Foreign Trade Policy 2015-20

CHAPTER 2

GENERAL PROVISIONS REGARDING IMPORTS AND EXPORTS

(Relevant Procedure Chapter 2)

2.00 Objective

The general provisions governing import and export of goods and services are dealt with in this chapter.

2.01 Exports and Imports - 'Free', unless regulated

(a) Exports and Imports shall be 'Free' except when regulated by way of 'prohibition', 'restriction' or 'exclusive trading through State Trading Enterprises (STES)' as laid down in Indian Trade Classification (Harmonized System) [ITC (HS)] of Exports and Imports. The list of 'Prohibited', 'Restricted', and STE State Trading Enterprise items can be viewed by clicking on 'Downloads' at http://dgft.gov.in(b) Further, there are some items which are 'free' for import/export, but subject to conditions stipulated in other Acts or in law for the time being in force.

2.02 Indian Trade Classification (Harmonised System) [ITC (HS)] of Exports and Imports.

(a) ITC (HS) is a compilation of codes for all merchandise / goods for export/ import. Goods are classified based on their group or sub-group at 2/4/6/8 digits.(b) ITC (HS) is aligned at 6 digit level with international

Harmonized System goods nomenclature maintained by World Customs

Organization (http://www.wcoomd.org). However, India maintains national

Harmonized System of goods at 8 digit level which may be viewed by

clicking on 'Downloads' at http: //dgft.gov.in

(c) The import/export policies for all goods are indicated against

each item in ITC (HS).Schedule 1 of ITC (HS) lays down the Import Policy

regime while Schedule 2 of ITC (HS) details the Export Policy regime.

(d) Except where it is clearly specified, Schedule 1 of ITC (HS),

Import Policy is for new goods and not for the Second Hand goods. For

Second Hand goods, the Import Policy regime is given in Para 2.31 in

this FTP.

2.03 Compliance of Imports with Domestic Laws

(a) Domestic Laws/ Rules/ Orders/ Regulations/ technical specifications/ environmental/safety and health norms applicable to domestically produced goods shall apply, mutatis mutandis, to imports, unless specifically exempted.(b) However, Goods to be utilized/ consumed in manufacture of export products, as notified by DGFT, may be exempted from domestic standards/ quality specifications.

2.04 Authority to specify Procedures

DGFT may, specify Procedures to be followed by an exporter or importer or by any licensing/Regional Authority (RA) or by any other authority for purposes of implementing provisions of FT (D&R) Act, the Rules and the Orders made there under and FTP. Such procedures, or amendments if any, shall be published by means of a Public Notice. Importer-Exporter Code/e-IEC Electronic Importer-Exporter Code*2.05 Importer-Exporter Code (IEC)

(I) An IEC is a 10-character alpha-numeric number allotted to a person that is mandatory for undertaking any export/import activities. With a view to maintain the unique identity of an entity (firm/company/LLP etc.), consequent upon introduction / implementation of GST, IEC will be equal to PAN and will be separately issued by DGFT based on an application.

3[(a) No export or import

shall be made by any person without obtaining an IEC number unless

specifically exempted. For services exports, IEC shall be necessary

as per the provisions in Chapter 3 only when the service provider is

taking benefits under the Foreign Trade Policy.

(b) Exempt categories and corresponding permanent IEC numbers are given

in Para 2.07 of Handbook of Procedures.

(c) Application process for IEC 8[and updation in IEC] is completely online and

IEC can be

generated by the applicant as per the procedure detailed in the Handbook

of Procedure.]

11[An IEC holder has to ensure that details in its IEC is updated electronically every year, during April-June period. However, for the current year only, this period is extended by another month i.e till 31st August, 2021.

In cases where there are no changes in IEC details same also needs to be confirmed online.]

[10[(d) An IEC holder has to

ensure that details in its IEC is updated electronically every year,

during April-June period. However, for the current year only, this

period is extended by another month i.e. till 31st July, 2021.

In cases where there are no changes in IEC details same also needs to be

confirmed online.]]

old[8[(d) An IEC holder has to ensure that details in its IEC is updated electronically every year, during April-June period. In cases where there are no changes in IEC details same also needs to be confirmed online.]

(e) An IEC shall be de-activated, if it is not updated within the prescribed time. An IEC so de-activated may be activated, on its successful updation. This would however be without prejudice to any other action taken for violation of any other provisions of the FTP.

(f) An EEC may be also be flagged for

scrutiny. IEC holder(s) are required to ensure that any

risks flagged by the system is timely addressed; failing which the EEC

shall be deactivated.]

old[(a) Application for obtaining IEC may be filed online in ANF 2A with

applicable fees and submitted with digital signature.

(b) When an e-IEC Electronic Importer-Exporter Code is approved by the competent authority, applicant

is informed through e-mail that a computer generated e-IEC Electronic Importer-Exporter Code is available

on the DGFT website. By clicking on "Application Status" after having

filled and submitted the requisite details in "Online IEC Application"

webpage, applicant can view and print his e-IEC Electronic Importer-Exporter Code.

