of capital goods

of capital goods

for producing quality goods and

services

for producing quality goods and

services

and enhance India's manufacturing competitiveness.

and enhance India's manufacturing competitiveness.Foreign Trade Policy 2015-20

CHAPTER-5

EXPORT PROMOTION CAPITAL GOODS (EPCG) SCHEME

(Relevant Procedure Chapter 5)

5.00 Objective

The objective of the EPCG Scheme

is to facilitate import

of capital goods

for producing quality goods and

services

and enhance India's manufacturing competitiveness.

5.01 EPCG Scheme

*(a) EPCG Scheme allows import of capital goods

(except those specified in

negative list in Appendix 5 F) for pre- roduction, production and

post-production at zero customs duty. Capital goods imported under EPCG

Authorisation for physical exports are also exempt from IGST and

Compensation Cess upto 8[30.06.2022]

old[7[31.03.2022]]

old[6[30.09.2021]]

old[ 5[31.03.2021]]

old[3[31.03.2020]]

old[2[31.03.2019]]

old[1[01.10.2018]]

old[31.03.2018] only, leviable thereon under the

subsection(7) and subsection (9) respectively, of section 3 of the

Customs Tariff Act, 1975 (51 of 1975), as provided in the notification

issued by Department of Revenue. Alternatively, the Authorisation holder

may also procure Capital Goods from indigenous sources in accordance

with provisions of paragraph 5.07 of FTP. Capital goods for the purpose

of the EPCG scheme shall include:

(i) Capital Goods as defined in Chapter 9 including in CKD/SKD condition thereof;

(ii) Computer systems and software which are a part of the Capital Goods being imported;

(iii) Spares

, moulds, dies, jigs,

fixtures, tools & refractories; and

, moulds, dies, jigs,

fixtures, tools & refractories; and

(iv) Catalysts for initial charge plus one subsequent charge.

(b) Import of capital goods for Project Imports notified by Central Board of Excise and Customs is also permitted under EPCG Scheme.

(c) Import under EPCG Scheme shall be

subject to an export obligation

equivalent to 6 times of duties, taxes

and cess saved on capital goods, to be fulfilled in 6 years reckoned

from date of issue of Authorisation

equivalent to 6 times of duties, taxes

and cess saved on capital goods, to be fulfilled in 6 years reckoned

from date of issue of Authorisation

. 4[However,

in case the validity period for import expires during 1st February, 2020

to 31st July, 2020, the validity stands automatically extended by

further 6 months from the date of such expiry]

. 4[However,

in case the validity period for import expires during 1st February, 2020

to 31st July, 2020, the validity stands automatically extended by

further 6 months from the date of such expiry]

(d) Authorisation shall be valid for import for 18 months from the date of issue of Authorisation. Revalidation of EPCG Authorisation shall not be permitted.

(e) In case Integrated Tax and Compensation Cess are paid in cash on imports under EPCG, incidence of the said Integrated Tax and Compensation Cess would not be taken for computation of net duty saved provided Input Tax Credit is not availed.

(f) Deleted.

(g) Deleted.

(h) Import of items which are restricted

for import shall be permitted under EPCG Scheme only after approval from

Exim Facilitation Committee (EFC) at DGFT Headquarters.

for import shall be permitted under EPCG Scheme only after approval from

Exim Facilitation Committee (EFC) at DGFT Headquarters.

(i) If the

goods proposed to be exported under EPCG authorisation are restricted

for export

, the EPCG authorization shall be issued only after approval

for issuance of export authorisation from Exim Facilitation Committee at

DGFT Headquarters.

, the EPCG authorization shall be issued only after approval

for issuance of export authorisation from Exim Facilitation Committee at

DGFT Headquarters.

5.02 Coverage

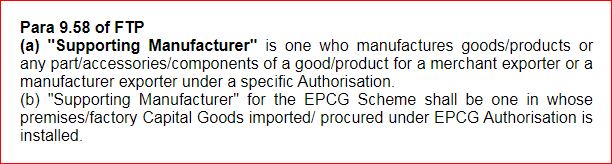

(a) EPCG

scheme covers manufacturer exporters

with or without supporting manufacturer

with or without supporting manufacturer

(s), merchant exporters

(s), merchant exporters

tied to supporting manufacturer(s)

and service providers

tied to supporting manufacturer(s)

and service providers

. Name of supporting manufacturer(s) shall be

endorsed on the EPCG Authorisation before installation of the capital goods

in the factory / premises of the supporting manufacturer (s). In

case of any change in supporting manufacturer (s) the RA Regional Authority shall intimate

such change to jurisdictional Customs Authority of existing as well as

changed supporting manufacturer(s) and the Customs at port of

registration of Authorisation

.

