Chapter III of CGST Rules,

2017

REGISTRATION

RULE 8. Application for registration.- (corresponding

section 25, section 27)

10[(1)

Every person who is liable to be registered under sub-section (1) of

section 25 and every person seeking

registration under sub-section (3) of

section 25 (hereafter in this Chapter

referred to as "the applicant"), except-

(i) a non-resident taxable

person;

(ii) a person required to

deduct tax at source under section 51;

(iii) a person required to

collect tax at source under section 52;

(iv) a person supplying

online information and database access or retrieval services from a place

outside India to a non-taxable online recipient referred to in

section 14 or

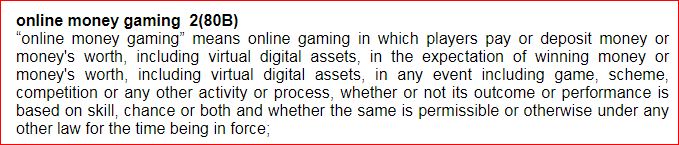

a person supplying

online money gaming

from a place outside India to a

person in India referred to in

section 14A under the Integrated Goods and

Services Tax Act, 2017 (13 of 2017),

from a place outside India to a

person in India referred to in

section 14A under the Integrated Goods and

Services Tax Act, 2017 (13 of 2017),

shall, before applying for

registration, declare his Permanent Account Number, State or Union territory in

Part A of FORM GST REG-01 on the common portal, either directly or

through a Facilitation Centre notified by the Commissioner:

Provided

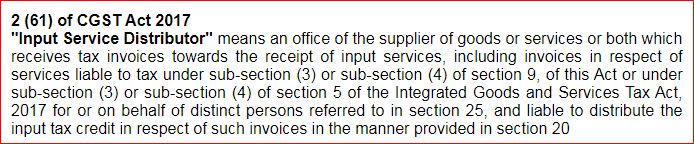

that every person being an

Input Service Distributor

shall make a

separate application for registration as such Input Service Distributor.]

shall make a

separate application for registration as such Input Service Distributor.]

[helldodold[(1) Every person, other than a

non-resident taxable person, a person required to deduct tax at source under

section 51, a person required to collect tax at source under

section 52 and a

person supplying online information and database access or retrieval services

from a place outside India to a non-taxable online recipient referred to in

section 14 of the Integrated Goods and Services Tax Act, 2017 (13 of 2017) who

is liable to be registered under sub-section (1) of

section 25 and every person

seeking registration under sub-section (3) of

section 25 (hereafter in this

Chapter referred to as 'the applicant') shall, before applying for registration,

declare his Permanent Account Number,

[helldod 6omit[mobile number, e-mail address,]

helldod] State or

Union territory in Part A of FORM GST REG-01 on

the common portal, either directly or through a Facilitation Centre notified by

the Commissioner:

[helldod

1omit[Provided that a person having a unit(s) in a Special Economic Zone or being a

Special Economic Zone developer shall make a separate application for

registration as a business vertical distinct from his other units located

outside the Special Economic Zone:]helldod]

2[Provided]

[helldod

old[ Provided further]helldod] that every person being an

Input Service Distributor shall make a separate application for registration as

such Input Service Distributor.]helldod]

(2) (a) The Permanent Account Number shall be validated online by the common

portal from the database maintained by the Central Board of Direct Taxes 7[and

shall also be verified through separate one-time passwords sent to the mobile

number and e-mail address linked to the Permanent Account Number]

[helldod 6omit[(b) The mobile number declared under sub-rule (1) shall be verified through a

one-time password sent to the said mobile number; and

(c) The e-mail address declared under sub-rule (1) shall be verified through a

separate one-time password sent to the said e-mail address.] helldod]

(3) On successful verification of the Permanent Account Number, mobile number

and email address, a temporary reference number shall be generated and

communicated to the applicant on the said mobile number and e-mail address.

(4) Using the reference number generated under sub-rule (3), the applicant shall

electronically submit an application in Part B of FORM GST REG-01, duly signed

or verified through electronic verification code, along with the documents

specified in the said Form at the common portal, either directly or through a

Facilitation Centre notified by the Commissioner.

*9[(4A) Where an applicant, other than a person notified under

sub-section (6D) of section 25, opts for authentication of Aadhaar number,

he shall, while submitting the application under sub-rule (4), undergo

authentication of Aadhaar number and the date of submission of the

application in such cases shall be the date of authentication of the Aadhaar

number, or fifteen days from the submission of the application in Part B of

FORM GST REG-01 under sub-rule (4), whichever is earlier.

