |

| (1) | (2) | (3) |

|

(i) MEIS Merchandise Exports from India Scheme (for exports made in the period 01.04.2020 to 31.12.2020) |

30.04.2022 |

Nil |

|

(ii) 2 % additional ad hoc incentive (under para 3.25 of the FTP - for exports made in the period 01.01.2020 to 31.03.2020 only) |

30.04.2022 |

Nil |

|

(iii) ROSCTL (for exports made in the period 07.03.2019 to 31.12.2020) |

15.03.2022 |

Nil |

|

(iv) ROSL (for exports made upto 06.03.2019 for which claims have not yet been disbursed under scrip mechanism) |

15.03.2022 |

Nil |

No further applications would be allowed to be submitted after the prescribed last date (as above) as they would become time-barred. Late cut provisions shall also not be available for submitting claims thereafter.]]

old[a. In supersession of the existing laid down provisions in the Hand Book of

Procedures, 2015-20 with regard to last date for submitting online applications

for scrip based claims, the last date for submitting online applications stands

revised to 10[28th February 2022] 9[31st January 2022]

old[31st December 2021] for the following schemes i.e.

i. for MEIS Merchandise Exports from India Scheme (for exports made in the period (s) 01.07.2018 to 31.03.2019,

01.04.2019 to 31.03.2020 and 01.04.2020 to 31.12.2020),

ii. for SEIS Service Exports From India Scheme (for service exports rendered in FY 18-19 and FY 2019-20),

iii. for 2 % additional ad hoc incentive (under para 3.25 of the FTP — for

exports made in the period 01.01.2020 to 31.03.2020 only),

iv'. for ROSCTL (for exports made from 07.03.2019 to 31.12.2020) and

v. for ROSL (for exports made upto 06.03.2019 for which claims have not yet been

disbursed under scrip mechanism).

After 10[28.02.2022] 9[31.01.2022] old[31.12.2021], no further applications would be allowed to be submitted and they would become time-barred. Late cut provisions shall also not be available for submitting claims at a later date.]

b. In supersession of the laid down provisions on applicable late cut as in para 9.02 of the HBP, the new late cut for applications submitted upto 10[28.02.2022] 9[31.01.2022] old[31.12.2021] as indicated above shall be:

|

SI. No. |

Scheme |

Period of Exports (Let Export Date in the period)/Services rendered in the period |

Late Cut (as % age of Entitlement under the Scheme) |

| 1 | MEIS Merchandise Exports from India Scheme | FY 2018-19 (01.07.2018 to 31.03.2019) |

10% |

| 2 | MEIS Merchandise Exports from India Scheme | FY 2019-20 and FY 2020-21 (upto 31.12.2020) |

Nil |

| 3 | SEIS Service Exports From India Scheme | FY 2018-19 |

5% |

| 4 | SEIS Service Exports From India Scheme | FY 2019-20 |

Nil |

| 5 | ROSCTL | 07.03.2019 to 31.12.2020 |

Nil |

| 6 | ROSL | Upto 06.03.2019 |

Nil |

3.13B Validity Period of Scrips

a. In supersession of existing laid down provisions regarding validity of a Duty Credit Scrip in Hand Book of Procedures (HBP) 2015-20, the new validity period of a Duty Credit Scrip issued on or after 16.09.2021 shall be 12 months from the date of issue, for scrip based Schemes under chapter 3 and chapter 4 of the Foreign Trade Policy (FTP) 2015-20 or the earlier FTPs]

3.14 Transitional Arrangement

For the goods exported or services

rendered

upto the date of notification of this Policy, which were otherwise

eligible for issuance of scrips under erstwhile Chapter 3 of the earlier

Foreign Trade Policy(ies) and scrip is applied / issued on or after

notification of this Policy against such export

of goods or services

rendered, the then prevailing policy and procedure regarding

eligibility, entitlement, transferability, usage of scrip and any other

condition in force at the time of export of goods or rendering of the

services, shall be applicable to such scrips.

3.15 CENVAT/ Drawback

Additional Customs duty specified under Sections 3(1), 3(3) and 3(5) of the Customs Tariff Act, 1975 /Central excise duty paid in cash or through debit under Duty Credit scrip shall be adjusted as CENVAT Credit or Duty Drawback as per DoR Department of Revenue rules or notifications. Basic Custom duty paid in cash or through debit under Duty Credit scrip shall be adjusted for Duty Drawback as per DoR Department of Revenue rules or notifications.

