Duty Drawback- A Detailed Analysis

Duty drawback simply means the duties which have been paid at the time of import are being paid back by the Government. In other words, the import of goods from outside India are chargeable to customs duty. However, in certain situations, the customs duty paid on the import of goods are refunded to the importers in the form of duty drawbacks under customs. In this article we are going to discuss in detail about the concept of duty drawback and the conditions of drawback.

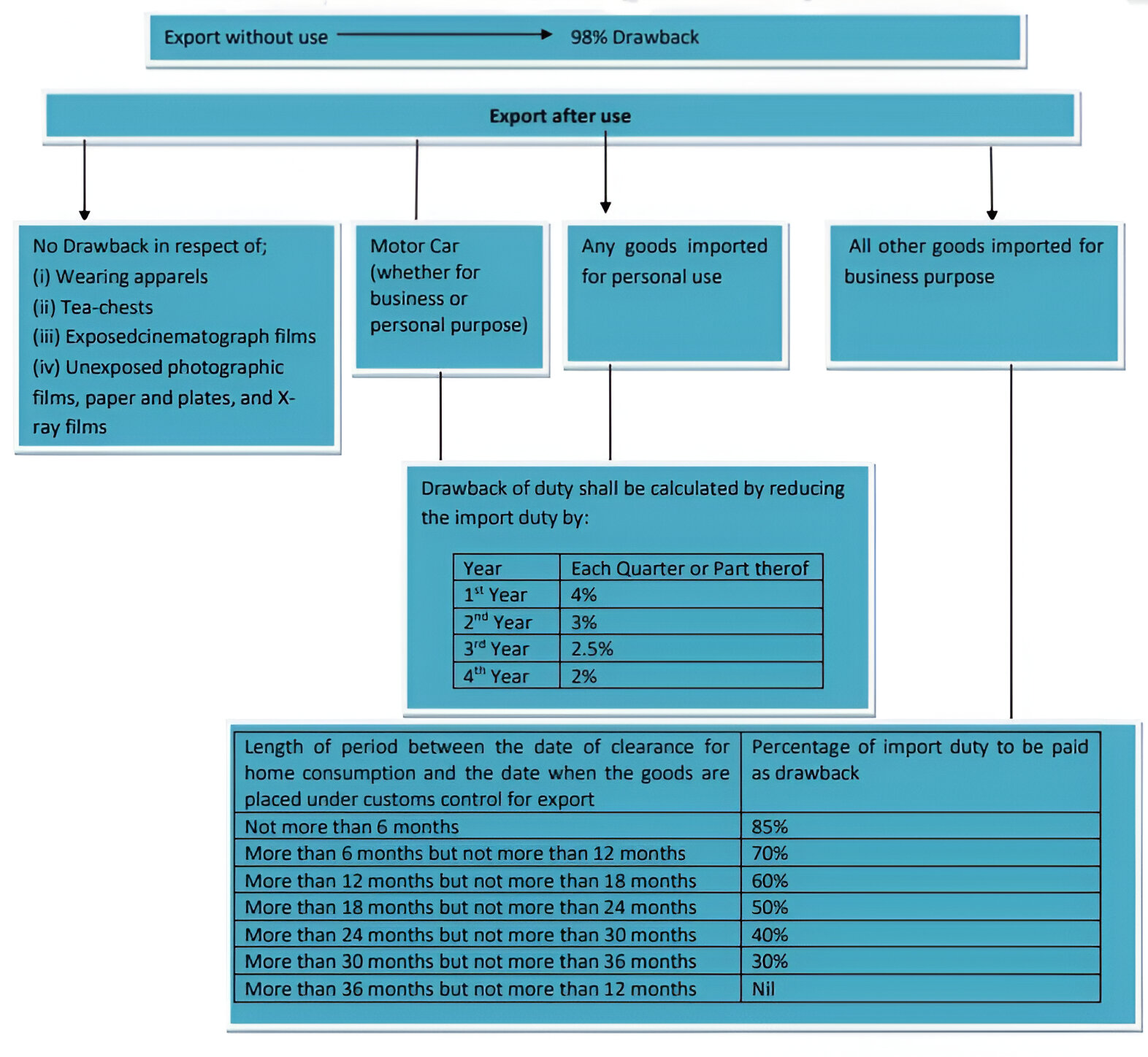

The provisions relating to duty drawback are contained in section 74 & section 75 of Customs Act 1962. Under section 74 the drawback is allowable on re export of goods on which duty was paid at the time of import. The rate of duty drawback under section 74 would be 98% of duty paid at the time of import. However, such drawback would subject to certain conditions;

(i) said goods are being exported within two years from the date of payment of duty on the importation and

(ii) such goods are identified to the satisfaction of the Assistant Commissioner of Customs or Deputy Commissioner of Customs as the goods which were imported.

Further, sub section 2 of section 74 of Customs Act 1962 states that in the case of goods which have been used after the importation, the rates of drawback thereof shall be such as fixed by the Central Government by way of notification in the Official Gazette. Accordingly, in the exercise of the powers conferred by section 74(2), the Central Government has fixed the rates at which drawback of import duty shall be allowed in respect of goods used after their importation. The said rates of duty drawback are fixed by issuing a Notification No. 19/65-Cus dated 06.02.1965.