. Name of supporting manufacturer(s) shall be

endorsed on the EPCG Authorisation before installation of the capital goods

in the factory / premises of the supporting manufacturer (s). In

case of any change in supporting manufacturer (s) the RA Regional Authority shall intimate

such change to jurisdictional Customs Authority of existing as well as

changed supporting manufacturer(s) and the Customs at port of

registration of Authorisation

.

(b) Export Promotion Capital Goods (EPCG) Scheme also covers a service provider who is designated / certified as a Common Service Provider (CSP) by the DGFT, Department of Commerce or State Industrial Infrastructural Corporation in a Town of Export Excellence subject to provisions of Foreign Trade Policy/Handbook of Procedures with the following conditions:-

(i) Export

by users of the common

service, to be counted towards fulfillment of EO Export Obligation of the CSP Common Service Provider shall

contain the EPCG Authorisation details of the CSP Common Service Provider in the respective

Shipping bills and concerned RA Regional Authority must be informed about the details of

the Users prior to such export;

(ii) Such export will not count towards

fulfillment of specific export obligations

in respect of other EPCG

Authorisations (of the CSP Common Service Provider/User); and

(iii) Authorisation holder shall be required to submit Bank Guarantee (BG) which shall be equivalent to the duty saved. BG Bank Guarantee can be given by CSP Common Service Provider or by any one of the users or a combination thereof, at the option of the CSP Common Service Provider.

5.03 Actual User

Condition

Condition

Imported

capital goods

shall be subject to Actual User condition till export

obligation is completed and EODC Export Obligation Discharge Certificate is granted.

5.04 Export Obligation (EO)

Following conditions shall apply to the fulfilment of EO Export Obligation:-

(a) EO Export Obligation shall be fulfilled by the

authorisation holder through export of goods which are manufactured by

him or his supporting manufacturer

/ services

rendered by him, for which

the EPCG authorisation has been granted.

(b) EO Export Obligation under the scheme shall be, over

and above, the average level of exports achieved by the applicant

in the

preceding three licensing years

in the

preceding three licensing years

for the same and similar products within

the overall EO Export Obligation period including extended period, if any; except for

categories mentioned in paragraph 5.13(a) of HBP. Such average would be

the arithmetic mean of export

performance in the preceding three

licensing years for same and similar products.

for the same and similar products within

the overall EO Export Obligation period including extended period, if any; except for

categories mentioned in paragraph 5.13(a) of HBP. Such average would be

the arithmetic mean of export

performance in the preceding three

licensing years for same and similar products.

(c) In case of indigenous sourcing of

Capital Goods

, specific EO Export Obligation shall be 25% less than the EO Export Obligation stipulated in

Para 5.01.

(d) Shipments under Advance Authorisation, DFIA Duty Free Import Authorisation, Drawback scheme or reward schemes under Chapter 3 of FTP; would also count for fulfillment of EO Export Obligation under EPCG Scheme.

(e) Export shall be physical export.

However, supplies as specified

in paragraph 7.02 (a), (b), (e), (f) &

(h) of FTP shall also be counted towards fulfillment of export obligation

, along with usual benefits available under paragraph 7.03 of

FTP.

in paragraph 7.02 (a), (b), (e), (f) &

(h) of FTP shall also be counted towards fulfillment of export obligation

, along with usual benefits available under paragraph 7.03 of

FTP.

(f) EO Export Obligation can also be fulfilled by the supply of ITA-I items to DTA, provided realization is in free foreign exchange.

(g) Royalty payments received by the Authorisation holder in freely convertible currency and foreign exchange received for R&D Research and Development services shall also be counted for discharge under EPCG.

(h) Payment received in rupee terms for such Services as notified in Appendix 5D shall also be counted towards discharge of export obligation under the EPCG scheme.

