or

export

or

export

and includes any new business of import or export proposed

to be undertaken by the existing

importer

and includes any new business of import or export proposed

to be undertaken by the existing

importer

or

exporter

or

exporter

, as the case may be;]]helldod]

[helldodold[(a) "activity" means import or export;]helldod]

, as the case may be;]]helldod]

[helldodold[(a) "activity" means import or export;]helldod]| Previous |

Customs Act 1962

Advance Rulings

Section 28E. Definitions

In this Chapter, unless the context otherwise requires, -

[helldod5omit[1[(a) “activity” means

import

or

export

and includes any new business of import or export proposed

to be undertaken by the existing

importer

or

exporter

, as the case may be;]]helldod]

[helldodold[(a) "activity" means import or export;]helldod]

3[(b) 'advance

ruling' means a written decision on any of the questions referred to in

section

28H raised by the applicant in his application in respect of any

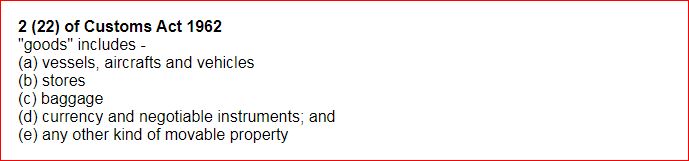

goods

prior to

its importation or exportation]

prior to

its importation or exportation]

[helldodold[(b) "advance ruling" means the determination, by the Authority, of a question of law or fact specified in the application regarding the liability to pay duty in relation to an activity which is proposed to be undertaken, by the applicant;]helldod]

[helldod7omit[4[(ba) 'Appellate Authority' means the Authority for Advance Rulings constituted under section 245-O of the Income-tax Act, 1961;]]helldod]

3[(c)

'applicant' means any person,''

(i) holding a valid Importer-exporter Code Number granted under

section 7 of the

Foreign Trade (Development and Regulation) Act, 1992; or

(ii) exporting any goods to

India

; or

; or

(iii) with a justifiable cause to the satisfaction of the Authority,

who makes an application for advance ruling under section 28H;']

[helldodold[( c) "applicant" means—

(i) ( a) a non-resident setting up a joint venture in India in collaboration with a non-resident or a resident; or

(b) a resident setting up a joint venture in India in collaboration with a non-resident; or

(c) a wholly owned subsidiary Indian company, of which the holding company is a foreign company, who or which, as the case may be, proposes to undertake any business activity in India;

(ii) a joint venture in India; or

(iii) a resident falling within any such class or category of persons, as the Central Government may, by notification in the Official Gazette, specify in this behalf, and which or who, as the case may be, makes application for advance ruling under sub-section (1) of section 28H;]helldod]

[helldod6omit[1Explanation.—For the purposes of this clause, “joint venture in India” means a contractual arrangement whereby two or more persons undertake an economic activity which is subject to joint control and one or more of the participants or partners or equity holders is a non-resident having substantial interest in such arrangement;]helldod]

(d) "application" means an application made to the Authority under sub-section (1) of section 28H;3[(e) 'Authority' means the Customs Authority for Advance Rulings appointed under section 28EA;]

[helldodold[2[(e) Authority” means the Authority for Advance Rulings constituted under section 245-O of the Income-tax Act, 1961;]helldod]

[helldodold[(e) "Authority" means the Authority for Advance Rulings (Central Excise, Customs and Service Tax) constituted under section 28F;]helldod]

[helldod7omit[(f) "Chairperson" means the Chairperson of the 3[Appellate Authority] [helldodold[Authority]helldod];

[helldod7omit[(g) "Member" means a Member of the 3[Appellate Authority] [helldodold[Authority]helldod] and includes the Chairperson; and]helldod]

[helldod6omit[(h) "non-resident", "Indian company" and "foreign company" have the meanings respectively assigned to them in clauses ( 30), ( 26) and ( 23A) of section 2 of the Income-tax Act, 1961.]helldod]

1. Substituted Vide Chapter IV of Finance bill 2013

2. Substituted Vide Section 93 of Finance Act, 2017

3. Substituted Vide Section 64 of Finance Act 2018

4. Inserted Vide Section 64 of Finance Act 2018

5. Omitted Vide Section 64 of Finance Act 2018

6. Omitted Vide Section 90 of Finance Act 2022

7. Omitted Vide The Tribunals Reforms (Rationalisation and Conditions of Service) Ordinance, 2021 [Para 5 (a)]

| Previous |