The following rates have been fixed at which drawback for import duty shall be allowed for goods that have been used after an importation:

|

Length of period between the date of clearance for home consumption and the date when the goods are placed under customs control for export |

Percentage of import duty to be paid as drawback |

|

Not more than 6 months |

85% |

|

More than 6 months but not more than 12 months |

70% |

|

More than 12 months but not more than 18 months |

60% |

|

More than 18 months but not more than 24 months |

50% |

|

More than 24 months but not more than 30 months |

40% |

|

More than 30 months but not more than 36 months |

30% |

|

More than 36 months but not more than 12 months |

Nil |

However, no drawback of import duty will be allowed in respect of the following goods, if they have been used after their importation in India;

(i) Wearing apparels

(ii) Tea-chests

(iii) Exposed cinematograph films passed by the Board of Film Censors in India

(iv) Unexposed photographic films, paper and plates, and X-ray films

In the case of motor car or the goods (other than the goods specified in (i) to (iv) above) imported by the person for his personal and private use, the drawback of duty shall be calculated by reducing the following percentage of the import duty paid in respect of such motor car or goods;

| Year | Drawback of duty shall be calculated by reducing the import duty by |

| 1st year | 4% per quarter or part thereof |

| 2nd Year | 3% per quarter or part thereof |

| 3rd Year | 2.5% per quarter or part thereof |

| 4th Year | 2% per quarter or part thereof |

Also no drawback shall be allowed if such motor car or goods has or have been used for more than 4 years.

Let us summarised the section 74 with the help of following diagram;

Drawback on imported materials used in the manufacture of exported goods (Section 75 of Customs Act 1962):

Duty drawback under section 75 of the Customs Act covers the cases where any raw material has been imported from outside India and such material is used in the manufacturing or processing of final products which are being exported. In such case, duty drawback shall be allowed for the duty paid on the imported material used for the manufacture or processing of such goods. However, no drawback shall be allowed u/s 75, if the export value of such goods or class of goods is less than the value of the imported materials used in the manufacture or processing of such goods.

It is also important to know that export proceeds of such product should also be received with in the time prescribed under Foreign Exchange Management Act, 1999 i.e., within 9 months. Accordingly, if any duty drawback has been allowed and sale proceeds on export have not been received in accordance with the provisions of FEMA 1999, then such duty drawback shall be deemed to have never been allowed and the procedure for recovery or adjustment of the drawback amount shall be initiated.

Further, if it appears to the Central Government that the quantity of a particular material imported into India is more than the total quantity of like material that has been used in the goods manufactured, processed or on which any operation has been carried out in India and exported outside India, then, the Central Government may declare that so much of the material as is contained in the goods exported shall be deemed to be imported material.

The another important point that needs to be noted here is that under section 75 of customs Act 1962, the duty drawback would also be allowed in respect of raw material which is being procured from India and used in manufacture of final product which is being exported outside India.

The rates of duty drawback under section 75 are notified by the Central Government vide Notification No. 77/2023-Customs (N.T.) Dated 20.10.2023. These are called All Industry Rates of drawback. However, as per clause 9 of said notification, no drawback shall be allowed on export of a commodity or product if such commodity or product is;

(i) manufactured partly or wholly in a warehouse under section 65 of the Customs Act, 1962.

(ii) manufactured or exported in discharge of export obligation against an Advance Authorisation or Duty-Free Import Authorisation issued under the Duty Exemption Scheme of the relevant Foreign Trade Policy

(iii) manufactured or exported by a unit licensed as 100% Export Oriented Unit

(iv) manufactured or exported by any of the units situated in Free Trade Zones or Export Processing Zones or Special Economic Zones;

(v) manufactured or exported availing the benefit of the notification No. 32/1997-Customs, dated 1st April, 1997.

Thus from the above it is clear that no drawback shall be allowed in respect of goods exported under MOOWR Schemes, goods exported against Advance Authorisation or Duty-Free Import Authorisation, goods exported by EOU, SEZ.

Main difference between drawback under section 74 & 75;

1. The drawback under section 74 can be claimed in respect of goods which were imported earlier and the same goods are being exported after that. However, the drawback under section 75 can be claimed when any raw material is procured and finished goods are being exported after manufacture. In other words, the drawback under section 74 can be claimed when the imported product and exported both are of same HSN. However, the drawback under section 75 can be claimed when the imported product and exported both are of different HSN.

2. The another difference between drawback under section 74 & 75 is that drawback under section 74 is allowed only when goods are imported from outside India. In other words, the drawback under section 74 is not allowed on goods which are procured domestically and exported outside India. However, the drawback under section 75 is allowed even if the raw material is purchased domestically and exported outside India.

Interest on Drawback

In case the drawback payable to a claimant under section 74 or 75 is not paid within 1 month from the date of filing of the claim for such drawback, then the claimant shall be paid interest at the rate not less than 5% and not exceeding 30% from the date immediately after the expiry of 1 month till the date of payment of such drawback. Further, if excess drawback has been paid to the claimant, then the claimant shall pay the drawback within 2 months from the date of demand along with interest at the rate not less than 10% and not exceeding 36%. The interest shall be payable from the date of payment of such drawback to the claimant till the date of recovery of the drawback.

Further as per

section 76 of customs Act 1962, no drawback shall be allowed -

(a) in respect of any goods the market-price of which is less than the amount of

drawback due thereon;

(b) where the drawback due in respect of any goods is less than fifty rupees.

Disclaimer: The information given in this article is solely for purpose of understanding the law. It is completely based on the interpretation of the author and cannot be constituted as a legal advise, the author of this article and Lawcrux team is not responsible for any legal issues if arises on the basis of the interpretation given above.