of inputs for export

production, including replenishment of inputs or duty remission.

of inputs for export

production, including replenishment of inputs or duty remission.Foreign Trade Policy 2015-20

CHAPTER-4

DUTY EXEMPTION / REMISSION SCHEMES

(Relevant Procedure Chapter 4)

4.00 Objective

Schemes

under this Chapter enable duty free import

of inputs for export

production, including replenishment of inputs or duty remission.

4.01 Schemes

(a) Duty Exemption Schemes. The Duty Exemption schemes consist of the following:• Advance Authorisation (AA) (which will include Advance Authorisation for Annual Requirement).

• Duty Free Import Authorisation (DFIA).

(b) Duty Remission Scheme. Duty Drawback (DBK) Scheme, administered by Department of Revenue.

9[(c) Scheme for Rebate on State and Central Taxes and Levies (RoSCTL), as notified by the Ministry of Textiles on 07.03.2019, and implemented by the DGFT.]

15[(d) Scheme for Rebate of State Levies (RoSL), as notified in para 6.3 of Ministry of Textiles Notification No. 14/26/2016-IT (Vol-II) dated 07.03.2019 and as amended vide notification No. 12015/11/2020-TTP dated 09.06.2020 will be implemented by the DGFT in scrip mode, for which procedure will be laid down separately]

18[(e) Scheme for Remission of Duties and Taxes on Exported Products (RoDTEP) notified by Department of Commerce and administered by Department of Revenue.]

4.02 Applicability of Policy & Procedures

Authorisation

under this Chapter shall be issued in accordance with the

Policy and Procedures in force on the date of issue of the Authorisation.

under this Chapter shall be issued in accordance with the

Policy and Procedures in force on the date of issue of the Authorisation.

4.03 Advance Authorisation

(a) Advance Authorisation is issued to allow duty free import of input, which is physically incorporated in export product (making normal allowance for wastage). In addition, fuel, oil, catalyst which is consumed / utilized in the process of production of export product, may also be allowed.(b) Advance Authorisation is issued for inputs in relation to resultant product, on the following basis: (i) As per Standard Input Output Norms (SION) notified (available in Hand Book of Procedures); OR

(ii) On the basis of self declaration as per paragraph 4.07 of Handbook of Procedures. OR

(iii) Applicant

specific prior fixation

of norm by the Norms Committee. OR

specific prior fixation

of norm by the Norms Committee. OR

(iv) On the basis of Self Ratification Scheme in terms of Para 4.07A of Foreign Trade Policy.

4.04 Advance Authorisation for Spices

Duty free import

of spices covered under Chapter-9 of ITC (HS) shall be permitted

only for activities like crushing/grinding / sterilization/ manufacture

of oils or oleoresins. Authorisation

shall not be available for simply

cleaning, grading, re-packing etc.

of oils or oleoresins. Authorisation

shall not be available for simply

cleaning, grading, re-packing etc.4.04A A Special Advance Authorisation Scheme for export of Articles of Apparel and Clothing accessories.

Duty free imprt of fabric under 'Special Advance Authorisation Scheme for export of Articles of Apparel and Clothing Accessories' shall be allowed, as per Customs Notification issued for this scheme, for export of items covered under Chapter 61 and 62 of ITC(HS) Classification of Export and Import, subject to the following terms and conditions:(i) The authorisation shall be issued based on Standard Input Output Norms (SION) or prior fixation of norms by Norms Committee.

(ii) The authorisation shall be issued for the import of relevant fabrics including inter lining only as input. No other input, packing material, fuel, oil and catalyst shall be allowed for import under this authorisation.

(iii) Exporters shall be eligible for All Industry Rate of Duty Drawback, for non fabric inputs, as determined by Central Government for this scheme. For the purpose of value addition norm of Para 4.08 of FTP, the value of any other input used on which benefit of Drawback is claimed or intended to be claimed shall be equal to 22% of the FOB value of export realised. Minimum value addition shall be as per Para 4.09 of FTP.

(iv) Where the exporter desires to claim drawback determined and fixed by Jurisdictional Customs Authority (brand rate), he shall follow Para 4.15 of FTP regarding declarations to be made in application for the authorisation and make export under claim for brand rate. In such cases the value addition shall be as per Para 4.08 of FTP. Minimum value addition shall be as per Para 4.09 of FTP.

(v) authorisation, and the fabric

imported, shall be subject to actual user

condition. The same shall be

non transferable even after completion of export obligation

condition. The same shall be

non transferable even after completion of export obligation

. However

fabric imported may be transferred for job work in terms of provisions

of GST Acts under intimation to the Customs authority at the port of

registration (excluding to units located in areas eligible for area

based exemption from Central Excise Duty). Invalidation of the

Authorisation shall not be permitted.

. However

fabric imported may be transferred for job work in terms of provisions

of GST Acts under intimation to the Customs authority at the port of

registration (excluding to units located in areas eligible for area

based exemption from Central Excise Duty). Invalidation of the

Authorisation shall not be permitted.

(vi) The fabric imported shall be subject to pre-import condition and it shall be physically incorporated in the export product (making normal allowance for wastage). Only Physical exports shall fulfil the export obligation.

(vii) Provisions of paragraphs 4.02, 4.05(a), 4.13(i), 4.13(ii), 4.14, 4.15, 4.17, 4.19, 4.21(i), 4.21(ii), 4.21 (iii), 4.21(v), 4.22(i), and 4.24 of Foreign Trade Policy shall be applicable in so far as they are not inconsistent with this scheme.

4.05 Eligible

Applicant

/ Export

/ Supply

/ Supply

or

merchant exporter

or

merchant exporter

tied to supporting manufacturer

tied to supporting manufacturer

.

.(b) Advance Authorisation for pharmaceutical products manufactured through Non-Infringing (NI) process (as indicated in paragraph 4.18 of Handbook of Procedures) shall be issued to manufacturer exporter only.

(c) Advance Authorisation shall be issued for:

(i) Physical export (including export to SEZ);

(ii) Intermediate supply; and/or

(iii) Supply of goods to the categories mentioned in paragraph 7.02 (b), (c), (e), (f), (g) and (h) of this FTP.

(iv) Supply of 'stores

' on board of

foreign going vessel / aircraft, subject to condition that there is

specific Standard Input Output Norms in respect of item supplied.

' on board of

foreign going vessel / aircraft, subject to condition that there is

specific Standard Input Output Norms in respect of item supplied.

4.06 Advance Authorisation for Annual Requirement

(i) Advance Authorisation for Annual Requirement shall only be issued for items notified in Standard Input Output Norms (SION), and it shall not be available in case of adhoc norms under paragraph 4.03 (b)(ii) of FTP.(ii) Advance Authorisation for Annual Requirement shall also not be available in respect of SION where any item of input appears in Appendix 4-J.

4.07 Eligibility Condition to obtain Advance Authorisation for Annual Requirement

(i) Exporters having past export

performance (in at least preceding two

financial years) shall be entitled for Advance Authorisation for Annual

requirement.\(ii) Entitlement in

terms of CIF value of imports

shall be upto 300% of the FOB value of

physical export and / or FOR value of deemed export in preceding

financial year or Rs 1 crore, whichever is higher.

