Topic

Publish Date

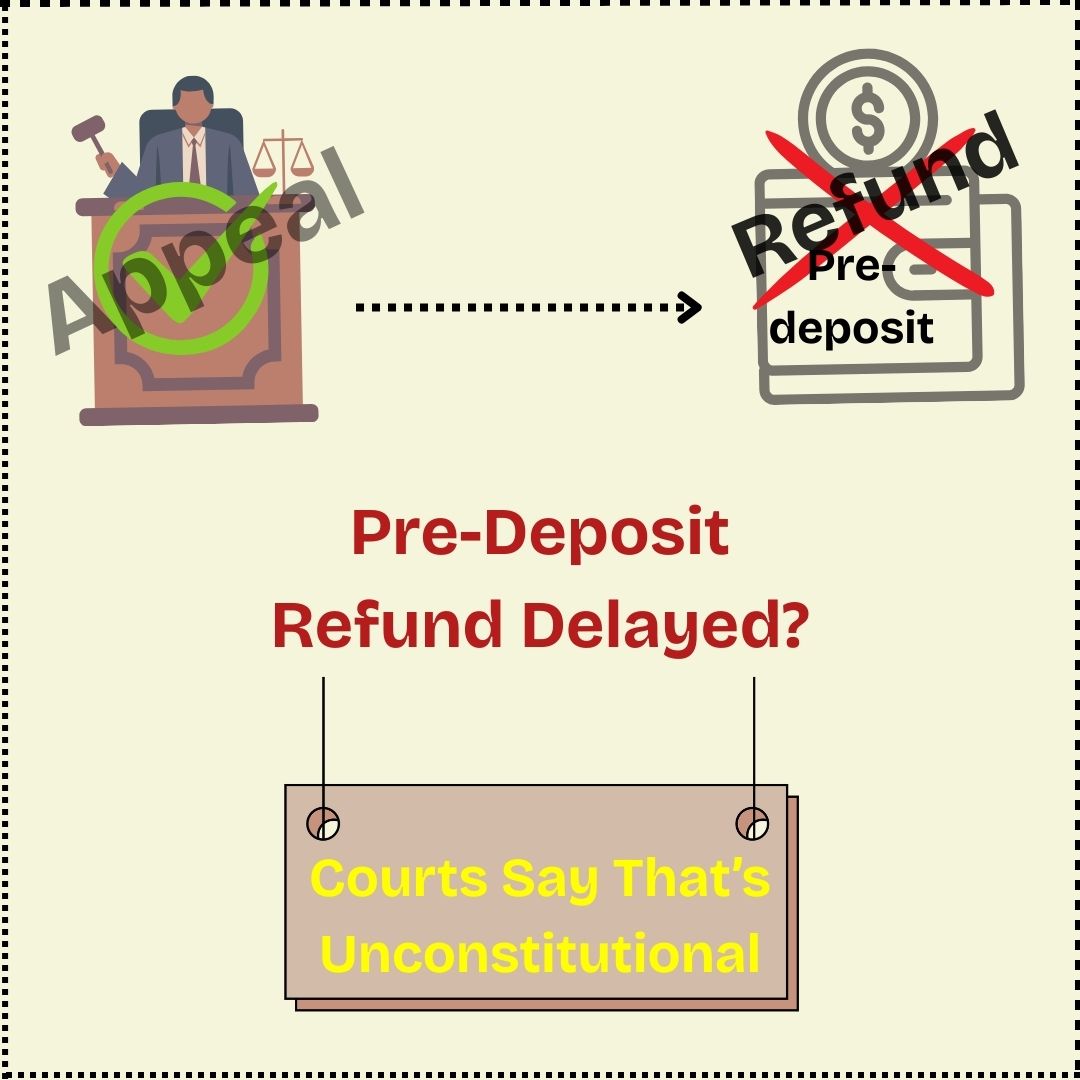

Pre-Deposit Refund Delayed? Courts Say That's Unconstitutional

"Justice delayed is justice denied," they say. But what if it's delayed not by courts—but by portals, procedural rigidity, and a misinterpretation of the word "may"? This is the story of a taxpayer who fulfilled every requirement under the law, won their appeal fair and square, and yet had to knock on the doors of the High Court just to get back what was rightfully theirs—a statutory pre-deposit................... Read More

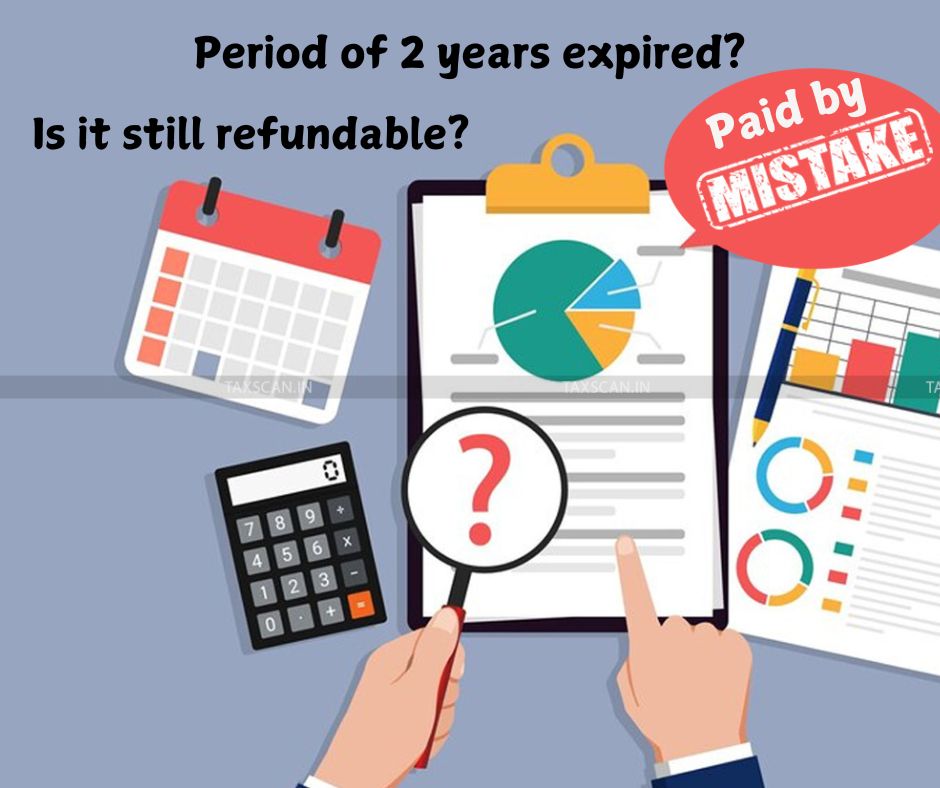

Paid by Mistake? Here's Why Time Limits May Not Block Your Refund

Imagine this: A taxpayer, either suo-moto or subsequently, deposits a hefty sum with the tax department. Time passes, the case fizzles out, and two years later, they realize the amount was never actually payable. They rush to claim a refund—only to be told, "Sorry, you’re too late! The two-year window under Section 54(1) has closed". ut is that really the end of the road? Judicial precedents say otherwise........................ Read More