3.16

Import

under lease financing

Utilization of Duty Credit Scrip shall be

permitted for payment of duty in case of import of capital goods

under

lease financing in terms of provision in paragraph 2.34 of FTP.

3.17 Transfer of export

performance

shall be counted in export performance / turnover of applicant

only if export proceeds from overseas are realized in applicant's bank

account and this shall be evidenced from e - BRC Electronic Bank Realisation Certificate / FIRC Foreign Exchange Inward Remittance Certificate.

shall be counted in export performance / turnover of applicant

only if export proceeds from overseas are realized in applicant's bank

account and this shall be evidenced from e - BRC Electronic Bank Realisation Certificate / FIRC Foreign Exchange Inward Remittance Certificate. (along with disclaimer from the company / firm who has

realized the foreign exchange directly from overseas) or by the company/

firm who has realized the foreign exchange directly from overseas.

(along with disclaimer from the company / firm who has

realized the foreign exchange directly from overseas) or by the company/

firm who has realized the foreign exchange directly from overseas.3.18 Facility of payment of custom duties and fee through duty credit scrips

(a) Duty

Credit Scrip can be utilized / debited for payment of Custom Duties in

case of EO Export Obligation defaults for

Authorisations

issued under Chapters 4 and 5 of

Foreign Trade Policy. Such utilization /usage shall be in respect of

those goods which are permitted to be imported under the respective

reward schemes. However, penalty / interest shall be required to be paid

in cash.

issued under Chapters 4 and 5 of

Foreign Trade Policy. Such utilization /usage shall be in respect of

those goods which are permitted to be imported under the respective

reward schemes. However, penalty / interest shall be required to be paid

in cash.

(b) Duty credit scrips can also be used for payment of composition fee

under FTP, for payment of application fee under FTP, if any and for

payment of value shortfall in EO Export Obligation under Para 4.49 of HBP 2015-20.

3.19 Risk Management System

(a) A Risk Management System shall be in operation whereby every month Computer system in DGFT Headquarters, on random basis and on the basis of guidelines issued by the DGFT from time to time, will select 10% of applications for each RA Regional Authority where scrips and Status Holder Certificates

have already been issued, under each scheme. RA Regional Authority in turn may call for

original documents in all such selected cases for further examination in

detail. In case any discrepancy and/ or over claim is found on such

examination, the applicant

shall be under obligation to rectify such

discrepancy and/or refund over claim in cash with interest at the rate

prescribed

under section 28 A A of the Customs Act 1962, from the date

of issue of scrip in the relevant Head of Account of Customs within one

month. The original holder of scrip, however, may refund such over claim

by surrendering the same scrip whether partially utilized or fully

unutilized, without interest.

Certificates

have already been issued, under each scheme. RA Regional Authority in turn may call for

original documents in all such selected cases for further examination in

detail. In case any discrepancy and/ or over claim is found on such

examination, the applicant

shall be under obligation to rectify such

discrepancy and/or refund over claim in cash with interest at the rate

prescribed

under section 28 A A of the Customs Act 1962, from the date

of issue of scrip in the relevant Head of Account of Customs within one

month. The original holder of scrip, however, may refund such over claim

by surrendering the same scrip whether partially utilized or fully

unutilized, without interest.(b)

Regional Authority

may ask for original proof of landing

certificate (wherever required under the policy), annexures attached to

ANFs or any other document, which has been uploaded digitally or any

other export related documents related to the application such as Export

Invoices at any time within three years from the date of issue of scrip.

Failure to submit such documents in original would make applicant liable

to refund the reward granted along with interest at the rate prescribed

under section 28 A A of the Customs Act 1962, from the date of issuance

of scrip. If an applicant is found to have mis-declared the Item

description under any ITC HS Code, appropriate action under FT(D&R) Act,

would be taken. It would be the responsibility of applicant to maintain

such documents, certificate etc. for a period of at least three years

from the date of issuance of scrips or the completion of scrutiny under

RMS initiated by the RA Regional Authority whichever is later.

may ask for original proof of landing

certificate (wherever required under the policy), annexures attached to

ANFs or any other document, which has been uploaded digitally or any

other export related documents related to the application such as Export

Invoices at any time within three years from the date of issue of scrip.