4.07A Self Ratification Scheme

i. Where there is no SION/valid Adhoc Norms for an export product and where SION has been notified but exporter intends to use additional inputs in the manufacturing process, eligible exporter can apply for an Advance Authorisation under this scheme on self declaration and self ratification basis. RA Regional Authority may issue Advance Authorisations and such cases need not be referred to Norms Committees for ratification of norms. Application under this scheme shall be made along with a Certificate from Chartered Engineer in the prescribed format.

ii. A Certificate from a Chartered Engineer

who has been not been penalised in the last five years under FT D&R) Act

1992, Customs Act 1962, Central Excise Act 1944, GST Acts and allied

acts and rules made there under shall only be accepted for grant of

Authorisation

under this scheme.

iii. Detailed procedure for administering

the scheme shall be prescribed

in the Handbook of Procedures.

in the Handbook of Procedures.

iv. An exporter (manufacturer or merchant) who holds AEO Authorised Economic Operator Certificate under Common Accreditation Programme of CBEC is eligible to opt for this scheme.

v. The scheme shall not be available for the following export products.

a) All items covered under Chapter-

to 24 and Chapter-71 of ITC(HS) Classification;

b) Biotechnology items and related products; and

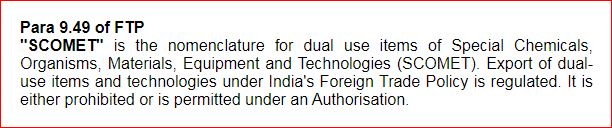

c) SCOMET

items.

items.

vi. The scheme shall not be available for the following inputs.

a) All vegetable / edible oils classified

under Chapter-15 and all types of oilseeds classified under Chapter- 2

of ITC (HS) book;

b) All types of cereals classified under Chapter-10 of ITC (HS) book;

c) Horn, hoof and any other organ of animal;

d) Wild animal

products, organs and waste thereof;

products, organs and waste thereof;

e) Honey;

f) All items with basic customs duty of 30% or more;

g) All types of fruits/ nuts/ vegetables classified under Chapter-7 and

Chapter-8 of ITC (HS) book;

h) Items covered under heading 2515, 2516, 3301, 3302, 3303 6801 and

6802 of ITC(HS) Classification; i) Items covered under Chapter 50 to 63

of ITC(HS) classification.

j) Acetic Anhydride, Ephedrine and Pseudoephedrine; k) Vitamins;

l) Biotechnology items and related products;

m) Insecticides, Rodenticides, Fungicides, herbicides, Anti sprouting

products, and plant growth regulators, disinfectants and similar

products of all forms, types and grades;

n) Waste/Scrap of all types; and o) Second hand goods.

vii. Inputs imported shall be subject to

pre import condition and they shall be physically incorporated in the

export

product (making normal allowance for wastage). In case of local

procurement under invalidation/ARO Advance Release Order, the inputs shall be procured prior

to manufacture

of export item and shall be physically incorporated in

the export product.

viii. Wherever value of by-products and recoverable wastage generated during manufacturing process is more than 5% of CIF value, corresponding quantity of main input shall be reduced from the entitlement to the extent that value of disallowed quantity is equal to the value of by-products and recoverable wastage generated during manufacturing process.

ix. DGFT or any person authorised by him may conduct audit of the manufacturer. The frequency and manner of audit shall be prescribed by DGFT in Handbook of Procedures. The manufacturer shall be required to provide the necessary facility to verify the books of account/other documents as required, give information and assistance for timely completion of the audit. Non-availability of production and consumption documents/data shall be treated as misdeclaration and indulgence in fraudulent activities and shall be penalised under FT(D&R) Act, as amended and rules made there under.

x. DGFT or any person authorised by him may initiate special audit, considering the nature and complexity of the case and revenue of government, if he is of the opinion at any stage of scrutiny/enquiry/investigation that the norms have not been claimed correctly or the excess benefit has been availed. Special audit can be conducted even if the manufacturer has already been audited before.

xi. If the audit results in detection of misdeclaration and/or instances of claiming of inputs which are not used in manufacturing process or excess quantity of inputs than consumed, demand and recovery actions will be initiated in addition to initiation of action against the authorisation holder, manufacturer and Chartered Engineer in terms of Foreign Trade Development and Regulation Act 1992 and/or Customs Act 1962, as amended and rules made there under.

xii. In cases where Chartered Engineer has not exercised due diligence or has willfully become party to misdeclaration action will be initiated under against such person under FT(D&R) Act 1992, as amended and rules made there under. In addition, such cases shall also be referred to 'The Institute of Engineers India for taking action as warranted under the bylaws of the institute.

xiii. All the provisions applicable for Advance Authorisation Scheme shall be applicable to this scheme also in so far they are not inconsistent with this scheme.

4.08 Value Addition

Value Addition for the purpose of this Chapter (except for Gems and Jewellery sector for which value addition is prescribed

in paragraph 4.38 of FTP)

shall be:-VA Value Addition =A-B/Bx100, where

A =FOB value of export realized/FOR value of supply received.

B =CIF value of inputs covered by Authorisation

, plus value of any other

input used on which benefit of DBK is claimed or intended to be claimed.

4.09 Minimum Value Addition

(i) Minimum value addition required to be achieved under Advance Authorisation is 15%.

Products where value addition could be less than 15% are

given in Appendix 4D.4.10 Import

of

Mandatory Spares

Import of

mandatory spares which are required to be exported / supplied with the

resultant product shall be permitted duty free to the extent of 10% of

CIF value of Authorisation

.

4.11 Ineligible categories of import on Self Declaration basis

(a) Import of following products shall not be permissible on self- declaration basis:(i) All vegetable / edible oils classified under Chapter-15 and all types of oilseeds classified under Chapter- 2 of ITC (HS) book;

(ii) All types of cereals classified under Chapter-10 of ITC (HS) book;

(iii) All Spices other than light black pepper (light berries) having a basic customs duty of more than 30%, classified under Chapter-9 and 12 of ITC (HS) book;

(iv) All types of fruits/ vegetables having a basic customs duty of more than 30%, classified under Chapter-7 and Chapter-8 of ITC (HS) book;

(v) Horn, Hoof and any other organ of animal;

(vi) Honey;

(vii) Rough Marble Blocks/Slabs; and

(viii) Rough Granite. (ix) Vitamins except for use in pharmaceutical industry.

(b) For export

of perfumes, perfumery

compounds and various feed ingredients containing vitamins, no

Authorisation

shall be issued by Regional Authority

under

paragraph 4.07 of Handbook of Procedures and applicants

shall be

required to apply under paragraph 4.06 of Hand Book of Procedures to the

Norms Committee.

under

paragraph 4.07 of Handbook of Procedures and applicants

shall be

required to apply under paragraph 4.06 of Hand Book of Procedures to the

Norms Committee.

(c) Where export and/or import of biotechnology items and related products are involved, Authorisation under paragraph 4.07 of Handbook of Procedures shall be issued by Regional Authority only on submission of a "No Objection Certificate" from Department of Biotechnology.