(c) The applicant may submit online application with the following

details /documents (scanned copies to be submitted/ uploaded) along with

the IEC application:

(i) Digital photograph of the signatory applicant;

(ii) Copy of the PAN card of the business entity in whose name

Import/Export would be done (Applicant individual in case of

Proprietorship firms);

(iii) Cancelled cheque bearing entity's pre-printed name or Bank

certificate in prescribed format ANF-2A(I)

(d) For modification in IEC, applicants may submit online

application through digital signature (Class-II or Class-Ill), by paying

applicable fees and uploading requisite documents, corresponding to the

changes sought.

(e) Detailed guidelines for applying for e-IEC Electronic Importer-Exporter Code is available at

http://dgft.gov.in/exim/2000/iec anf/iecanf.htm

(II) No Export/Import without IEC:

(i) No export or import shall be made by any person without

obtaining an IEC number unless specifically exempted.

(ii) Exempt categories and corresponding permanent IEC numbers are given

in Para 2.07 of Handbook of Procedures.]

2.06 Mandatory documents for export/import of goods from/into India:

(a) Mandatory documents required for export of goods from India:[Note: *(i) As per CBEC Circulars issued under the Customs Act, 1962 (ii) Separate Commercial Invoice and Packing List would also be accepted.]

(c) For export or import of

specific goods or category of goods, which are subject to any

restrictions/policy conditions or require NOC or product specific

compliances under any statute, the regulatory authority concerned may

notify additional documents for purposes of export or import.

(d) In specific cases of export or import, the regulatory authority

concerned may electronically or in writing seek additional documents or

information, as deemed necessary to ensure legal compliance.

(e) The above stipulations are effective from 1st April, 2015.

2.07 Principles of Restrictions

12[DGFT may, through a

Notification, impose ‘Prohibition’ or ‘Restriction’: -

a. on export of foodstuffs or other essential products for preventing or

relieving critical shortages;

b. on imports and exports necessary for the application of standards or

regulations for the classification, grading or marketing of commodities

in international trade;

c. on imports of fisheries product, imported in any form, for

enforcement of governmental measures to restrict production of the

domestic product or for certain other purposes;

d. on imports to safeguard country’s external financial position and to

ensure a level of reserves.

e. on imports to promote establishment of a particular industry;

f. for preventing sudden increases in imports from causing serious

injury to domestic producers or to relieve producers who have suffered

such injury;

g. for protection of public morals or to maintain public order;

h. for protection of human, animal or plant life or health

i. relating to the importations or exportations of gold or silver;

j. necessary to secure compliance with laws and regulations including

those relating to the protection of patents, trademarks and copyrights,

and the prevention of deceptive practices

k. relating to the products of prison labour for the protection of

national treasures of artistic, historic or archaeological value

m. for the conservation of exhaustible natural resources

n. for ensuring essential quantities for the domestic processing

industry

o. essential to the acquisition or distribution of products in general

or local short supply;

p. for the protection of country's essential security interests:

i. relating to

fissionable materials or the materials from which they are derived;

ii. relating to the traffic in arms, ammunition and

implements of war;

iii. taken in time of war or other emergency in

international relations; or

q) in pursuance of country's obligations under the United Nations Charter for the maintenance of international peace and security.]

old[DGFT may,

through a Notification, impose restrictions on export and import,

necessary for: -

(a) Protection of public morals;

(b) Protection of human, animal or plant life or health;

(c) Protection of patents, trademarks and copyrights, and the

prevention of deceptive practices;

(d) Prevention of use of prison labour;

(e) Protection of national treasures of artistic, historic or

archaeological value;

(f) Conservation of exhaustible natural resources;

(g) Protection of trade of fissionable material or material from

which they are derived;

(h) Prevention of traffic in arms, ammunition and implements of

war

(i) Relating to the importation or exportation of gold or silver.]

2.08 Export/Import of Restricted Goods/Services

Any goods /service, the export or import of which is 'Restricted' may be exported or imported only in accordance with an Authorisation / Permission or in accordance with the Procedures prescribed in a Notification / Public Notice issued in this regard.2.09 Export of SCOMET Items

