HELP MANUAL & FAQs

|

General Instructions - 1. These instructions are to be read with relevant Public Notice and Policy – Provisions.

2. Separate return applications are required to be filed for DTA and for AA/EoU/SEZ Exports.

3. If the total RoDTEP claim for a given IEC exceeds Rs. 1 crore in a financial year, filing the Annual RoDTEP Return (ARR) is mandatory. Conversely, if the total claims for a given IEC remain below Rs. 1 crore for the financial year, you need NOT file the ARR.

3.1. Once you qualify under the rule above, and yet none of the individual 8-digit ITCHS codes crosses Rs. 50 lakh in RoDTEP claims, you may file the ARR only for the 8 digit code under which you claimed the highest amount.

3.1.1. For example, if your total RoDTEP claim in a year amounts to Rs. 1.2 crore— where the distribution is

3.2. However, after qualifying under the 1 cr rule, if any individual 8-digit ITC-HS code exceeds Rs. 50 lakh in RoDTEP, an ARR must be filed for each of those codes.

3.2.1. For instance, if your total RoDTEP claim is Rs. 1.2 crore, where the distribution is

4. The Tax/Duties/Levies need to be provided in the fields on pro-rata basis for export products on which the retrun is being filed.

5. Wherever approximation is used for calculation of taxes/duties/levies etc. the same should be justified and substantiated at the time of scrutiny in case the return is picked up for scrutiny on the Risk Management System.

6. The return should be complete to the extent possible. Minor items with low value may be omitted if they don’t significantly alter the amount of remission claimed. 7.The details of the taxes/levies should be limited to such taxes/levies which are not currently being rebated/refunded through any other mechanism such as GST refunds or exemptions by state/central government.

Field related Instructions - |

1.