4.12 Accounting of Input

(i) Wherever SION permits use of either (a) a generic input or (b) alternative input, unless the name of the specific input together with quantity [which has been used in manufacturing the export product] gets indicated / endorsed in the relevant shipping bill and these inputs, so endorsed, within quantity specified and match the description in the relevant bill of entry, the concerned Authorisation will not be redeemed. In other words, the name/description of the input used (or to be used) in the Authorisation must match exactly with the name/description endorsed in the shipping bill.(ii) In addition, if in any SION, a

single quantity has been indicated against a number of inputs

(more than one input), then quantities of such inputs to be permitted

for import shall be in proportion to the quantity of these inputs

actually used/consumed in production, within overall quantity against

such group of inputs. Proportion of these inputs actually

used/consumed in production of export

product shall be clearly indicated

in shipping bills.

(iii) At the time of discharge of export obligation

(issue of EODC Export Obligation Discharge Certificate) or at the time of redemption, Regional

Authority shall allow only those inputs which have been specifically

indicated in the shipping bill together with quantity.

(iv) The above provisions will also be

applicable for supplies to SEZs and supplies made under Deemed exports.

Details as given above will have to be indicated in the relevant Bill of

Export, ARE-3 Application for Removal of Excisable Goods from a factory or a warehouse to another arehouse, Central Excise certified Invoice / import document / Tax

Invoice for export prescribed

under the GST rules

4.13 Pre-import condition in certain cases

(i) DGFT may, by Notification, impose pre-import condition for inputs under this Chapter.(ii) Import

items subject to pre-import

condition are listed in Appendix 4-J or will be as indicated in Standard

Input Output Norms (SION).

(iii) Import of drugs from unregistered sources shall have pre-import condition.

4.14 Details of Duties exempted

6[Imports under Advance Authorisation are exempted from payment of Basic Customs Duty, Additional Customs Duty, Education Cess, Anti-dumping Duty, Countervailing Duty, Safeguard Duty, Transition Product Specific Safeguard Duty, wherever applicable. Import against supplies covered under paragraph 7.02 (c) and (g) of FTP will not be exempted from payment of applicable Anti-dumping Duty, Countervailing Duty, Safeguard Duty and Transition Product Specific Safeguard Duty, if any. However, imports under Advance Authorisation are also exempt from whole of the Integrated Tax and Compensation Cess leviable under sub-section (7) and sub-section (9) respectively, of section 3 of the Customs Tariff Act, 1975 (51 of 1975), as may be provided in the notification issued by Department of Revenue, for making physical exports or domestic supplies notified at Sr Nos. 1, 2 and 3 of the table contained in Notification no. 48/2017-Central Tax dated 18.10.2017 issued by Department of Revenue. Imports against Advance Authorisations are exempted from Integrated Tax and Compensation Cess upto * 21[30.06.2022] old[19[31.03.2022]] old[17[30.09.2021]] old[12[31.03.2021] old[8[31.03.2020]] old[31.03.2019] only.]old[Imports under Advance Authorisation are exempted from payment of Basic Customs Duty, Additional Customs Duty, Education Cess, Anti-dumping Duty, Countervailing Duty, Safeguard Duty, Transition Product Specific Safeguard Duty, wherever applicable. Import against supplies covered under paragraph 7.02 (c), (d) and (g) of FTP will not be exempted from payment of applicable Anti-dumping Duty, Countervailing Duty, Safeguard Duty and Transition Product Specific Safeguard Duty, if any. However, imports under Advance Authorisation for physical exports are also exempt from whole of the integrated tax and Compensation Cess leviable under sub-section (7) and sub-section (9) respectively, of section 3 of the Customs Tariff Act, 1975 (51 of 1975), as may be provided in the notification issued by Department of Revenue, and such imports shall be subject to pre-import condition. Imports against Advance Authorisations for physical exports are exempted from Integrated Tax and Compensation Cess upto 3[31.03.2019]] old[31.03.2018] only.]

Refer:- Circular No. 16/2023-Customs Dated 07/06/2023

4.15 Admissibility of Drawback

Drawback as

per rate determined and fixed by Customs authority in terms of DoR Department of Revenue Rules

shall be available for duty paid imported or indigenous inputs (not

specified in the norms) used in the export

product. For this purpose,

applicant

shall indicate clearly details of duty paid input in the

application for Advance Authorisation. As per details mentioned in the

application, Regional Authority

shall also clearly endorse details of

such duty paid inputs in the condition sheet of the Advance Authorisation.

4.16 Actual User

Condition for Advance Authorisation

(i) Advance

Authorisation and / or material imported under Advance Authorisation

shall be subject to 'Actual User' condition. The same shall not be

transferable even after completion of export obligation

. However,

Authorisation holder will have option to dispose of product manufactured

out of duty free input once export obligation is completed.

(ii) In case where CENVAT/input tax

credit facility on input has been availed for the exported goods, even

after completion of export obligation, the goods imported against such

Advance Authorisation shall be utilized only in the manufacture

of

dutiable goods whether within the same factory or outside (by a

supporting manufacturer

). For this, the Authorisation holder shall

produce a certificate from 7delete[either the jurisdictional Customs Authority

or] Chartered Accountant, at the option of the exporter, at the time of

filing application for Export Obligation Discharge Certificate to

Regional Authority concerned.

(iii) Waste / Scrap arising out of manufacturing process, as allowed, can be disposed off on payment of applicable duty even before fulfillment of export obligation.

4.17 Validity

Period for Import

and its Extension

Validity

period for import under Advance Authorisation shall be as prescribed

in

Handbook of Procedures.

4.18

Importability/Export ability of items that are Prohibited

/Restricted

/Restricted

/

STE State Trading Enterprise

/

STE State Trading Enterprise

(i) No

export

or import of an item shall be allowed under Advance Authorisation

/ DFIA Duty Free Import Authorisation if the item is prohibited for exports or imports respectively.

Export of a prohibited item may be allowed under Advance Authorisation

provided it is separately so notified, subject to the conditions given

therein.

(ii) Items reserved for imports by STEs cannot be imported against Advance Authorisation / DFIA Duty Free Import Authorisation. However, those items can be procured from STEs against ARO Advance Release Order or Invalidation letter. STEs are also allowed to sell goods on High Sea Sale basis to holders of Advance Authorisation / DFIA Duty Free Import Authorisation holder. STEs are also permitted to issue "No Objection Certificate(NOC)" for import by Advance Authorisation / DFIA Duty Free Import Authorisation holder. Authorisation Holder would be required to file Quarterly Returns of imports effected against such NOC to concerned STE State Trading Enterprise and STE State Trading Enterprise would submit half-yearly import figures of such imports to concerned administrative Department for monitoring with a copy endorsed to DGFT.

(iii) Items reserved for export by STE State Trading Enterprise can be exported under Advance Authorisation / DFIA Duty Free Import Authorisation only after obtaining a 'No Objection Certificate' from the concerned STE State Trading Enterprise.