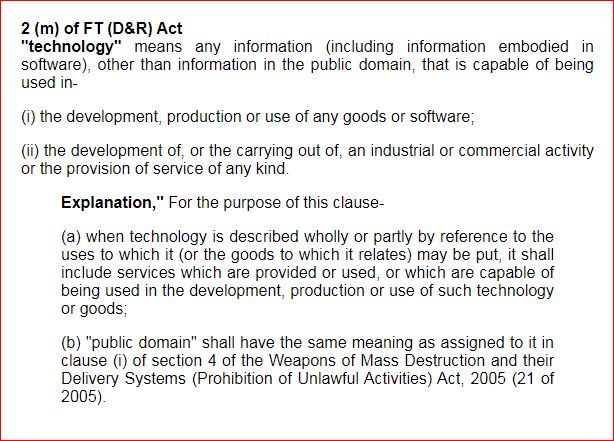

Export of Special Chemicals, Organisms, Materials, Equipment and Technologies (SCOMET), as indicated in Appendix-3 of Schedule 2 of ITC(HS) Classification of Export & Import Items, shall be governed by the specific provisions of (i) Chapter IV A of the FT(D&R) Act, 1992 as amended from time to time (ii) Sl. No. 4 & 5 of Table A and Appendix-3 of Schedule 2 of ITC(HS) Classification of Export & Import Items (iii) Para 2.16, Para 2.17, Para 2.18 of FTP and (iv) Para 2.73 -2.82 of Hand Book of Procedures, in addition to the other provisions of FTP and Handbook of Procedures governing export Authorisations.2.10 Actual User Condition

Goods which are importable freely without any 'Restriction' may be imported by any person. However, if such imports require an Authorisation, actual user alone may import such good(s) unless actual user condition is specifically dispensed with by DGFT.2.11 Terms and Conditions of an Authorisation

Every Authorisation shall, inter alia, include either all or some of the following terms and conditions (as applicable in terms of the para under which the Authorisation has been issued), in addition to such other conditions as may be specified:*2.12 Application Fee

Application for IEC/ Authorisation / License / Scrips must be accompanied by application fees as indicated in the Appendix 2K of Appendices and Aayat Niryat Forms. Fees must be paid online through electronic fund transfer (EFT) mechanism or through Credit/Debit Cards, unless provided otherwise.2.13 Clearance of Goods from Customs against Authorisation

Goods already imported / shipped / arrived, in advance, but not cleared from Customs may also be cleared against an Authorisation issued subsequently. However, such goods already imported/ shipped/ arrived, in advance are first warehoused against Bill of Entry for Warehousing and then cleared for home consumption against an Authorisation issued subsequently. This facility will however be not available to "restricted" items or items traded through STES.2.14 Authorisation - not a Right

No person can claim an Authorisation as a right and DGFT or RA Regional Authority shall have power to refuse to grant or renew the same in accordance with provisions of FT (D&R) Act, Rules made there under and FTP.

2.15 Penal action and placing of an entity in Denied Entity List (DEL)

a) If an Authorisation holder violates any condition of such Authorisation or fails to fulfill export obligation, or fails to deposit the requisite amount within the period specified in demand notice issued by Department of Revenue and /or DGFT, he shall be liable for action in accordance with FT (D&R) Act, the Rules and Orders made there under, FTP and any other law for time being in force.

, scrips,

certificates, instruments etc will be blocked from printing/

issue/renewal.6 [2.15A Cases referred to National Company Law Tribunal (NCLT).

Any firm / company coming under the adjudication proceedings before the National Company Law Tribunal (NCLT) shall inform the concerned Regional Authority (RA) and NCLT of any outstanding export obligations/liabilities under any of the schemes under FTP. The total outstanding duty saved amount / dues along with interest, and any penalty imposed under FTD&R Act, or any other dues, shall be counted as part of the dues to the government against the said firm / company. ]

2.16 Prohibition on Import and Export of 'Arms and related material' from / to Iraq

Notwithstanding the policy on Arms and related materials in Chapter 93 of ITC(HS), the import/export of Arms and related material from/to Iraq is 'Prohibited'. However, export of Arms and related material to Government of Iraq shall be permitted subject to 'No Objection Certificate' from the Department of Defence Production.

2.16 A Prohibition on Trade with the Islamic State in Iraq and the Levant [ISIL, also known as Daesh], Al Nusrah Front [ANF] and other individuals, groups, undertakings and entities associated with Al Qaida.

In compliance with United Nations Security Council Resolution No. 2199 [2015] (full text of the Resolution is available at http://www.un.org/press/en/2015/ sc11775.doc.htm), trade in oil and refined oil products, modular refineries and related materials, besides items of cultural (including antiquities), scientific and religious importance is prohibited with the Islamic State in Iraq and the Levant [ISIL], Al Nusrah Front [ANF] and other individuals, groups, undertakings and entities associated, directly or indirectly, with Al Qaida.

*2.17 Prohibition on direct or indirect import and export from/to DPRK

Direct or Indirect export and import of items, whether or not originating in Democratic People's Republic of Korea (DPRK) to/from DPRK is detailed in Appendix - I of FTP.2.18 Direct or Indirect Export/Import to/from Iran

(a) Direct or indirect export to Iran or import from Iran of any item, material, equipment, goods and technology mentioned in the following documents

would be permitted subject to the provisions contained in Annex-B to the

United Nations Security Council Resolution 2231 (2015):

mentioned in the following documents

would be permitted subject to the provisions contained in Annex-B to the

United Nations Security Council Resolution 2231 (2015):(i) Items listed in INFCIRC International Atomic Energy Agency Information Circular/254/Rev.9/Part 1 and INFCIRC International Atomic Energy Agency Information Circular /254/Rev.7 /Part 2 (IAEA International Atomic Energy Agency Documents) as updated by the IAEA International Atomic Energy Agency from time to time.