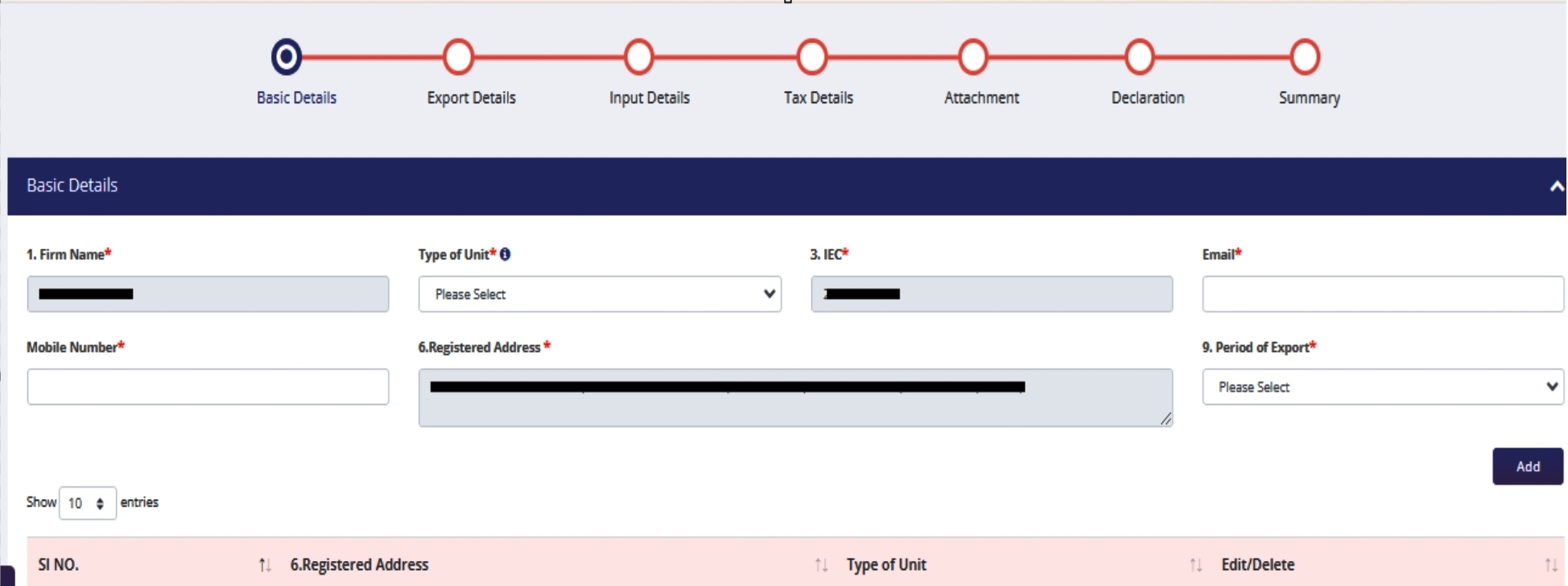

Basic Details

|

Sl No. |

Item Field |

Description |

|

1 |

Name of the Manufacturer/ Manufacturer Exporter |

Name of the IEC Holder availing RoDTEP |

|

2 |

Type of Unit (DTA/AA/SEZ/EoU) |

1. This refers to the type of unit your business operates for the RoDTEP benefits claimed under. This field is for purposes of mapping of exports and its related duties/levies with the eligible rate of support under RoDTEP for DTA Exports (Appendix 4R) and for SEZ/AA/EoU (Appendix 4RE). 2. Separate returns are required to be filed for DTA and AA/EoU/SEZ Exports. |

|

3 |

IEC/PAN |

Registered 12 digit PAN/IEC |

|

6 |

Complete Address of the Manufacturing unit with mobile/ office phone and working office email (add more rows if data pertains to more than 1 unit -2A, 2B,etc.) |