Failure to submit such documents in original would make applicant liable

to refund the reward granted along with interest at the rate prescribed

under section 28 A A of the Customs Act 1962, from the date of issuance

of scrip. If an applicant is found to have mis-declared the Item

description under any ITC HS Code, appropriate action under FT(D&R) Act,

would be taken. It would be the responsibility of applicant to maintain

such documents, certificate etc. for a period of at least three years

from the date of issuance of scrips or the completion of scrutiny under

RMS initiated by the RA Regional Authority whichever is later.

3.20 Status Holder

(a) Status Holders are business leaders who have excelled in international trade and have successfully contributed to country's foreign trade. Status Holders are expected to not only contribute towards India's exports

but

also provide guidance and handholding to new entrepreneurs.

13[b) All exporters of goods, services

and technology

having an

import-export code (IEC) number shall be eligible for recognition as a

status holder. Status recognition will depend on export performance. An

applicant

shall be categorized as status holder on achieving export

performance during the current and previous three financial years (for

Gems & Jewellery Sector the performance during the current and previous

two financial years shall be considered for recognition as status

holder) as indicated in paragraph 3.21 of Foreign Trade Policy. The

export performance will be counted on the basis of FOB of export earning

in freely convertible foreign currencies or in Indian Rupees as per para

2.53 of the FTP.]

having an

import-export code (IEC) number shall be eligible for recognition as a

status holder. Status recognition will depend on export performance. An

applicant

shall be categorized as status holder on achieving export

performance during the current and previous three financial years (for

Gems & Jewellery Sector the performance during the current and previous

two financial years shall be considered for recognition as status

holder) as indicated in paragraph 3.21 of Foreign Trade Policy. The

export performance will be counted on the basis of FOB of export earning

in freely convertible foreign currencies or in Indian Rupees as per para

2.53 of the FTP.]

old[(b) All exporters of goods, services and technology having an import-export code (IEC) number shall be eligible for recognition as a status holder. Status recognition will depend on export performance. An applicant shall be categorized as status holder on achieving export performance during the current and previous three financial years (for Gems& Jewellery Sector the performance during the current and previous two financial years shall be considered for recognition as status holder) as indicated in paragraph 3.21 of Foreign Trade Policy. The export performance will be counted on the basis of FOB of export earning in freely convertible foreign currencies]

(c) For deemed export, FOR value of exports in Indian Rupees shall be converted in US$ at the exchange rate notified by CBEC, as applicable on 1st April of each Financial Year.

(d) For granting status, export performance is necessary in at least two out of four years.

3.21 Status Category

| Status Category | Export Performance FOB / FOR (as converted) Value (in US $ million) |

| One Star Export House | 3 |

| Two Star Export House | 25 |

| Three Star Export House | 100 |

| Four Star Export House | 500 |

| Five Star Export House | 2000 |

3.22 Grant of double weightage

(a) The exports

by IEC holders under the following categories shall be granted

double weightage for calculation of export performance for grant of

status.

(i) Micro, Small & Medium Enterprises (MSME) as defined in Micro, Small & Medium Enterprises Development (MSMED) Act 2006.

(ii) Manufacturing units having ISO/BIS Bureau of Indian Standards.

(iii) Units located in North Eastern States including Sikkim and Jammu & Kashmir.

(iv) Units located in Agri Export Zones.

(b) Double Weightage shall be available for grant of One Star Export House Status category only. Such benefit of double weightage shall not be admissible for grant of status recognition of other categories namely Two Star Export House, Three Star Export House, Four Star export House and Five Star Export House.

(c) A shipment can get double weightage only once in any one of above categories.

3.23 Other conditions for grant of status

(a) Export performance of one IEC holder shall not be permitted to be

transferred to another IEC holder. Hence, calculation of exports

performance based on disclaimer shall not be allowed.

(b) Exports made on re-export basis shall not be counted for

recognition.

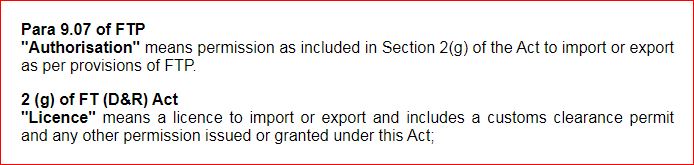

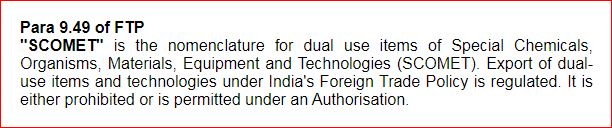

(c) Export of items under Authorisation

, including SCOMET

items, would

be included for calculation of export performance.

items, would

be included for calculation of export performance.