(ii) Items listed in S/2006/263 (UN Security Council document) as updated by the Security Council from time to time.

(b) All the UN Security Council Resolutions/Documents and IAEA International Atomic Energy Agency Documents referred to above are available on the UN Security Council website (www.un.org/Docs/sc) and IAEA International Atomic Energy Agency website (www.iaea.org).

2.19 Prohibition on Import of Charcoal from Somalia

Direct or indirect import of charcoal is prohibited from Somalia, irrespective of whether or not such charcoal has originated in Somalia [United Nations Security Council Resolution 2036 (2012)]. Importers of Charcoal shall submit a declaration to Customs that the consignment has not originated in Somalia. Import / Export through State Trading Enterprises:

2.20 State Trading Enterprises (STEs)

(a) State Trading Enterprises (STEs) are governmental and non¬governmental enterprises, including marketing boards, which deal with goods for export and /or import. Any good, import or export of which is governed through exclusive or special privilege granted to State Trading Enterprise (STE), may be imported or exported by the concerned STE State Trading Enterprise as per conditions specified in ITC (HS). The list of STEs notified by DGFT is in Appendix-2J.2.21 Trade with Neighbouring Countries

DGFT may issue instructions or frame schemes as may be required to promote trade and strengthen economic ties with neighboring countries.

2.22 Transit Facility

Transit of goods through India from/ or to countries adjacent to India shall be regulated in accordance with bilateral treaties between India and those countries and will be subject to such restrictions as may be specified by DGFT in accordance with International Conventions.

2.23 Trade with Russia under Debt-Repayment Agreement

In case of trade with Russia under Debt Repayment Agreement, DGFT may issue instructions or frame schemes as may be required, and anything contained in FTP, in so far as it is inconsistent with such instructions or schemes, shall not apply. Import of Specific Categories of Goods:

2.24 Import of Samples

Import of samples shall be governed by Para 2.65 of Handbook of Procedures.

2.25 Import of Gifts

9[Import of goods, including those purchased from e-commerce portals, through post or courier, where Customs clearance is sought as gifts, is prohibited except for life saving drugs / medicines/ oxygen concentrators and Rakhi (but not gifts relatedThe exemption for oxygen concentrators is allowed only for a period till 31 July 2021 for personal use.

Explanation:

1 .Rakhi (but not gifts related to Rakhi) will be covered under Section 25(6) of Customs Act. 1962 that reads " no duty shall be collected if the amount of duty leviable is equal to or less than Rs.100/-"

2. Import of goods as gifts with payment of full applicable duties is allowed]

old[7[Import of goods, including those purchased from

e-commerce portals, through post or courier, where Customs clearance is

sought as gifts, is prohibited except for life saving drugs / medicines

and Rakhi (but not gifts related to Rakhi).

Explanation:

1. Rakhi (but not gifts related to Rakhi) will be covered under Section

25(6) of Customs Act, 1962 that reads ... no duty shall be collected if

the amount of duty leviable is equal to or less than Rs. 100/.”

2. Import of goods as gifts with payment of full applicable duties is

allowed.]]

old[Import of gifts shall be 'free' where such goods are otherwise freely importable under ITC (HS). In other cases, such imports shall be permitted against an Authorisation issued by DGFT.]

2.26 Passenger Baggage

(a)

Bona-fide household goods and personal effects may be imported as part

of passenger baggage as per limits, terms and conditions thereof in

Baggage Rules notified by Ministry of Finance.

(b) Samples of such items that are otherwise freely importable

under FTP may also be imported as part of passenger baggage without an

Authorisation.

(c) Exporters coming from abroad are also allowed to import

drawings, patterns, labels, price tags, buttons, belts, trimming and

embellishments required for export, as part of their passenger baggage

without an Authorisation.

2.27 Re - import of goods repaired abroad

Capital

goods, equipments, components, parts and accessories, whether imported

or indigenous, except those restricted under ITC (HS) may be sent abroad

for repairs, testing, quality improvement or upgradation or

standardization of technology

and re-imported without an Authorisation.

2.28 Import of goods used in projects abroad

Project contractors after completion of projects abroad, may import without an Authorisation, goods including capital goods used in the project, provided they have been used for at least one year.