5.05 Deleted

-

5.06 LUT/Bond/BG Bank Guarantee in case of Agro units

LUT/Bond or 15% BG Bank Guarantee, as applicable, may be furnished for EPCG authorisation granted to units in Agri-Export Zones provided EPCG authorisation is taken for export of primary agricultural product(s) notified or their value added variants.

5.07 Indigenous

Sourcing of Capital Goods

and benefits to Domestic Supplier

A person

holding an EPCG authorisation may source capital goods from a domestic

manufacturer. Such domestic manufacturer shall be eligible for deemed

export benefits under paragraph 7.03 of FTP and as may be provided under

GST Rules under the category of deemed exports. Such domestic sourcing

shall also be permitted from EOU

s and these supplies shall be counted

for purpose of fulfilment of positive NFE Net Foreign Exchange by said EOU as provided in

Para 6.09 (a) of FTP.

s and these supplies shall be counted

for purpose of fulfilment of positive NFE Net Foreign Exchange by said EOU as provided in

Para 6.09 (a) of FTP.

5.08 Calculation

of Export Obligation

In case of

direct imports

, EO Export Obligation shall be reckoned with reference to actual duty saved

amount. In case of domestic sourcing, EO Export Obligation shall be reckoned with

reference to notional Customs duties saved on FOR value.

5.09 Incentive for early EO Export Obligation fulfilment

With a view

to accelerating exports

, in cases where Authorisation holder has

fulfilled 75% or more of specific export obligation and 100% of Average

Export Obligation till date, if any, in half or less than half the

original export obligation period specified, remaining export obligation

shall be condoned and the Authorisation redeemed by RA Regional Authority concerned.

However no benefit under Para 5.21 of HBP shall be permitted where

incentive for early EO Export Obligation fulfillment has been availed.

5.10 Reduced EO Export Obligation for Green Technology Products

For exporters of Green Technology Products, Specific EO Export Obligation shall be 75% of EO Export Obligation as stipulated in Para 5.01. There shall be no change in average EO Export Obligation imposed, if any, as stipulated in Para 5.04. The list of Green Technology Products is given in Para 5.29 of HBP.

5.11 Reduced EO Export Obligation for North East Region and Jammu & Kashmir

For units located in Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura and Jammu & Kashmir, specific EO Export Obligation shall be 25% of the EO Export Obligation, as stipulated in Para 5.01. There shall be no change in average EO Export Obligation imposed, if any, as stipulated in Para 5.04.

5.12 Post Export EPCG Duty Credit Scrip(s)

(a) Post Export EPCG Duty Credit Scrip(s) shall be available to exporters who intend to import capital goods

on full payment of applicable duties,

taxes and cess in cash and choose to opt for this scheme.

(b) Basic Customs duty paid on Capital Goods shall be remitted in the form of freely transferable duty credit scrip(s), similar to those issued under Chapter 3 of FTP.

(c) Specific EO Export Obligation shall be 85% of the applicable specific EO Export Obligation under the EPCG Scheme. However, average EO Export Obligation shall remain unchanged.

(d) Duty remission shall be in proportion to the EO Export Obligation fulfilled.

(e) All provisions for utilization of scrips issued under Chapter 3 of FTP shall also be applicable to Post Export EPCG Duty Credit Scrip (s).

(f) All provisions of the existing EPCG Scheme shall apply insofar as they are not inconsistent with this scheme.

Refer Public Notice No. 71/2015-20 Dated 31/01/2019

1.Substituted Vide:- Notification No.54/2015-2020 Dated 22/03/2018

2.Substituted Vide:- Notification No. 35/2015-2020 Dated 26/09/2018

3.Substituted Vide:- Notification No. 57/2015-2020 Dated 20/03/2019

4. Inserted Vide Notification No. 57/2015-2020 Dt.31/03/2020

5.Substituted Vide Notification No. 57/2015-2020 Dt.31/03/2020

6. Substituted Vide Notification No. 60/2015-2020 Dt.31/03/2020

7. Substituted Vide Notification No. 33/2015-2020 Dt.28/09/2021

8. Substituted Vide Notification No. 66/2015-2020 Dt.01/04/2022