and the

recipient

and the

recipient

of the supply are not related and the price is the sole consideration

for the supply.

of the supply are not related and the price is the sole consideration

for the supply.| Previous |

THE CENTRAL GOODS AND SERVICES TAX ACT, 2017

TIME AND VALUE OF SUPPLY

Section 15: Value of taxable supply. (Relevant Rules 27 to 35) (Relevant Updates)

(1) The value of a supply of goods or services or

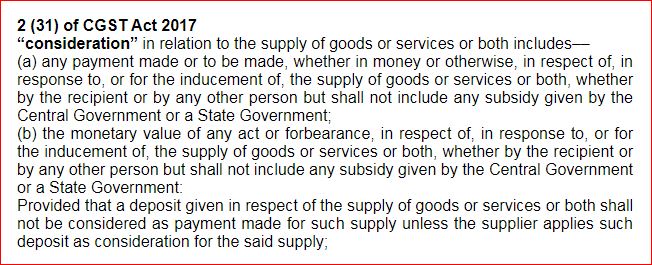

both shall be the transaction value, which is the price actually paid or payable

for the said supply of goods or services or both where the

supplier

and the

recipient

of the supply are not related and the price is the sole consideration

for the supply.

(2) The value of supply shall include––

*a)

any taxes, duties,

cesses, fees and charges levied under any law for the time being in force other

than this Act, the State Goods and Services Tax Act

, the

Union Territory Goods and Services Tax Act

, the

Union Territory Goods and Services Tax Act

and the

Goods and Services Tax (Compensation to States) Act

and the

Goods and Services Tax (Compensation to States) Act

, if charged separately by the supplier;

, if charged separately by the supplier;

*b)

any amount that the

supplier is liable to pay in relation to such supply but which has been

incurred by the recipient of the supply and not included in the price actually

paid or payable for the goods

or services or both;.

or services or both;.

c)

incidental expenses,

including commission and packing, charged by the supplier to the recipient of a

supply and any amount charged for anything done by the supplier in respect of

the supply of goods or services

or both at the time of, or before delivery of

goods or supply of services;

or both at the time of, or before delivery of

goods or supply of services;

*d)

interest or late fee

or penalty for delayed payment of any

consideration

for any supply; and

for any supply; and

*e)

subsidies

directly linked to the price excluding subsidies provided by the Central

Government and State Governments.

Explanation.––For the purposes of this sub-section, the amount of subsidy shall be included in the value of supply of the supplier who receives the subsidy.

*(3) The value of the supply shall not include any discount which is given––

*a) before or at the time

of the supply if such discount has been duly recorded in the

invoice

issued in

respect of such supply; and

issued in

respect of such supply; and

*b) after

the supply has been effected, if—

(i) such discount is established in terms of an agreement entered into at or before the time of such supply and specifically linked to relevant invoices; and

*(ii) input tax credit

as is attributable to the discount on the basis of document

issued by the supplier has been reversed by the recipient of the supply.

(4) Where the value of the supply of goods or services or both cannot be determined under sub-section (1), the same shall be determined in such manner as may be prescribed.

(5) Notwithstanding anything contained in

sub-section (1) or sub-section (4), the value of such supplies

as may be

notified by the

Government

on the recommendations of the

Council

on the recommendations of the

Council

shall be

determined in such manner as may be prescribed.

shall be

determined in such manner as may be prescribed.

Explanation.—For the purposes of this Act,––

(a)

persons

shall be deemed to be “related

persons” if––

shall be deemed to be “related

persons” if––

(i) such persons are officers or directors of one another’s businesses;

(ii) such persons are legally recognised partners in

business

;

;

(iii) such persons are employer and employee;

(iv) any person directly or indirectly owns, controls or holds twenty-five per cent or more of the outstanding voting stock or shares of both of them;

(v) one of them directly or indirectly controls the other;

(vi) both of them are directly or indirectly controlled by a third person;

(vii) together they directly or indirectly control a third person; or they are

members of the same

family

;

;

(b) the term “person” also includes legal persons;

(c) persons who are associated in the business of one another in that one is the sole agent or sole distributor or sole concessionaire, howsoever described, of the other, shall be deemed to be related.

| Previous |