Provided that every application made under sub-rule (4) by a

person, other than a person notified under sub-section (6D) of

section 25,

who has opted for authentication of Aadhaar number and is identified on the

common portal, based on data analysis and risk parameters, shall be followed

by biometric-based Aadhaar authentication and taking photograph of the

applicant where the applicant is an individual or of such individuals in

relation to the applicant as notified under sub-section (6C) of

section 25

where the applicant is not an individual, along with the verification of the

original copy of the documents uploaded with the application in

FORM GST

REG-01 at one of the Facilitation Centres notified by the

Commissioner for the purpose of this sub-rule and the application shall be

deemed to be complete only after completion of the process laid down under

this proviso;]

11[Provided

further that every application made under sub-rule (4) by a person, other than a

person notified under sub-section (6D) of

section

25, who has not opted for authentication of Aadhaar number, shall be followed by

taking photograph of the applicant where the applicant is an individual or of

such individuals in relation to the applicant as notified under sub-section (6C)

of section

25 where the applicant is not an individual, along with the

verification of the original copy of the documents uploaded with the application

in FORM GST REG-01 at one of the Facilitation

Centers notified by the Commissioner for the purpose of this sub-rule and the

application shall be deemed to be complete only after successful verification as

laid down under this proviso.]

[helldod old[8[(4A)

Every application made under sub-rule (4) by a person, other than a person

notified under sub-section (6D) of

section 25, who has opted for authentication of Aadhaar number and is

identified on the common portal, based on data analysis and risk parameters,

shall be followed by biometric-based Aadhaar authentication and taking

photograph of the applicant where the applicant is an individual or of such

individuals in relation to the applicant as notified under subsection (6C) of

section 25 where the applicant

is not an individual, along with the verification of the original copy of the

documents uploaded with the application in FORM

GST REG-01 at one of the Facilitation Centres notified by the Commissioner

for the purpose of this sub-rule and the application shall be deemed to be

complete only after completion of the process laid down under this sub-rule] helldod]

[helldod old[5[(4A)Every

application made under rule (4) shall be followed by—

(a) biometric-based Aadhaar authentication and taking photograph, unless

exempted under subsection (6D) of section 25, if he has opted for authentication

of Aadhaar number; or

(b) taking biometric information, photograph and verification of such other KYC

documents, as

notified, unless the applicant is exempted under sub-section (6D) of section 25,

if he has opted not

to get Aadhaar authentication done,

of the applicant where the applicant is an individual or of such individuals in

relation to the applicant as

notified under sub-section (6C) of section 25

where the applicant is not an individual, along with the verification of the

original copy of the documents uploaded with the application in FORM GST REG-01 at one of the Facilitation Centres notified by the Commissioner for the purpose

of this sub-rule and the

application shall be deemed to be complete only after completion of the process

laid down under this subrule.].] helldod]

[helldod old[4[(4A)

Where an applicant, other than a person notified under sub-section (6D) of section 25, opts for authentication of Aadhaar number, he

shall, while submitting the application under sub-rule (4), with effect from 21st

August, 2020, undergo authentication of Aadhaar number and the date of

submission of the application in such cases shall be the date of authentication

of the Aadhaar number, or fifteen days from the submission of the application in

Part B of FORM GST REG-01 under subrule (4),

whichever is earlier.]

helldod]

[helldod old[3[(4A) The applicant shall, while submitting an application

under sub-rule (4), with effect from 01.04.2020, undergo authentication of Aadhaar number for grant of registration]helldod]

7[(4B)

The Central Government may, on the recommendations of the Council, by

notification specify the States or Union territories wherein the 9[proviso to]

[helldodold[provisions of]helldod]

sub-rule (4A) shall not apply.]

(5) On receipt of an application under sub-rule (4) 7[or

sub-rule (4A)], an acknowledgement shall be

issued electronically to the applicant in FORM GST REG-02.

(6) A person applying for registration as a

casual taxable person

shall be given

a temporary reference number by the common portal for making advance deposit of

tax in accordance with the provisions of

section 27 and the acknowledgement

under sub-rule (5) shall be issued electronically only after the said deposit.

shall be given

a temporary reference number by the common portal for making advance deposit of

tax in accordance with the provisions of

section 27 and the acknowledgement

under sub-rule (5) shall be issued electronically only after the said deposit.