(iv) Import of restricted items shall be allowed under Advance Authorisation/ DFIA Duty Free Import Authorisation.

(v) Export of restricted / SCOMET

items

however, shall be subject to all conditionalities or requirements of

export authorisation or permission, as may be required, under Schedule 2

of ITC (HS).

4.19 Free of Cost Supply by Foreign Buyer

Advance

Authorisation shall also be available where some or all inputs are

supplied free of cost to exporter by foreign buyer. In such cases,

notional value of free of cost input shall be added in the CIF value of

import

and FOB value of export for the purpose of computation of value

addition. However, realization of export proceeds will be equivalent to

an amount excluding notional value of such input.

4.20 Domestic Sourcing of Inputs

(i) Holder

of an Advance Authorisation / Duty Free Import Authorisation can procure

inputs from indigenous supplier/ State Trading Enterprise

/EOU

/EOU

/EHTP Electronic Hardware Technology Park/BTP Biotechnology Park/STP

in lieu of direct import. Such procurement can be against Advance

Release Order (ARO), or Invalidation Letter.

/EHTP Electronic Hardware Technology Park/BTP Biotechnology Park/STP

in lieu of direct import. Such procurement can be against Advance

Release Order (ARO), or Invalidation Letter.

(ii) When domestic supplier intends to

obtain duty free material for inputs through Advance Authorisation for

supplying resultant product to another Advance Authorisation / DFIA Duty Free Import Authorisation /

EPCG Authorisation, Regional Authority

shall issue Invalidation Letter.

(iii) Regional Authority shall issue Advance Release Order if the domestic supplier intends to seek refund of duties exempted through Deemed Exports mechanism as per provisions under Chapter-7 of FTP.

(iv) Regional Authority may issue Advance

Release Order or Invalidation Letter at the time of issue of

Authorisation

simultaneously or subsequently.

(v) Advance Authorisation holder under DTA can procure inputs from / SEZ units without obtaining Advance Release Order or Invalidation Letter.

(vi) Deleted

(vii) Validity of Advance Release Order / Invalidation Letter shall be co¬terminous with validity of Authorisation.

4.21 Currency

for Realisation of Export

Proceeds.

22[(i) Export proceeds shall be realized in freely convertible currency

or in Indian Rupees as per para 2.53 of FTP, except otherwise specified

.

Provisions regarding realisation and non-realisation of export proceeds

are given in paragraph 2.52, 2.53 and 2.54 of FTP. ]

.

Provisions regarding realisation and non-realisation of export proceeds

are given in paragraph 2.52, 2.53 and 2.54 of FTP. ]

old[(i) Export proceeds shall be realized in freely convertible currency except otherwise specified. Provisions regarding realisation and non realisation of export proceeds are given in paragraph 2.52, 2.53 and 2.54 of FTP.]

(ii) Deleted

(iii) Export to SEZ Units shall be taken

into account for discharge of export obligation

provided payment is

realised from Foreign Currency Account of the SEZ unit.

(iv) Export to SEZ Developers

/

Co-developers can also be taken into account for discharge of export

obligation even if payment is realised in Indian Rupees.

/

Co-developers can also be taken into account for discharge of export

obligation even if payment is realised in Indian Rupees.

(v) Authorisation holder needs to file Bill of Export for export to SEZ unit / developer / co-developer in accordance with the procedures given in SEZ Rules, 2006.

4.22 Export Obligation Period and its Extension

Period for

fulfilment of export obligation and its extension under Advance

Authorisation shall be as prescribed

in Handbook of Procedures.

4.23 Deleted

-

4.24 Re-import of exported goods under Duty Exemption / Remission Scheme

Goods

exported under Advance Authorisation/ Duty Free Import Authorisation may

be re-imported in same or substantially same form subject to such

conditions as may be specified by Department of Revenue. Authorisation

holder shall also inform about such re-importation to the Regional Authority

which had issued the Authorisation within one month from date

of re-import.

DUTY FREE IMPORT AUTHORISATION SCHEME (DFIA)

4.25 DFIA Duty Free Import Authorisation Scheme

(a) Duty

Free Import Authorisation is issued to allow duty free import

of inputs.

In addition, import of oil and catalyst which is consumed / utilised in

the process of production of export product, may also be allowed.

(b) Provisions of paragraphs 4.12, 4.18, 4.20, 4.21 and 4.24 of FTP

shall be applicable to DFIA Duty Free Import Authorisation also.

1[(c) Export

of white sugar under DFIA Duty Free Import Authorisation is allowed under SION SI.No-E 52 till

30.9.2018 and DFIA Duty Free Import Authorisation in such cases shall be issued only on or after 1.10.2019.

Such DFIAs shall be valid for imports till 30.9.2021]

old[(c) Duty Free Import Authorisation Scheme shall not be available for

import of raw sugar.]

16[(d) Import of Tyres under DFIA Duty Free Import Authorisation scheme is not allowed.]

4.26 Duties Exempted

(i) Duty Free Import Authorisation shall be exempted only from payment of Basic Customs Duty (BCD).

(ii) Deleted

(iii) Drawback as per rate determined and

fixed by Customs authority shall be available for duty paid inputs,

whether imported or indigenous, used in the export product. However, in

case such drawback is claimed for inputs not specified in SION, the

applicant

should have indicated clearly details of such duty paid inputs

also in the application for Duty Free Import Authorisation, and as per

the details mentioned in the application, the Regional Authority should

also have clearly endorsed details of such duty paid inputs in the

condition sheet of the Duty Free Import Authorisation.

4.27 Eligibility

(i) Duty

Free Import Authorisation shall be issued on post export

basis for

products for which Standard Input Output Norms have been notified.

(ii) Merchant Exporter

shall be required

to mention name and address of supporting manufacturer

of the export

product on the export document viz. Shipping Bill/ Bill of Export / Tax

Invoice for export prescribed

under the GST rules.

(iii) Application is to be filed with

concerned Regional Authority

before effecting export under Duty Free

Import Authorisation.

1[(iv) No Duty Free Import Authorisation shall be issued for an input which is

subjected to pre-import condition or where SION prescribes 'Actual User

'

condition or Appendix-4J prescribes pre import condition for such an input.

However, this restriction is not applicable for 'Raw Sugar' on exports made till

30.9.2018.]

old[(iv) No Duty Free Import Authorisation

shall be issued for an input which is subjected to pre-import condition

or where SION prescribes 'Actual User' condition or Appendix-4J

prescribes pre import condition for such an input.]

4.28 Minimum Value Addition

Minimum value addition of 20% shall be required to be achieved.

4.29 Validity &Transferability of DFIA Duty Free Import Authorisation

(i)

Applicant

shall file online application to Regional Authority concerned

before starting export

under DFIA Duty Free Import Authorisation.

(ii) Export shall be completed within 12 months from the date of online filing of application and generation of file number.

(iii) While doing export/supply, applicant shall indicate file number on the export /supply documents viz. Shipping Bill / / Bill of Export / Tax invoice for supply prescribed under GST rules.