2.29 Import of Prototypes

Import of new / second hand prototypes / second hand samples may be allowed on payment of duty without an Authorisation to an Actual User (industrial) engaged in production of or having industrial license / letter of intent for research in item for which prototype is sought for product development or research, as the case may be, upon a self- declaration to that effect, to satisfaction of customs authorities

2.30 Import through courier service/Post

Imports through a registered courier service or post are permitted as per Notification(s) issued under the Customs Act, 1962. However, importability of such items shall be regulated in accordance with FTP/ ITC (HS), 2017.

Import Policy for Second Hand Goods:

2.31 Second Hand Goods

| S.No. | Categories of Second Hand Goods | Import Policy | Conditions, if any |

| I | Second Hand Capital Goods | ||

| 5[(a)

(b) |

i. Desktop

Computers , ii. refurbished/ re-conditioned spares of re-furbished parts of Personal Computers/ Laptops iii. Air Conditioners iv. Diesel generating sets

All electronics and IT Goods notified under the Electronics and IT Goods (Requirement of Compulsory Registration) Order, 2012 as amended from time to time. |

Restricted

|

Importable

against Authorisation

|

| old[(a) |

i.

Personal computers/ laptops including their refurbished/ re-

conditioned spares ii. Photocopier machines/ Digita multifunction Print & Copying Machines iii. Air conditioners iv. Diesel generating sets. |

Restricted | Importable against Authorisation] |

| (c) | Refurbished / re-conditioned spares of Capital Goods | Free | Subject to production of Chartered Engineer certificate to the effect that such spares have at least 80% residual life of original spare. |

| (d) | All other second hand capital goods {other than (a) , (b) & (c) above} | Free | |

| II | Second Hand Goods other than capital goods | Restricted |

Importable against Authorisation |

| 1[III |

Second Hand Goods imported for the purpose of repair / refurbishing / re - conditioning or re-engineering. |

Free | Subject to condition that waste generated during the repair / refurbishing of imported items is treated as per domestic Laws/ Rules/ Orders / Regulations/ technical specifications/ Environmental /safety and health norms and the imported item is re - exported back as per the Customs Notification.] |

Import Policy for Metallic Waste and Scraps:

2.32 Import of Metallic waste and Scrap

(a) Import of any form of metallic waste, scrap will be subject to the condition that it will not contain hazardous, toxic waste, radioactive contaminated waste/scrap containing radioactive material, any types of arms, ammunition, mines, shells, live or used cartridge or any other explosive material in any form either used or otherwise as detailed in Para 2.54 of Handbook of Procedures.2.33 Removal of Scrap/waste from SEZ

A SEZ unit/Developer/ Co-developer may be allowed to dispose of in DTA any waste or scrap, including any form of metallic waste and scrap, generated during manufacturing or processing activity, without an Authorisation, on payment of applicable Customs Duty.Other Provisions Related to Imports:

2.34 Import under Lease Financing

No specific permission of RA Regional Authority is required for lease financed capital goods.

2.35 Execution of Legal Undertaking (LUT) / Bank Guarantee (BG)

(a) Wherever any duty free import is allowed or where otherwise specifically stated, importer shall execute, Legal Undertaking (LUT) / Bank Guarantee (BG) / Bond with the Customs Authority, as prescribed, before clearance of goods.(b) In case of indigenous sourcing, Authorisation holder shall furnish LUT/BG Bank Guarantee/Bond to RA Regional Authority concerned before sourcing material from indigenous supplier/nominated agency as prescribed in Chapter 2 of Handbook of Procedures.

2.36 Private/Public Bonded Warehouses for Imports

(a) Private/ Public bonded warehouses may be set up in DTA as per rules, regulations and notifications issued under the Customs Act, 1962. Any person may import goods except prohibited items, arms and ammunition, hazardous waste and chemicals and warehouse them in such bonded warehouses.2.37 Special provision for Hides Skins and semi-finished goods

Hides, Skins and semi-finished leather may be imported in the Public/ Private Bonded warehouse for the purpose of DTA sale and the unsold items thereof can be re-exported from such bonded warehouses on payment of the applicable rate of export duty.

2.38 Sale on High Seas

Sale of goods on high seas for import into India may be made subject to FTP or any other law in force.

Exports:

2.39 Free Exports

All goods may be exported without any restriction except to the extent that such exports are regulated by ITC (HS) or any other provision of FTP or any other law for the time being in force. DGFT may, however, specify through a public notice such terms and conditions according to which any goods, not included in ITC (HS), may be exported without an Authorisation.

2.40 Deleted

-

2.41 Benefits for Supporting Manufacturers

For any benefit to accrue to the supporting manufacturer (as defined in Para 9.58 of FTP), the names of both supporting manufacturer as well as the merchant exporter must figure in the concerned export documents, especially in ARE-1 Application for Removal of Excisable Goods for Export (By Air/Sea/Post/Land) / ARE-3 Application for Removal of Excisable Goods from a factory or a warehouse to another arehouse / Shipping Bill / Bill of Export/ Airway Bill.

