*(i) persons making any inter-State taxable supply;

*(ii)

casual taxable persons

making taxable supply;

making taxable supply;

(iii)

persons

who are required to pay tax under

reverse charge

who are required to pay tax under

reverse charge

;

;

(iv) person who are required to pay tax under sub-section (5) of section 9;

*(v)

non-resident taxable persons

making taxable supply;

making taxable supply;

*(vi) persons who are required to deduct tax under section 51, whether or not separately registered under this Act;

*(vii) persons who make

taxable supply

of goods or

services

of goods or

services

or both on behalf of

other

taxable person

or both on behalf of

other

taxable person

whether as an

agent

whether as an

agent

or otherwise;

or otherwise;

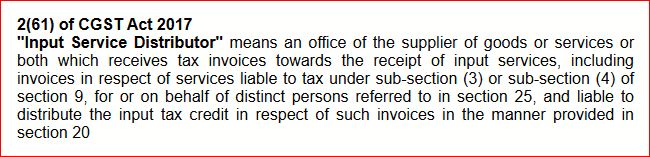

(viii)

Input Service Distributor

, whether or not separately registered under

this Act;

, whether or not separately registered under

this Act;

*(ix) persons who supply goods or services or both, other than supplies specified

under sub-section (5) of section 9, through such

electronic commerce operator

who is required to collect tax at source under

section 52;

who is required to collect tax at source under

section 52;

(x) every electronic commerce operator; 1[who is required to collect tax at source under section 52]

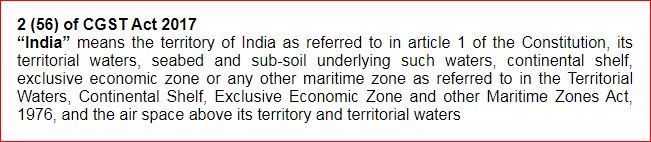

(xi) every person supplying online information and data base access or retrieval

services from a place outside

India

to a person in India, other than a

registered person

to a person in India, other than a

registered person

;

[helldod2omit[and]helldod]

;

[helldod2omit[and]helldod]

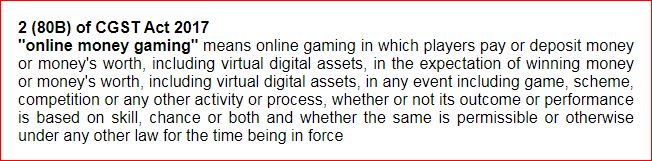

3[(xia) every person supplying

online money gaming

online

money gaming from a place outside India to a person in India; and]

online

money gaming from a place outside India to a person in India; and]

(xii) such other person or class of persons as may be notified by the

Government

on the recommendations of the

Council

on the recommendations of the

Council

.

.