(iv) In terms of Para 4.12 of FTP,

Wherever SION permits use of either (a) a generic input or (b)

alternative input, the specific input together with quantity [which has

been used in manufacturing the export product] should be indicated /

endorsed in the relevant Shipping Bill / Bill of Export / Tax invoice

for supply prescribed under GST rules . Only such inputs may be

permitted for import in the authorisation

in proportion to the quantity

of these inputs actually used/consumed in production, within overall

quantity against such generic input/alternative input.

(v) In addition, if in any SION, a single

quantity has been indicated against a number of inputs (more than one

input), then quantities of such inputs to be permitted for import

shall

be in proportion to the quantity of these inputs actually used/consumed

in production and declared in Shipping Bill / Bill of Export / Tax

invoice for supply prescribed under GST rules within overall quantity

against such group of inputs. Proportion of these inputs actually

used/consumed in production of export product shall be clearly indicated

in Shipping Bill / Bill of Export / Tax invoice for supply prescribed

under GST rules.

2[(vi) Separate DFIA Duty Free Import Authorisation shall be issued for each SION]

old[(vi) Separate DFIA Duty Free Import Authorisation shall be issued for each SION and each port.]

2[ (vii) Export under DFIA Duty Free Import Authorisation shall be made from any port listed in Para 4.37 of Handbook of Procedures. However, separate application shall be made for EDI and non-EDI ports. In case export is made from a non-EDI port, separate application shall be made for each non-EDI port.]

old[(vii) Exports under DFIA Duty Free Import Authorisation shall be made from a single port as mentioned in paragraph 4.37 of Handbook of Procedures. ]

(viii) Regional Authority

shall issue

transferable DFIA Duty Free Import Authorisation with a validity of 12 months from the date of issue.

11[However, for all DFIAs (including transferable DFIAs),

where the validity for import is expiring between 01.02.2020 and

31.07.2020, the validity stands automatically extended by six months

from the date of expiry.]

No further revalidation shall be granted by Regional Authority.

4.30 Sensitive Items under Duty Free Import Authorisation

(a) In respect of following inputs, exporter shall be required to provide declaration with regard to technical characteristics, quality and specification in Shipping Bill:

"Alloy steel including Stainless Steel, Copper Alloy, Synthetic Rubber, Bearings, Solvent, Perfumes / Essential Oil/ Aromatic Chemicals, Surfactants, Relevant Fabrics, Marble, Articles made of Polypropylene, Articles made of Paper and Paper Board, Insecticides, Lead Ingots, Zinc Ingots, Citric Acid, Relevant Glass fibre reinforcement (Glass fibre, Chopped / Stranded Mat, Roving Woven Surfacing Mat), Relevant Synthetic Resin (unsaturated Polyester Resin, Epoxy Resin, Vinyl Ester Resin, Hydroxy Ethyl Cellulose), Lining Material".

(b) While issuing Duty Free Import

Authorisation, Regional Authority shall mention technical

characteristics, quality and specification in respect of above inputs in

the Authorisation

.

CHEMES FOR EXPORTERS OF GEMSAND JEWELLERY

4.31 Import

of

Input

Exporters

of gems and Jewellery can import / procure duty free (excluding

Integrated Tax and Compensation Cess leviable under Section 3(7) and

3(9) of customs Tariff Act) input for manufacture

of export product.

4.32 Items of Export

Following items, if exported, would be eligible:

5[(i)"Gold jewellery, including partly processed jewellery and articles including

medallions and coins (excluding legal tender coins), whether plain or studded,

containing gold of 8 carats and above up to maximum limit of 22 carats.

Gold religious idols (only gods and goddess) of 8 carats and above (upto 24

carats) subject to the following conditions:

i) Exports would be subject to 100% examination by the Approved Government

Valuer.

ii) Foreign remittance has to be realised within a period of 3 months from the

date of export.

iii) Exporters must submit confirmed export order before effecting export.

iv) Distinction must be made between a religious idol and simply moulded gold

article/ idol.

v) Exports may be allowed only by actual manufacturers of such idols.

The Findings like posts, push backs, locks which help in collating the jewellery

pieces together, containing gold of 3 carats and above up to a maximum limit of

22 carats."]

old[4[(i)Gold jewellery, including partly processed jewellery and articles including medallions and coins (excluding legal tender coins), whether plain or studded, containing gold of 8 carats and above up to a maximum limit of 22 carats.

The Findings like posts, push backs, locks which help in collating the jewellery pieces together, containing gold of 3 carats and above up to a maximum limit of 22 carats.]]

old[(i) Gold jewellery, including partly processed jewellery and articles including medallions and coins (excluding legal tender coins), whether plain or studded, containing gold of 8 carats and above up to a maximum limit of 22 carats]

(ii) Silver jewellery including partly processed jewellery, silverware, silver strips and articles including medallions and coins (excluding legal tender coins and any engineering goods) containing more than 50% silver by weight;

(iii) Platinum jewellery including partly processed jewellery and articles including medallions and coins (excluding legal tender coins and any engineering goods) containing more than 50% platinum by weight.

4.33 Schemes

The schemes

are as follows:

(i) Advance Procurement / Replenishment of Precious Metals from

Nominated Agencies;

(ii) Replenishment Authorisation for Gems;

(iii) Replenishment Authorisation for Consumables

;

;

(iv) Advance Authorisation for Precious Metals.

4.34 Advance Procurement/ Replenishment of Precious Metals from Nominated Agencies

10[(i) Exporter of gold / silver / platinum

jewelery and articles thereof including mountings and findings may

obtain gold / silver / platinum as an input for export

product from

Nominated Agency, in advance or as replenishment after export in

accordance with the procedure specified in this behalf.

Replenishment of gold / silver / platinum will be subject to Customs

notification No. 57/2000-Customs dated 08.05.2000, as amended.]

old[(i) Exporter of gold / silver / platinum jewellery and articles thereof including mountings and findings may obtain gold / silver / platinum as an input for export product from Nominated Agency, in advance or as replenishment after export in accordance with the procedure specified in this behalf. No replenishment of the precious metal shall be available to the exporter/manufacturer where the exporter/manufacturer avails any of the benefits in respect of exported product.

a. CENVAT Credit is availed on inputs or services by the manufacturer.

b. Finished goods stage rebate is availed under Notification No 19/2004-CE (NT) dated 06.09.2004.

c. Input stage rebate is availed in respect of duty of excise paid on the precious metal bar or articles of precious metal under Notification No 21/2004-CE(NT) dated 06.09.2004.

d. Precious metal or articles of precious metal are procured by the manufacturer under rule 19(2) of the Central Excise Rules, 2002.

e. Input Tax Credit is availed on inputs or services or both by the exporter under Chapter V of CGST Act; or refund of ITC or refund of IGST is availed under section 54 of the CGST Act.]

(ii) The export would be subject to

wastage norms and minimum value addition as prescribed

in paragraph 4.60

and 4.61 respectively in the Handbook of Procedures.

*4.35 Replenishment Authorisation for Gems

(i)

Exporter may obtain Replenishment Authorisation for Gems from

Regional Authority

in accordance with procedure specified in Handbook of

Procedures as per the replenishment rate prescribed in Appendix 4F.

