Chapter - VIII of CGST Rules,

2017

RETURNS

RULE 80. Annual return (corresponding

section 44)

4[(1) Every registered person, other than those referred to in the second proviso

to section 44, an

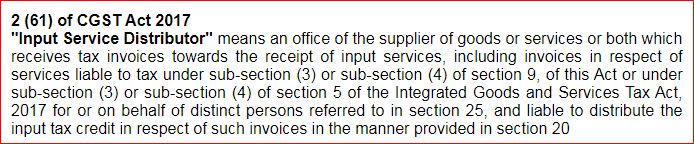

Input Service Distributor

, a person paying tax under

section

51 or section 52, a

casual taxable person

, a person paying tax under

section

51 or section 52, a

casual taxable person

and a non-resident taxable person,

shall furnish an annual return for every financial year as specified under

section 44 electronically in

FORM GSTR-9 on or before the thirty-first

day of December following the end of such financial year through the common

portal either directly or through a Facilitation Centre notified by the

Commissioner:

and a non-resident taxable person,

shall furnish an annual return for every financial year as specified under

section 44 electronically in

FORM GSTR-9 on or before the thirty-first

day of December following the end of such financial year through the common

portal either directly or through a Facilitation Centre notified by the

Commissioner:

Provided that a person

paying tax under section 10 shall furnish the annual return in

FORM GSTR-9A.

5[(1A)

Notwithstanding anything contained in sub-rule (1), for the financial year

2020-2021 the said annual return shall be furnished on or before the

twenty-eighth day of February, 2022.]

6[(1B)

Notwithstanding anything contained in sub-rule (1), for the financial year

2022-2023, the said annual return shall be furnished on or before the tenth day

of January, 2024 for the registered persons whose principal place of business is

in the districts of Chennai, Tiruvallur, Chengalpattu, Kancheepuram, Tirunelveli,

Tenkasi, Kanyakumari, Thoothukudi and Virudhunagar in the state of Tamil Nadu.;]

(2) Every electronic

commerce operator required to collect tax at source under

section 52 shall

furnish annual statement referred to in sub-section (5) of the said section in

FORM GSTR - 9B.

(3) Every registered person,

other than those referred to in the second proviso to

section 44, an Input

Service Distributor, a person paying tax under

section 51 or

section 52, a

casual taxable person and a non-resident taxable person, whose

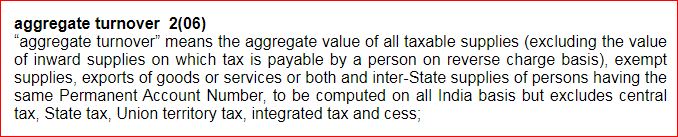

aggregate turnover

during a financial year exceeds five crore rupees, shall also furnish a

self-certified reconciliation statement as specified under

section 44 in

FORM

GSTR-9C along with the annual return referred to in sub-rule (1), on or

before the thirty-first day of December following the end of such financial

year, electronically through the common portal either directly or through a

Facilitation Centre notified by the Commissioner.”.]

during a financial year exceeds five crore rupees, shall also furnish a

self-certified reconciliation statement as specified under

section 44 in

FORM

GSTR-9C along with the annual return referred to in sub-rule (1), on or

before the thirty-first day of December following the end of such financial

year, electronically through the common portal either directly or through a

Facilitation Centre notified by the Commissioner.”.]

[helldod old[(1) Every registered person, other than an Input Service Distributor a person

paying tax under section 51 or

section 52, a

casual taxable person

and a

nonresident taxable person, shall furnish an annual return as specified under

sub-section (1) of section 44 electronically in

FORM GSTR-9 through the common

portal either directly or through a Facilitation Centre notified by the

Commissioner:

Provided that a person paying tax under

section 10 shall furnish the annual

return in FORM GSTR-9A.

(2) Every electronic commerce operator required to collect tax at source under

section 52 shall furnish annual statement referred to in sub-section (5) of the

said section in FORM GSTR -9B.

(3) Every registered person 1[other than

those referred to in the proviso to sub-section (5) of

section 35] whose

aggregate turnover

during a financial year

exceeds two crore rupees shall get his accounts audited as specified under

sub-section (5) of section 35 and he shall furnish a copy of audited annual

accounts and a reconciliation statement, duly certified, in

FORM GSTR-9C,

electronically through the common portal either directly or through a

Facilitation Centre notified by the Commissioner.

3[Provided that for the financial year

2018-2019 and 2019-2020, every registered person whose aggregate turnover

exceeds five crore rupees shall get his accounts audited as specified under

sub-section (5) of

section 35 and he shall furnish a copy of audited annual

accounts and a reconciliation statement, duly certified, in

FORM GSTR-9C

for the said financial year, electronically through the common portal either

directly or through a Facilitation Centre notified by the Commissioner.]

helldod]

[helldod old[2[Provided that every registered person whose

aggregate turnover

during the financial year 2018-2019 exceeds five crore rupees shall get

his accounts audited as specified under subsection (5) of

section 35 and he

shall furnish a copy of audited annual accounts and a reconciliation statement,

duly certified, in FORM GSTR-9C for

the financial year 2018- 2019, electronically through the common portal either

directly or through a Facilitation Centre notified by the Commissioner.]]

helldod]

5[(3A)

Notwithstanding anything contained in sub-rule (3), for the financial year

2020-2021 the said self-certified reconciliation statement shall be furnished

along with the said annual return on or before the twenty-eighth day of

February, 2022.]

6[(3B)

Notwithstanding anything contained in sub-rule (3), for the financial year

2022-2023, the said self certified reconciliation statement shall be furnished

along with the said annual return on or before the tenth day of January, 2024

for the registered persons whose principal place of business is in the districts

of Chennai, Tiruvallur, Chengalpattu, Kancheepuram, Tirunelveli, Tenkasi,

Kanyakumari, Thoothukudi and Virudhunagar in the state of Tamil Nadu.;]