2.42 Third Party Exports

Third party exports (except Deemed Export) as defined in Chapter 9 shall be allowed under FTP. In such cases, export documents such as shipping bill shall indicate name of both manufacturing exporter/manufacturer and third party exporter(s). Bank Realization Certificate (BRC), Export Order and Invoice should be in the name of third party exporter.

Exports of Specific Categories:

2.43 Export of Samples

Export of Samples and Free of charge goods shall be governed by provisions given in Para 2.66 of Handbook of Procedures.

2.44 Export of Gifts

Goods including edible items, of value not exceeding Rs.5,00,000/- in a licensing year, may be exported as a gift. However, items mentioned as restricted for exports in ITC (HS) shall not be exported as a gift, without an Authorisation.

2.45 Export of Passenger Baggage

(a) Bona-fide personal baggage may be exported either along with passenger or, if unaccompanied, within one year before or after passenger's departure from India. However, items mentioned as restricted in ITC (HS) shall require an Authorisation. Government of India officials proceeding abroad on official postings shall, however, be permitted to carry along with their personal baggage, food items (free, restricted or prohibited) strictly for their personal consumption. The Provisions of the Para shall be subject to Baggage Rules issued under Customs Act, 1962.(b) Samples of such items that are otherwise freely exportable under FTP may also be exported as part of passenger baggage without an Authorisation.

2.46 Import for export

I. (a) Goods imported, in accordance with FTP, may be exported in same or substantially the same form without an Authorisation provided that item to be imported or exported is not in the restricted for import or export in ITC (HS).(c) Goods in (b) above will include 'Restricted' goods for import (except 'Prohibited' items).

(d) Capital goods, which are freely importable and freely exportable, may be imported for export on execution of LUT/BG Bank Guarantee with Customs Authority.

(e) Notwithstanding the above, goods which are freely

importable may be re-exported except items as in the Prohibited or SCOMET List of exports, in same or substantially same form even though

such goods are under "restricted list" for export, subject to the

following conditions:

(i) Goods are

not of Indian Origin;

(ii) Goods imported

shall be kept in bonded warehouse under supervision of Customs;

(iii) Goods to be

exported have never been cleared for home consumption;

(iv) Export of

goods shall be subjected to Section 69 of Customs Act, 1962.

II. 14[(a) Goods imported against payment in freely convertible currency would be permitted for export only against payment in freely convertible currency, unless otherwise notified by DGFT. Goods imported under Para 2.52(d)(i) would be permitted for exports only against payments as per Para 2.52(d)(ii), unless otherwise notified by DGFT.]

old[(a) Goods imported against payment in freely convertible currency would be permitted for export only against payment in freely convertible currency, unless otherwise notified by DGFT.

(b) Export of such goods to the notified

countries (presently only Iran) would be permitted against payment in

Indian Rupees, subject to minimum 15% value addition.

(c) However, re-export of food, medicine and

medical equipments, namely, items covered under ITC(HS) Chapters 2 to 4,

7 to 11, 15 to 21, 23, 30 and items under headings 9018, 9019, 9020,

9021 & 9022 of Chapter-90 of ITC(HS) will not be subject to minimum

value addition requirement for export to Iran. Exports of these items to

Iran shall, however, be subject to all other conditions of FTP 2015-20

and ITC (HS) 2017, as applicable. Bird's eggs covered under ITC (HS)

0407 & 0408 and Rice covered under ITC (HS) 1006 are not covered under

this dispensation, as at II (a) above.

(d) Exports under this dispensation, as at

I (e) and II (a), (b) and (c) above shall not be eligible for any export

incentives.

2.47 Export through Courier Service/Post

4[2.47 Export through Courier Service/Postold[2[Exports through a registered courier service is permitted as per Notification issued by DoR Department of Revenue. However, exportability of such items shall be regulated in accordance with FTP/ ITC (HS), 2017. The value limit for such exports through courier service and Post shall be Rs 5,00.000 per consignment.]]

old[Exports through a registered courier service is permitted as per Notification issued by DoR Department of Revenue. However, exportability of such items shall be regulated in accordance with FTP/ ITC (HS), 2017.]

2.48 Export of Replacement Goods

Goods or parts thereof on being exported and found defective/damaged or otherwise unfit for use may be replaced free of charge by the exporter and such goods shall be allowed for export by Customs authorities, provided that replacement goods are not mentioned as restricted/SCOMET items for exports in ITC (HS). If the export item is 'restricted'/ under SCOMET, the exporter shall require a export license for replacement.

2.49 Export of Repaired Goods

Goods or

parts thereof, except restricted under ITC (HS), on being exported and

found defective, damaged or otherwise unfit for use may be imported for

repair and subsequent re-export. Such goods shall be allowed clearance

without an Authorisation and in accordance with customs notification. To

that extent the exporter shall return the benefits /incentive availed on

the returned goods. If the item is 'restricted' for import, the exporter

shall require an import license.