Replenishment Authorisation for Gems shall be freely transferable.

(ii) Replenishment Authorisation for Gems

may be issued against export

including that made against supply by

Nominated Agency (paragraph 4.41 of FTP) and against supply by foreign

buyer (paragraph 4.45 of FTP).

(iii) In the case of studded

gold/silver/platinum jewellery and articles thereof, the value of Gem

Replenishment Authorisation shall be on the remaining FOB value of

exports after deducting the value of gold/ silver/ platinum including

admissible wastage. The scale of replenishment and the item of import

will be as prescribed in Appendix 4G.

*4.36

Replenishment Authorisation for Consumables

(i)

Replenishment Authorisation for duty free (excluding Integrated Tax and

Compensation cess leviable under Section 3(7) and 3(9) of Customs Tariff

Act)import of Consumables, Tools and other items namely, Tags and

labels, Security censor on card, Staple wire, Poly bag (as notified by

Customs) for Jewellery made out of precious metals (other than Gold &

Platinum) equal to 2% and for Cut and Polished Diamonds and Jewellery

made out of Gold and Platinum equal to 1% of FOB value of exports of the

preceding year, may be issued on production of Chartered Accountant

Certificate indicating the export performance. However, in case of

Rhodium finished Silver jewellery, entitlement will be 3% of FOB value

of exports of such jewellery. This Authorisation shall be

non-transferable and subject to actual user

condition.

(ii) Application for import of consumables as given above shall be filed

online to the concerned Regional Authority in ANF 4H.

4.37 Advance Authorisation for Precious Metals

(a) Advance Authorisation shall be granted on pre-import basis with 'Actual User' condition for duty free (excluding Integrated Tax and Compensation cess leviable under Section 3(7) and 3(9) of Customs Tariff Act)import of:

(i) Gold of fineness not less than 0.995 and mountings, sockets, frames and findings of 8 carats and above;

(ii) Silver of fineness not less than 0.995 and mountings, sockets, frames and findings containing more than 50% silver by weight;

(iii) Platinum of fineness not less than 0.900 and mountings, sockets, frames and findings containing more than 50% platinum by weight.

(b) Advance Authorisation shall carry an

export obligation

which shall be fulfilled as per procedure indicated in

Chapter 4 of Handbook of Procedures.

(c) Value Addition shall be as per paragraph4.38 of FTP and 4.61 of Handbook of Procedures.

14[(d)

Advance Authorisation

Scheme is not available where the item of export

is 'Gold Medallions and Coins'

or 'Gold jewellery/articles manufactured by fully mechanised process]

4.38 Value Addition

Minimum

Value Addition norms for gems and jewellery sector are given in

paragraph 4.61 of Handbook of Procedures. It would be calculated as

under:

VA Value Addition =A-B/Bx100,where

A = FOB value of the export realised/ FOR

value of supply received.

B= Value of inputs (including domestically procured) such as

gold/silver/platinum content in export product plus admissible wastage

along with value of other items such as gemstone etc. Wherever gold has

been obtained on loan basis, value shall also include interest paid in

free foreign exchange to foreign supplier.

4.39 Wastage Norms

Wastage or manufacturing loss for gold/silver/platinum jewellery shall be admissible as per paragraph 4.60 of Handbook of Procedures.

4.40 DFIA Duty Free Import Authorisation not available

Duty Free Import Authorisation scheme shall not be available for Gems and Jewellery sector.

4.41 Nominated Agencies

(i)

Exporters may obtain gold / silver / platinum from Nominated Agency.

Exporter in EOU

and units in SEZ would be governed by the respective

provisions of Chapter-6 of FTP / SEZ Rules, respectively.

(ii) Nominated Agencies are MMTC Ltd, The Handicraft and Handlooms Exports Corporation of India Ltd, The State Trading Corporation of India Ltd, PEC Project and Equipment Corporation of India Ltd. Ltd, STCL Spices Trading Corporation Limited Ltd, MSTC Metal Scrap Trade Corporation Ltd, and Diamond India Limited.

(iii) Notwithstanding any provision

relating to import

of gold by Nominated Agencies under Foreign Trade

Policy (2015-2020), the import of gold by Four Star and Five Star Houses

with Nominated Agency Certificate is subjected to actual user

condition

and are permitted to import gold as input only for the purpose of

manufacture

and export

by themselves during the remaining validity

period of the Nominated Agency certificate.

(iv) Reserve Bank of India can authorize any bank as Nominated Agency.

(iv) Procedure for import of precious metal by Nominated Agency (other than those authorized by Reserve Bank of India and the Gems & Jewellery units operating under EOU and SEZ schemes) and the monitoring mechanism thereof shall be as per the provisions laid down in Hand Book of Procedures.

(v) A bank authorised by Reserve Bank of India is allowed export of gold scrap for refining and import standard gold bars as per Reserve Bank of India guidelines.

4.42 Import of Diamonds for Certification / Grading & Re- export

Following

agencies are permitted to import diamonds to their laboratories without

any import duty, for the purpose of certification / grading reports,

with a condition that the same should be re-exported with the

certification/grading reports, as per the procedure laid down in Hand

Book of Procedures:

(1) Gemological Institute of America (GIA), Mumbai, Maharashtra.

(2) Indian Diamond Institute, Surat, Gujarat, India.

20[(3) De Beers India Private Ltd, Surat, Gujarat, India.]

old[(3) International Institute of Diamond Grading & Research India Pvt.

Ltd., Surat, Gujarat, India.]

(4) HRD Diamond Institute Private Limited, Mumbai, Maharashtra, India

(5) International Gemological Institute (India) Pvt. Ltd, Bandra Kurla

Complex, Mumbai

23[(6) Gemological Science International (GSI)

Pvt. Ltd., Mumbai, Maharashtra, India.]

4.43 Export of Cut & Polished Diamonds for Certification/ Grading & Re-import

List of authorized laboratories for certification / grading of diamonds of 0.25 carat and above are given in paragraph 4.74 of Handbook of Procedures.

4.44

Export

of

Cut & Polished Diamonds with Re-import Facility at Zero Duty

13[An exporter (with annual export turnover of Rs 5 crores for each of the last

three years) or the authorized offices/agencies in India of laboratories

mentioned under paragraph 4.74 of Hand Book of Procedures may export cut &

polished diamonds (each of 0.25 carat or above) to any o‘f the

agencies/laboratories mentioned under paragraph 4.74 of Handbook of Procedures

with re-import facility at zero duty within 3 months from the date of export.

Such facility of re-import at zero duty will be subject to guidelines issued by

Central Board of Customs & Excise, Department of Revenue.

However, for cases where re-import period is expiring between Feb 1, 2020 to

July 31, 2020, the period of re-import shall be considered automatically

extended by 3 more months.]

old[An exporter

(with annual export turnover of Rs 5 crores for each of the last three

years) or the authorized offices/agencies in India of laboratories

mentioned under paragraph 4.74 of Hand Book of Procedures may export cut

& polished diamonds (each of 0.25 carat or above) to any of the

agencies/laboratories mentioned under paragraph 4.74 of Handbook of

Procedures with re-import facility at zero duty within 3months from the

date of export. Such facility of re-import at zero duty will be subject

to guidelines issued by Central Board of Customs & Excise, Department of

Revenue.]