The appropriate registered address should be selected. |

|

9 |

Period of Export |

The relevant period of export from 01.04.2023 to 31.03.2024. |

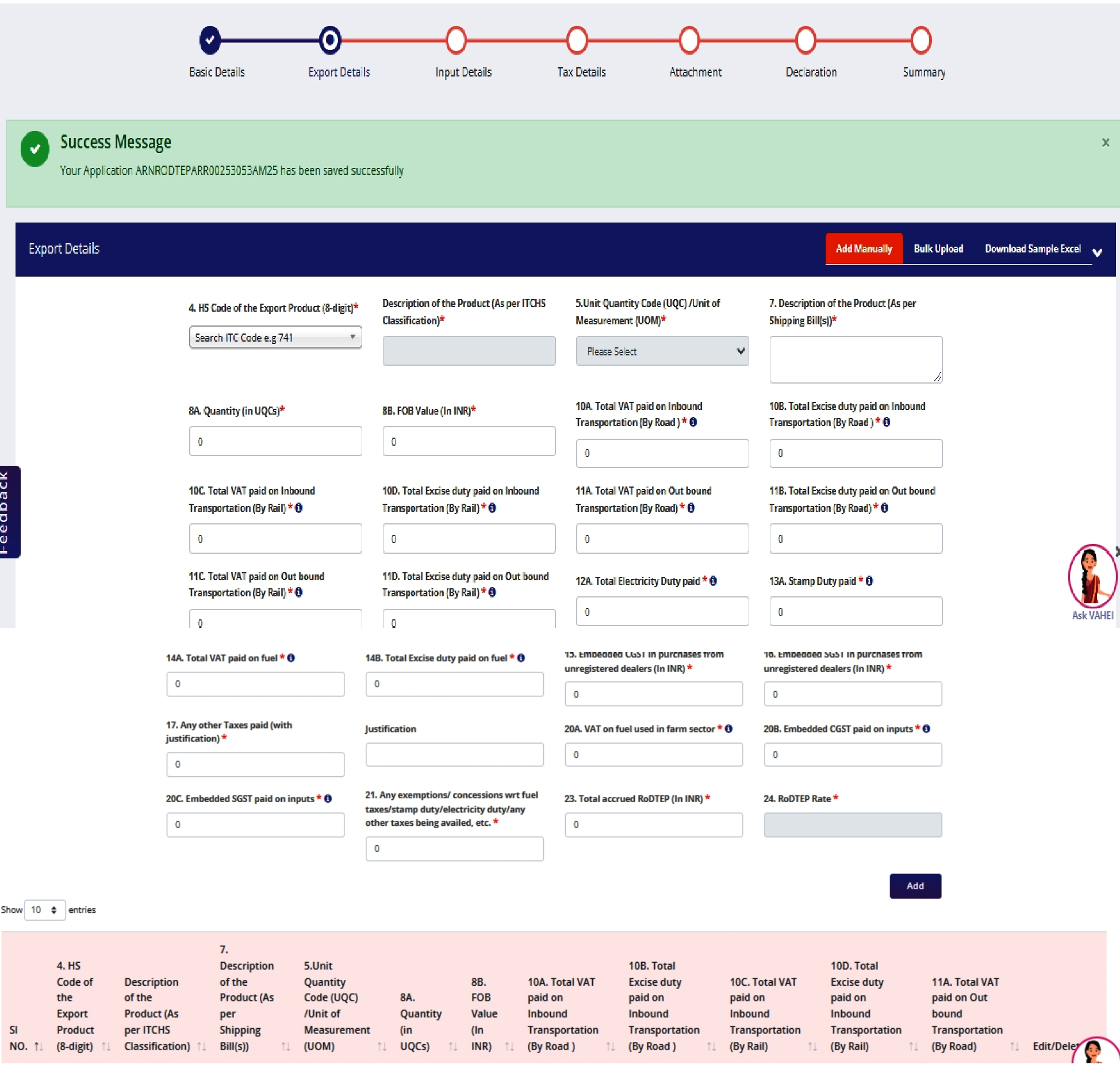

2. Export Details

|

Sl No. |

Item Field |

Description |

|

4 |

HS Code of the Export Product at 8 digit |

Separate returns are needed to be filed for the individual 8-digit HS Codes. However, it is required to file return for only such items wherein the RoDTEP benefit claimed value is equal to or more than Rs. 50 Lakhs in a year. Otherwise if under none of the 8-digit HS Code, the support accrued has crossed the threshold of Rs. 50 Lakhs a year, then a single return for the 8-digit HS Code with highest accrued support should be filed. |

|

5 |

Unit Quantity Code (UQC) of Exported Product /Unit of Measurement |

The response should be standardised to one of the Unit Quantity Code (UQC) torepresent the unit of measurement for a particular product. |

|

7 |

Exact Description of the Product as per Shipping Bill(s) |

This refers to the specific details of the product as it's listed on the Shipping Bill |

|

8 |

Export Clearance of Goods |

|

|

8A |

Quantity of product exported during 01.04.2023 to 31.03.2024 (in UQCs) |

Quantity of product exported during 01.04.2023 to 31.03.2024 (in UQCs) |

|

8B |

FOB value of product exported during 01.04.2023 to 01.03.2024 |

This refers to the total value of your exported product during the financial year 2023-2024, calculated on a Free On Board (FOB) basis in Indian Rupees as per the applicable Customs Exchange Rates. |

|

10 |

Cost of Inbound Transport: |

|

|

10A |

Total VAT paid on transportation cost actually incurred with respect to process of procuring raw materials, consumables, spares for manufacture of exported product (Inbound Transportation) (By Road ) |

Note: VAT is a type of tax levied by the State/UT Government on the Transportation Fuels such as Diesel. |

|

10B |

Total Excise duty paid on transportation cost actually incurred with respect to process of procuring raw materials, consumables, spares for manufacture of exported product (Inbound Transportation) (By Road ) |

This refers to the total amount of tax you paid specifically on the cost of transporting raw materials, consumables, and spare parts that you used to manufacture your exported product. This tax is only for the transportation costs, not the items themselves. It's the tax you paid on the cost of moving these items by road.

Note: Excise duty is a type of tax/duty levied by the Union Government on the Transportation Fuels such as Diesel. |

|

10C |

Total VAT paid on transportation cost actually incurred with respect to process of procuring raw materials, consumables, spares for manufacture of exported product (Inbound Transportation) (By Rail) |

Similar to 10 A. |

|

10D |

Total Excise duty paid on transportation cost actually incurred with respect to process of procuring raw materials, consumables, spares for manufacture of exported product (Inbound Transportation) (By Rail) |

Similar to 10B |

|

11 |

Cost of Outbound Transport: |

|

|

11A |

Total VAT paid on transportation cost actually incurred with respect to process of transporting exported product from factory to the gateway port (Out bound Transportation) (By road) |

This means the total tax (VAT) you paid on the cost of transporting your finished product from your factory to the gateway port from where it will be shipped internationally. This tax is specifically for the transportation costs, not the product itself. It's the tax you paid on the cost of moving your product by road.