However, re-export of such defective parts/spares by the Companies/firms

and Original Equipment Manufacturers shall not be mandatory if they are

imported exclusively for undertaking root cause analysis, testing and

evaluation purpose."

2.50 Export of Spares

Warranty spares (whether indigenous or imported) of plant, equipment, machinery, automobiles or any other goods [except those restricted under ITC (HS)] may be exported along with main equipment or subsequently but within contracted warranty period of such goods, subject to approval of RBI Reserve Bank of India.

2.50A Re-export of imported Goods found defective and unsuitable for use:

Imported goods found defective after Customs clearance, or not found as per specifications or requirements may be re-exported back as per Customs Act, 1962.

2.51 Private Bonded Warehouses for Exports

(a) Private bonded warehouses exclusively for exports may be set up in DTA as per terms and conditions of notifications issued by DoR Department of Revenue.*2.52 Denomination of Export Contracts

(a) All export contracts and invoices shall be denominated either in freely convertible currency or Indian rupees but export proceeds shall be realized in freely convertible currency.(c) Contracts (for which payments are received through Asian Clearing Union (ACU) shall be denominated in ACU Asian Clearing Union Dollar. However, participants in the ACU Asian Clearing Union may settle their transactions in ACU Asian Clearing Union Dollar or in ACU Asian Clearing Union Euro as per RBI Reserve Bank of India Notifications. Central Government may relax provisions of this paragraph in appropriate cases. Export contracts and invoices can be denominated in Indian rupees against EXIM Bank/Government of India line of credit.

13[(d) Invoicing, payment and settlement of exports and imports is also permissible in INR under RBI Reserve Bank of India’s A.P.(DIR Series) Circular No.10 dated 11th July, 2022. Accordingly, settlement of trade transactions in INR may also take place through the Special Rupee Vostro Accounts opened by AD banks in India as permitted under Regulation 7(1) of Foreign Exchange Management (Deposit) Regulations, 2016, in accordance to the following procedures:

(i) Indian importers undertaking imports through this mechanism shall make payment in INR which shall be credited into the Special Vostro account of the correspondent bank of the partner country, against the invoices for the supply of goods or services from the overseas seller /supplier.

(ii) Indian exporters, undertaking exports of goods and services through this mechanism, shall be paid the export proceeds in INR from the balances in the designated Special Vostro account of the correspondent bank of the partner country.]

2.53 14[Applicability of FTP Schemes for Export Realisations in Indian Rupees] old[Export to Iran -Realisations in Indian Rupees to be eligible for FTP benefits / incentives]

14[(i) Export proceeds realized in Indian Rupees against exports to Iran are permitted to avail exports benefits/fulfilment of Export Obligations under the Foreign Trade Policy (2015-20), at par with export proceeds realized in freely convertible currency, subject to compliance of para 2.18 of the FTP.old[Notwithstanding the provisions contained in para 2.52 (a) above, export proceeds realized in Indian Rupees against exports to Iran are permitted to avail exports benefits / incentives under the Foreign Trade Policy (2015¬20), at par with export proceeds realized in freely convertible currency.]

2.54 Non-Realisation of Export Proceeds

(a) If an exporter fails to realize export proceeds within time specified by RBI Reserve Bank of India, he shall, without prejudice to any liability or penalty under any law in force, be liable to return all benefits / incentives availed against such exports and action in accordance with provisions of FT (D&R) Act, Rules and Orders made there under and FTP.2.54A Export Credit Agencies (ECAs)

(i) Export Credit Agencies (ECAS) are policy instrument for Government to support exports. ECAS support exports by insurance, guarantee and also direct lending. Export Credit Agencies (ECAS) like Export Credit Guarantee Corporation of India Ltd. (ECGC) provides credit insurance support to exports and export credit lending. Coversissued by ECGC Export Credit Guarantee Corporation to exporters, protect against losses arising out of payment failures due to insolvency or default of the buyers or due to political risks. Exporters can diversify their markets in addition to protecting existing markets through such covers. ECGC Export Credit Guarantee Corporation also supports Medium and Long term (MLT) exports including project exports. EXIM Bank is the other ECA Enforcement- cum-Adjudication in the business of lending for MLT exports and fronting the governmenf s line of credit.*2.55 Recognition of EPCs to function as Registering Authority for issue of RCMC

(a) Export Promotion Councils (EPCs) are organizations of exporters, set up with the objective to promote and develop Indian exports. Each Council is responsible for promotion of a particular group of products/ projects/services as given in Appendix 2T of AANF.*2.56 Registration-cum-Membership Certificate (RCMC)

Any person, applying for:2.57 Interpretation of Policy

(a) The decision of DGFT shall be final and binding on all matters relating to interpretation of Policy, or provision in Handbook of Procedures, Appendices and Aayat Niryat Forms or classification of any item for import / export in the ITC (HS).*2.58 Exemption from Policy/Procedures