4.45 Export against Supply by Foreign Buyer

(i) Where

export orders are placed on nominated agencies / status holder

/

exporters of three years standing having an annual average turnover of

Rupees five crores during preceding three financial years, foreign buyer

may supply in advance and free of charge, gold / silver / platinum,

alloys, findings and mountings of gold / silver / platinum for

manufacture

and export.

/

exporters of three years standing having an annual average turnover of

Rupees five crores during preceding three financial years, foreign buyer

may supply in advance and free of charge, gold / silver / platinum,

alloys, findings and mountings of gold / silver / platinum for

manufacture

and export.

(ii) Such supplies can also be in advance

and may involve semi-finished jewellery including findings / mountings /

components

for repairs / re-make and export subject to minimum value

addition as prescribed

under paragraph 4.61 of Handbook of Procedures.

In such cases of export, wastage norms as per paragraph 4.60 of Handbook

of Procedures shall apply.

for repairs / re-make and export subject to minimum value

addition as prescribed

under paragraph 4.61 of Handbook of Procedures.

In such cases of export, wastage norms as per paragraph 4.60 of Handbook

of Procedures shall apply.

(iii) Exports may be made by nominated

agencies directly or through their associates or by status holder /

exporter. Import

and Export of findings shall be on net to net basis.

4.46 Export Promotion Tours/ Export of Branded Jewellery

(i) Nominated Agencies and their associates, with approval of Department of Commerce and with approval of Gem & Jewellery Export Promotion Council (GJEPC), may export gold / silver / platinum jewellery and articles thereof for exhibitions abroad.

(ii) Personal carriage of gold / silver /

platinum jewellery, precious, semi-precious stones, beads and articles

and export

of branded jewellery is also permitted, subject to conditions

as in Handbook of Procedures.

4.47 Personal Carriage of Export /Import Parcels

Personal carriage of gems and jewellery export parcels by foreign bound passengers and import parcels by an Indian importer/foreign national may be permitted as per the Handbook of Procedures.

4.48 Export by PostExport by Post

Export of jewellery through Foreign Post Office including via Speed Post is allowed. The jewellery parcel shall not exceed 20 kgs by weight.

4.49 Private / Public Bonded Warehouse

Private / Public Bonded Warehouses may be set up in SEZ/DTA for import and re-export of cut and polished diamonds, cut and polished coloured gemstones, uncut & unset precious & semi-precious stones, subject to achievement of minimum value addition of 5% by DTA units.

4.49(A)

Import, auction/sale and re-export of rough diamonds by entities, as notified vide RBI Reserve Bank of India Notification 116 of 1st April, 2014, as amended from time to time, on consignment or outright basis, will be permitted in Special Notified Zone (SNZ) administered by the operator of SNZ, under supervision of Customs. The procedure of import, auction/ sale and re¬export of rough diamonds (unsold) would be as specified by CBEC.

4.50 Diamond & Jewellery Dollar Accounts

(a) Firms

and companies dealing in purchase / sale of rough or cut and polished

diamonds / precious metal jewellery plain, minakari and / or studded

with / without diamond and / or other stones with a track record of at

least two years in import

or export

of diamonds / coloured gemstones /

diamond and coloured gemstones studded jewellery / plain gold jewellery

and having an average annual turnover of Rs.3 crore or above during

preceding three licensing years

may also carry out their business

through designated Diamond Dollar Accounts (DDA).

may also carry out their business

through designated Diamond Dollar Accounts (DDA).

(b) Dollars in such accounts available from bank finance and / or export proceeds shall be used only for:

(i) Import / purchase of rough diamonds from overseas/ local sources;

(ii) Purchase of cut and polished diamonds, coloured gemstones and plain gold jewellery from local sources;

(iii) Import / purchase of gold from overseas / nominated agencies and repayment of dollar loans from the bank; and

(iv) Transfer to Rupee Account of exporter. Details of this DDA Diamond Dollar Accounts Scheme are given in Handbook of Procedures.

(c) A non DDA Diamond Dollar Accounts holder is also permitted to

supply cut and polished diamonds to DDA Diamond Dollar Accounts holder, receive payment in

dollars and convert the same into Rupees within 7 days. Cut and polished

diamonds and coloured gemstones so supplied by non-DDA Diamond Dollar Accounts holder will also

be counted towards discharge of his export obligation

and/ or entitle

him to replenishment Authorisation.

4.51 Export of cut & polished precious and semi-precious stones for treatment and re-import

Gems and Jewellery exporters shall be allowed to export cut and polished precious and semi-precious stones for the treatment and re-import as per customs rules and regulations. In case of re-export, the exporter shall be entitled for duty drawback as per rules.

4.52 Re-import of rejected Jewellery

Gems & Jewellery exporters shall be allowed to re-import rejected precious metal jewellery as per paragraph 4.91 of Handbook of Procedures.

4.53

Export

and import

on consignment basis

Gems & Jewellery exporters shall be allowed to export and import diamond, gemstones & jewellery on consignment basis as per Handbook of Procedures and Customs Rules and Regulations.

18[4.54 Scheme Objective and Operating Principles

i. The Scheme's objective is to refund, currently un-refunded:

a. Duties/ taxes / levies, at the Central, State and local level, borne on the

exported product, including prior stage cumulative indirect taxes on goods and

services

used in the production of the exported product and

used in the production of the exported product and

b. Such indirect Duties/ taxes / levies in respect of distribution of exported

product.

ii . The rebate under the Scheme shall not be available in respect of duties and

taxes already exempted or remitted or credited.

iii. The determination of ceiling rates under the Scheme will be done by a

Committee in the Department of Revenue/Drawback Division with suitable

representation of the DoC Department of Commerce/DGFT, line ministries and experts, on the sectors

prioritized by Department of Commerce and Department of Revenue.

iv. The overall budget/outlay for the RoDTEP Scheme would be finalized by the

Ministry of Finance in consultation with Department of Commerce (DoC), taking

into account all relevant factors.

v. The Scheme will operate in a Budgetary framework for each financial year and

necessary calibrations and revisions shall be made to the Scheme benefits, as

and when required, so that the projected remissions for each financial year are

managed within the approved Budget of the Scheme. No provision for remission of

arrears or contingent liabilities is permissible under the Scheme to be carried

over to the next financial year.

vi. The sequence of introduction of the Scheme across sectors, prioritization of

the sectors to be covered, degree of benefit to be given on various items within

the rates set by the Committee and within a ceiling as may be prescribed, on the

per item/total overall benefit amount permissible, within the overall budget/

outlay finalized, will be decided and notified

by the Department of Commerce (DoC) in consultation with Department of Revenue.

vii. Under the Scheme, a rebate would be granted to eligible exporters at a

notified rate as a percentage of FOB value with a value cap per unit of the

exported product, wherever required, on export of items which are categorized

under the notified 8 digit HS Code. However, for certain export items, a fixed

quantum of rebate amount per unit may also be notified. Rates of rebate / value

cap per unit under RoDTEP will be notified in Appendix 4R. In addition to

necessary changes which may be brought in view of budget control measures as

mentioned above, efforts would be made to review the RoDTEP rates on an annual

basis and to notify them well in advance before the beginning of a financial

year.

viii. The rebate allowed is subject to the receipt of sale proceeds within time

allowed under the Foreign Exchange Management Act, 1999 failing which such

rebate shall be deemed never to have been allowed. The rebate would not be

dependent on the realization of export proceeds at the time of issue of rebate.

