under the Customs Tariff Act, 1975 (51 of 1975);

under the Customs Tariff Act, 1975 (51 of 1975);| Previous |

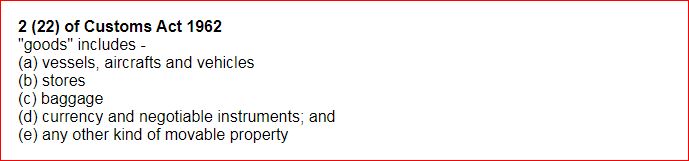

Customs Act 1962

Advance Rulings

Section 28H. Application for advance ruling

*(1) An applicant desirous of obtaining an advance ruling under this Chapter may make an application in such form and in such manner 4[and accompanied by such fee] as may be prescribed, stating the question on which the advance ruling is sought.

(2) The question on which the advance ruling is sought shall be in respect of, -

(a)

classification of

goods

under the Customs Tariff Act, 1975 (51 of 1975);

(b) applicability of a notification issued under sub-section (1) of section 25, having a bearing on the rate of duty;

(c)

the principles

to be adopted for the purposes of determination of

value

of the goods under the

provisions of this Act.

of the goods under the

provisions of this Act.

2[(d) applicability of notifications issued in respect of tax or duties under this Act or the Customs Tariff Act, 1975 or any tax or duty chargeable under any other law for the time being in force in the same manner as duty of customs leviable under this Act or the Customs Tariff Act;]

[helldodold[(d) applicability of notifications issued in respect of duties under this Act, the Customs Tariff Act, 1975 (51 of 1975) and any duty chargeable under any other law for the time being in force in the same manner as duty of customs leviable under this Act.]helldod]

(e) determination of origin of the goods in terms of the rules notified under the Customs Tariff Act, 1975 (51 of 1975) and matters relating thereto.

3[(f) any other matter as the Central Government may, by notification, specify.]

[helldod5omit[(3) The application shall be made in quadruplicate and be accompanied by a fee of 1[ten thousand rupees] [helldodold[two thousand five hundred rupees]helldod]]helldod]

(4) An applicant may withdraw his application 6[at any time before an advance ruling is pronounced] [helldodold[within thirty days from the date of the application]helldod].

3[(5)

The applicant may be represented by any person resident in

India

who is

authorised in this behalf.

who is

authorised in this behalf.

Explanation.''For the purposes of this sub-section 'resident' shall have the same meaning as assigned to it in clause (42) of section 2 of the Income-tax Act, 1961.']

1. Substituted Vide Section 96 of the Finance Act, 2017

2. Substituted Vide Section 67 of the Finance Act 2018

3. Inserted Vide Section 67 of the Finance Act 2018

4. Inserted Vide Section 91 of the Finance Act 2022

5. Omitted Vide Section 91 of the Finance Act 2022

6. Substituted Vide Section 91 of the Finance Act 2022

| Previous |