3.24

Privileges of Status Holders

and Customs Clearances for both import

and

exports

may be granted on self-declaration basis;

otherwise anywhere in FTP or HBP; who are also Status Holders shall be eligible to self-certify

their goods as originating from India as per Para 2.108 (d) of Hand Book

of Procedures.

who are also Status Holders shall be eligible to self-certify

their goods as originating from India as per Para 2.108 (d) of Hand Book

of Procedures.  for all exporters (excluding the exporters of following

sectors-(l) Gems and Jewellery Sector, (2) Articles of Gold and precious metals

sector) .

for all exporters (excluding the exporters of following

sectors-(l) Gems and Jewellery Sector, (2) Articles of Gold and precious metals

sector) .The free of cost supplies made under provisions of Para 3.24(j) shall not be entitled to Duty Drawback or' any other export incentive under any export promotion scheme.]

old[(j) Status holders shall be entitled to export freely exportable items (excluding Gems and Jewellery, Articles of Gold and precious metals) on free of cost basis for export promotion subject to an annual limit of Rupees One Crore or 2% of average annual export realization during preceding three licensing years, whichever is lower. For export of pharma products by pharmaceutical companies, the annual limit would be 2% of the average annual export realisation during preceding three licensing years. In case of supplies of pharmaceutical products, vaccines and lifesaving drugs to health programmes of international agencies such as UN, WHO-PAHO and Government health programmes, the annual limit shall be upto 8% of the average annual export realisation during preceding three licensing years. Such free of cost supplies shall not be entitled to Duty Drawback or any other export incentive under any export promotion scheme']

4[3.25 2% Additional Ad hoc

A 2% Additional Ad hoc Incentive for 2 HS Codes/

tariff lines, as below :

i. 85171211 - Mobile phones, other than push button type and

ii. 85171219 - Mobile phones, push button type-

would be available, along with

the rewards under MEIS Merchandise Exports from India Scheme for exports made in the period 01.01.2020 to 31.03.2020

only. The basis of calculation of reward would be on realised FOB value of

exports

in free foreign exchange, or on FOB value of exports as given in the

Shipping Bills in freely convertible foreign currencies, whichever is less,

unless otherwise specified

. All other provisions as applicable for MEIS Merchandise Exports from India Scheme in the

Foreign Trade Policy, 2015-20 and Handbook of Procedures 2015-20, shall be

applicable for the 2% Additional Ad Hoc Incentive as well. The application for

MEIS Merchandise Exports from India Scheme for the said codes would be considered as an application for the Additional

Ad hoc Incentive also.]

Refer Trade Notice No. 08/2018-19 Dated

15.05.2018

Refer Trade Notice No. 42/2015-20 Dated

11.01.2019

Refer

Public Notice No. 72/2015-20 Dated

05.02.2019

Refer Trade

Notice No. 46/2018-19 Dated 06.02.2019

Refer Policy

Circular No. 20/2015-20 Dated 22.02.2019

Refer

Public Notice No. 09/2015-20 Dated

11.06.2019

Refer

Instruction No. 03/2019 -Customs dt. 13/08/2019

Refer

Circulars No. 02/2020 -Customs dt. 10/01/2020

Refer Public Notice No. 58/2015-20 Dated

29.01.2020

Refer Trade

Notice No. 3/2020-21 Dated 15.04.2020

1.Substituted Vide:- Notification No. 08/2015-20 Dated 24.05.2018

2.Substituted Vide:- Notification No. 22/2015-2020 Dated 26.07.2018

3.Substituted Vide:-Notification No. 28/2015-2020 Dated 27.08.2018

4.Inserted Vide :-Notification No. 43/2015-2020 Dated 29.01.2020

5. Inserted Vide Notification No. 57/2015-2020 Dt.31/03/2020

6. Inserted Vide Notification No. 30/2015-2020 Dt.01/09/2020

7. Inserted Vide Notification No. 26/2015-2020 Dt.16/09/2021

8. Inserted Vide Notification No. 29/2015-2020 Dt.23/09/2021

9. Substituted Vide Notification No. 48/2015-2020 Dt.31/12/2021

10. Substituted Vide Notification No. 53/2015-2020 Dt.01/02/2022

11. Substituted Vide Notification No. 58/2015-2020 Dt.07/03/2022

12. Substituted Vide Notification No. 15/2015-2020 Dt.01/07/2022

13. Substituted Vide:-Notification No. 43/2015-2020 Dated 09.11.2022