However, adequate safeguards to avoid any misuse on account of non-realization

and other systemic improvements as in operation under Drawback Scheme, IGST and

other GST refunds relating to exports would also be applicable for claims made

under the RoDTEP Scheme.

ix. Mechanism of Issuance of Rebate: Scheme would be implemented through end to

end digitization of issuance of rebate amount in the form of a transferable duty

credit/electronic scrip (e-scrip), which will be maintained in an electronic

ledger by the Central Board of Indirect Taxes & Customs (CBIC). Necessary rules

and procedure regarding grant of RoDTEP claim under the Scheme and

implementation issues including manner of application, time period for

application and other matters including export realization, export

documentation, sampling procedures, record keeping etc. would be notified by the

CBIC, Department of Revenue on an IT enabled platform with a view to end to end

digitization. Necessary provisions for recovery of rebate amount where foreign

exchange is not realized, suspension/withholding of RoDTEP in case of frauds and

misuse, as well as imposition of penalty will also be built suitably by CBIC.

x. The Scheme will take effect for exports from 1st January 2021. However for

exports made by categories under Para 4.55 (x), (xi) and (xii), the

implementation date will be decided later as per provisions of Para 4.55B.

4.55 Ineligible Supplies/ Items/Categories under the Scheme

The

following categories of exports

/ exporters shall not be eligible for rebate

under RoDTEP Scheme:

i. Export of imported goods covered under paragraph 2.46 of FTP

ii. Exports through trans-shipment, meaning thereby exports that are originating

in third country but trans-shipped through India

iii. Export products which are subject to Minimum export price or export duty

iv. Products which are restricted

for export under Schedule-2 of Export Policy

in ITC (HS)

v. Products which are prohibited

for export under Schedule-2 of Export Policy in

ITC (HS).

vi. Deemed Exports

vii. Supplies of products manufactured by DTA units to SEZ/FTWZ Free Trade and Warehousing Zone units

viii. Products manufactured in EHTP Electronic Hardware Technology Park and BTP Biotechnology Park

ix. Products manufactured partly or wholly in a warehouse under section 65 of

the Customs Act, 1962 (52 of 1962)

x. Products manufactured or exported in discharge of export obligation

against

an Advance Authorization or Duty Free Import Authorization or Special Advance

Authorization issued under a duty exemption scheme of relevant Foreign Trade

Policy

xi. Products manufactured or exported by a unit licensed as hundred per cent

Export Oriented Unit (EOU) in terms of the provisions of the Foreign Trade

Policy

xii. Products manufactured or exported by any of the units situated in Free

Trade Zones or Export Processing Zones or Special Economic Zones

xiii. Products manufactured or exported availing the benefit of the Notification

No. 32/1997-Customs dated 1st April, 1997.

xiv. Exports for which electronic documentation in ICEGATE EDI has not been

generated/Exports from non-EDI ports

xv. Goods which have been taken into use after manufacture

4.55 A

Government, however, reserves the right to modify any of the categories as mentioned above for inclusion or exclusion under the scope of RoDTEP, at a later date.

4.55 B

Inclusion of exports

made by categories mentioned in para 4.55

(x), (xi) and (xii) above and RoDTEP rates for export items under such

categories would be decided based on the recommendations of the RoDTEP

Committee.

4.56 Nature of Rebate

The e-scrips would be used only for payment of duty of Customs leviable under the First Schedule to the Customs Tariff Act, 1975 viz. Basic Customs Duty.

4.57 Monitoring, Audit and Risk Management System

For the purposes of audit and verification, the exporter would be required to keep records substantiating claims made under the Scheme. A monitoring and audit mechanism with an IT based Risk Management System (RMS) would be put in place by the CBIC, Department of Revenue to physically verify the records of the exporters on sample basis. Sample cases for physical verification will be drawn objectively by the RMS, based on risk and other relevant parameters.

4.57 A Broad Level Monitoring

For a broad level monitoring, an Output Outcome framework will be maintained and monitored at regular intervals.

4.58 Residual Issues

Residual issues related to the Scheme arising subsequently shall be considered by an Inter-Ministerial Committee, named as "RODTEP Policy Committee (RPC)" chaired by DGFT (comprising members of Department of Commerce and Department of Revenue), whose decisions would be binding.

4.59 Appendix 4R

The Appendix 4R containing the eligible RoDTEP export items, rates and per unit value caps, wherever applicable is available at the DGFT portal www.dgft.gov.in under the link `Regulatory Updates >RoDTEP'.]

1.Substituted Vide:- Notification No. 57/2015-2020 Dated 28/03/2018

2.Substituted Vide:- Notification No. 13/2015-2020 Dated 20/06/2018

3.Substituted Vide:- Notification No. 35/2015-2020 Dated 26/09/2018

4.Substituted Vide:- Notification No. 43/2015-2020 Dated 05/11/2018

5.Substituted Vide:- Notification No. 44/2015-2020 Dated 30/11/2018

6.Substituted Vide:- Notification No. 53/2015-2020 Dated 10/01/2019

7.Deleted Vide:- Notification No. 53/2015-2020 Dated 10/01/2019

8.Substituted Vide:- Notification No. 57/2015-2020 Dated 20/03/2019

9.Inserted Vide:- Notification No. 59/2015-2020 Dated 29/03/2019

10.Substituted Vide:- Notification No. 16/2015-2020 Dated 02/09/2019

11. Inserted Vide:- Notification No. 57/2015-2020 Dt.31/03/2020

12. Substituted Vide:- Notification No. 57/2015-2020 Dt.31/03/2020

13. Substituted Vide:- Notification No. 15/2015-2020 Dt.25/06/2020

14. Inserted Vide:- Notification No. 25/2015-2020 Dt.10/08/2020

15. Inserted Vide:- Notification No. 37/2015-2020 Dt.06/10/2020

16. Inserted Vide:- Notification No. 38/2015-2020 Dt.06/10/2020

17. Substituted Vide Notification No. 60/2015-2020 Dt.31/03/2020

18. Inserted Vide Notification No. 19/2015-2020 Dt.17/08/2021

19. Substituted Vide Notification No. 33/2015-2020 Dt.28/09/2021

20. Substituted Vide Notification No. 42/2015-2020 Dt.08/11/2021

21. Substituted Vide Notification No. 66/2015-2020 Dt.01/04/2022

22. Substituted Vide:-Notification No. 43/2015-2020 Dated 09.11.2022

23. Inserted Vide Notification No. 56/2015-2020 Dt.07/02/2023