Sales Promotional Expenses- ITC available or not

In the competitive world, the companies usually execute/implement certain attractive promotional methodology to the boost up the sale of their goods or services and to attract new customers. These methodologies include various discount offers, involvement of free samples, providing warranty services etc. In this respect it is important to know about the GST implications on said attractive schemes and the eligibility of ITC in respect of inputs, input services or capital goods used in the production of goods which are distributed at free of cost or as sample. In this article we will discuss about the eligibility of ITC for the same.

As per section 7(1)(a) of CGST Act 2017 the supply includes all forms of supply of goods or services or both such as sale, transfer, barter, exchange, licence, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business. Accordingly, as per section 7(1)(a), for a transaction to be considered as supply there must be a flow of consideration. However, Schedule I of CGST Act 2017 specifies the list of transactions or activities which shall be considered as supply even if made without consideration. Thus if any transaction is covered under Schedule I of CGST Act then it would be treated as supply even if made without consideration.

Further, it is important to know that as per the clause (h) of sub section 5 of section 17 of CGST Act 2017 the ITC is blocked in respect of goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples.

From the above provisions it is clear that if any transaction is covered under schedule I then it would be treated as supply & GST would be applicable on it even if no consideration is involved. Let us discuss an example:

A company XYZ Ltd. has distributed gold coins having value Rs. 60,000/- to their employees for achieving the sales target. What would be the GST implications in this case and whether ITC would be available to XYZ Ltd. in respect of such gold coins purchased by them.

In this case the transaction of distributing the gold coins to employees would be covered under the para 2 of schedule I which covers the supply of goods or services or both between related persons or between distinct persons. Since the employees are considered as related person as per the Explanation given under Section 15.

It is also to be noted that there is a proviso to para 2 of schedule I which states that the gifts not exceeding Rs. 50,000/- in value in a financial year by an employer to an employee shall not be treated as supply. Hence the transaction of distributing the gold coins having value Rs. 60,000/- to employees would not be covered under said proviso and will be squarely covered under Schedule I and accordingly GST would be applicable in such transaction. Since the GST would be applicable on such transaction therefore the employer would also eligible to claim ITC in respect of tax paid at the time of purchase of such coins.

In Circular No. 92/11/2019 the clarifications are provided in respect of the various sales promotional schemes. The same is also summarised as follows;

Buy one get one free offer:

In the said circular it was clarified that in case of Buy one get one offer, it is not an individual supply of free goods but a case of two or more individual supplies where a single price is being charged for the entire supply. Taxability of such supply will be dependent upon as to whether the supply is a composite supply or a mixed supply and the rate of tax shall be determined as per the provisions of section 8 of CGST Act. It is also clarified that ITC shall be available to the supplier for the inputs, input services and capital goods used in relation to supply of goods or services as part of such offers.

Free samples and gifts:

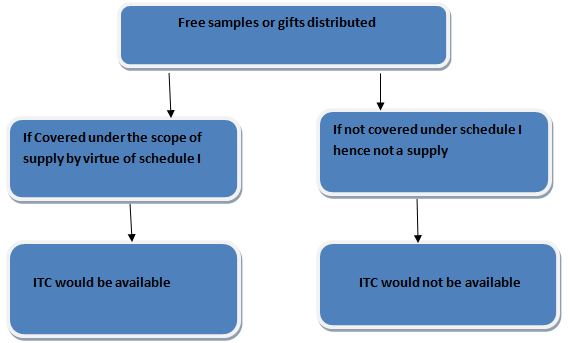

In this respect it was clarified in the circular that the ITC shall not be available to the supplier on the inputs, input services and capital goods to the extent they are used in relation to the gifts or free samples distributed without any consideration. However, where the activity of distribution of gifts or free samples falls in Schedule I, the supplier would be eligible to avail of the ITC.

Judicial Pronouncements:

There are many Advance Rulings in respect of the issue involving ITC on sales promotion expenses and gifts. So let’s dicuss the same:

1. Orient Cement Limited [2023(09)LCX0230(AAR)]

The Company (applicant) is engaged in the business of manufacture of Ordinary Portland Cement (OPC) & Pozzolona Portland Cement (PPC). The applicant is transferring different Goods to its dealers as incentives for achieving their sales targets. These include Gold Coins or White Goods such as a Microwave, Split Ac etc.

The applicant wants to whether the gold coins and white goods to the dealers / customers upon they achieving the stipulated lifting of the material / purchase target during the scheme period would be regarded as "goods disposed of by way of gift" and ITC on the same would be restricted as provided under the Section 17(5)(h) of the CGST Act, 2017?

The Telangana Authority for advance ruling held that the applicant is making supply of white goods and gold to his dealers or stockiest in return for the dealers or stockiest attaining a threshold of sales indicated in the scheme and therefore, the value of white goods and gold supplied by him are for the ‘act’ of achieving this threshold and therefore taxable in his hands. The value of the goods supply is determined under Section 15 of the GST Act read with Rule 30 of the CGST Rules. Since the transaction is taxable as supply of goods therefore eligible for ITC.

2. Kanahiya Realty Private Limited [2021(09)LCX0093(AAR)]

The West Bengal Authority for advance ruling held that the supply of goods at nominal price to retailers against purchase of specified units of hosiery goods pursuant to a promotional scheme would qualify as individual supplies taxable at the rates applicable to each of such goods as per section 9 of the GST Act. Further the credit of the input tax paid on the items being sold at nominal prices would be available to the applicant.

3. M/s Golden Tobie Private Limited [2021(10)LCX0151(AAR)]

In this case the applicant as per their sales promotion strategy would supply extra packs of cigarettes along with their regular supply quantity to their distributors without receiving any additional consideration or additional payment for the extra supply.

The Uttar Pradesh Authority for Advance Ruling in this case held that the additional 30 packs of cigarettes on every purchase of 100 packs of cigarettes would not be considered as exempt supplies or free samples and the ITC would be available to the supplier.

Conclusion: In nutshell the eligibility of ITC in respect of free samples or gifts distributed under sales promotional scheme can be understand with the help of following diagram:

Disclaimer: The information given in this article is solely for purpose of understanding the law. It is completely based on the interpretation of the author and cannot be constituted as a legal advise, the author of this article and Lawcrux team is not responsible for any legal issues if arises on the basis of the interpretation given above.