DGFT may in public interest pass such orders or grant such exemption, relaxation or relief, as he may deem fit and proper, on grounds of genuine hardship and adverse impact on trade to any person or class or category of persons from any provision of FTP or any Procedures. While granting such exemption, DGFT may impose such conditions as he may deem fit after consulting the Committees as under:| Sl.No. | Description | Committee |

| (a) | Fixation / modification of product norms | Norms Committees |

| (b) | Nexus with Capital Goods (CG) and benefits under EPCG Schemes | EPCG Committee |

| (c) | All other issues | Policy Relaxation Committee (PRC) |

2.59 Personal Hearing by DGFT for Grievance Redressal

(a) Government is committed to easy and speedy redressal of grievances from Trade and Industry. Paragraph 2.58 of FTP provides for relaxation of Policy and Procedures on grounds of genuine hardship and adverse impact on trade. If an importer/exporter is aggrieved by any decision taken by Policy Relaxation Committee (PRC), or a decision/order by any authority in the Directorate General of Foreign Trade, a specific request for Personal Hearing (PH) along with the prescribed application fee as per Appendix-2K has to be made to DGFT. DGFT may consider request for relaxation after consulting concerned Norms Committee, EPCG Committee or Policy Relaxation Committee (PRC) and the decision conveyed in pursuance to the personal hearing shall be final and binding.2.60 Regularization of EO Export Obligation default and settlement of Customs duty and interest through Settlement Commission

With a view to providing assistance to firms who have defaulted under FTP for reasons beyond their control as also facilitating merger, acquisition and rehabilitation of sick units, it has been decided to empower Settlement Commission in Department of Revenue to decide such cases also with effect from 01.04.2005.

Self Certification of Originating Goods:

2.61 Approved Exporter Scheme for Self Certification of Certificate of Origin.

(i)

Currently, Certificates of Origin under various Preferential Trade

Agreements [PTA], Free Trade Agreements [FTAS], Comprehensive Economic

Cooperation Agreements [CECA] and Comprehensive Economic Partnerships

Agreements [CEPA] are issued by designated agencies as per Appendix 2B

of Appendices and Aayat and Niryat Forms. A new optional system of self

certification is being introduced with a view to reducing transaction

cost.

(ii) The Manufacturers who are also Status Holders shall be eligible for

Approved Exporter Scheme. Approved Exporters will be entitled to self-

certify their manufactured goods as originating from India with a view

to qualifying for preferential treatment under different PTAS/FTAS/

CECAS/CEPAS which are in operation. Self-certification will be permitted

only for the goods that are manufactured as per the Industrial

Entrepreneurs Memorandum (IEM) / Industrial License (IL) /Letter of

Intent (LOI) issued to manufacturers.

(iii) Status Holders will be recognized by DGFT as Approved Exporters

for self-certification based on availability of required infrastructure,

capacity and trained manpower as per the details in Para 2.109 of

Handbook of Procedures 2015-20 read with Appendix 2F of Appendices &

Aayaat Niryat Forms.

(iv) The details of the Scheme, along with the penalty provisions, are

provided in Appendix 2F of Appendices and Aayaat Niryat Forms and will

come into effect only when India incorporates the scheme into a specific

agreement with its partner/s and the same is appropriately

notified by DGFT.

2.62 Certification of Origin of Goods EU-GSP

Exporters can self-certify the Statement on Origin of their goods, as per the self-certification scheme , Certification of Origin of Goods for European Union Generalised System of Preferences (EU-GSP) , of the European Union (EU) under the Registered Exporter System (REX) as in Para 2.104 (c) of the Handbook of Procedures.

1.Inserted Vide:-Notification No. 58/2015-2020 Dated 28.03.2018

2.Substituted Vide:-Notification No. 22/2015-2020 Dated 26.07.2018

3.Substituted Vide:-Notification No. 24/2015-2020 Dated 08.08.2018

4.Substituted Vide:-Notification No. 36/2015-2020 Dated 27.09.2018

5.Substituted Vide:-Notification No. 05/2015-2020 Dated 07.05.2019

6.Inserted Vide:-Notification No. 25/2015-2020 Dated 18.10.2019

7.Substituted Vide:-Notification No. 35/2015-2020 Dated 12.12.2019

8.Inserted Vide:-Notification No. 58/2015-2020 Dated 12.02.2021

9.Substituted Vide:-Notification No. 04/2015-2020 Dated 30.04.2021

10.Substituted Vide:-Notification No. 11/2015-2020 Dated 01.07.2021

11.Substituted Vide:-Notification No. 16/2015-2020 Dated 09.08.2021

12.Substituted Vide:-Notification No. 17/2015-2020 Dated 10.08.2021

13.Inserted Vide:-Notification No. 33/2015-2020 Dated 16.09.2022

14. Substituted Vide:-Notification No. 43/2015-2020 Dated 09.11.2022