Note: VAT is a type of tax levied by the State/UT Government on the Transportation Fuels such as Diesel. |

|

11B |

Total Excise duty paid on transportation cost actually incurred with respect to process of transporting exported product from factory to the gateway port (Out bound Transportation) (By road) |

Note: Excise duty is a type of tax/duty levied by the Union Government on the Transportation Fuels such as Diesel. |

|

11C |

Total VAT paid on transportation cost actually incurred with respect to process of transporting exported product from factory to the gateway port (Out bound Transportation) (By rail) |

Similar to 11 A. |

|

11D |

Total Excise duty paid on transportation cost actually incurred with respect to process of transporting exported product from factory to the gateway port (Out bound Transportation) (By rail) |

Similar to 11 B. |

|

12 |

Electricity Duty: |

|

|

12 |

Total Electricity Duty paid |

This means the total tax (electricity duty), |

|

A |

for manufacture of exported product in the period 01.04.2023 to 31.03.2024 |

apportionable to exported product, paid on the electricity consumed for the financial year 20232024. |

|

13 |

Stamp Duty: |

|

|

13A |

Stamp Duty paid for relevant Export Documents (in Rs) |

This means the total amount of tax (stamp duty) you paid on the official documents required for exporting your product. These documents might include contracts, invoices, bills of lading, and other customs paperwork. |

|

14 |

Fuel used in generation of captive power: |

|

|

14A |

Total VAT paid on fuel for manufacture of exported product in the period 01.04.2023 to 31.03.2024 |

The total amount of VAT paid on the fuel used for captive power generation, apportionable to exported product, for the financial year 2023-2024. |

|

14B |

Total Excise duty paid on fuel for manufacture of exported product in the period 01.04.2023 to 31.03.2024 |

The total amount of Excise duty paid on the fuel used for captive power generation, apportionable to exported product, for the financial year2023-2024. |

|

15 |

Embedded CGST in purchases from unregistered dealers |

Embedded CGST, apportionable to exported product, for the purchases made from the unregistered dealers, for which no refund is due. |

|

16 |

Embedded SGST in purchases from unregistered dealers |

This means the State Goods and Services Tax (SGST) that is included in the price of goods or services purchased from a supplier who is not registered under the GST system. In this case, you, as the registered business, are responsible for paying the SGST to the government, even though the supplier did not collect it. This is known as the Reverse Charge Mechanism (RCM) under GST.

Embedded CGST, apportionable to exported product, for the purchases made from the unregistered dealers, for which no refund is due. |

|

17 |

Any other Taxes paid (with justification) |

Proper calculation for such is to be attached. |

|

20 |

Taxes/ Duties per unit of Raw Material (only for farm sector) |

|

|

20A |

VAT on fuel used in farm sector (for farm products and for product made from farm products only) |

This means the tax (VAT) you pay on the fuel used for agricultural purposes. This fuel could be used for various activities like running tractors, irrigation pumps, or transporting farm products |

|

20B |

Embedded CGST paid on inputs such as pesticides, fertilizers etc. used in production of agricultural goods(For farm products only) |

This means the Central Goods and Services Tax (CGST) that is included in the price of inputs like pesticides and fertilizers for agricultural activities. |

|

20C |

Embedded SGST paid on inputs such as pesticides, fertilizers etc. used in production of agricultural goods(For farm products only) |

This means the State Goods and Services Tax (CGST) that is included in the price of inputs like pesticides and fertilizers for agricultural activities. |

|

21 |

Kindly indicate any exemptions/concessions w.r.t. fuel taxes/stamp duty/electricity duty/any other taxes being availed, etc. |

It is to be given with proper justification. |

|

23 |

Total accrued RoDTEP during the period 01.04.2023 to 31.03.2024. |

Value of the total amount of benefit that you are eligible for under the RoDEP Scheme in the given period. |

|

24 |

RoDTEP Rate given for the exported product |

The rate at which the exported product is eligible for RoDTEP benefit as mentioned in Appendix 4R or/and Appendix 4RE. |

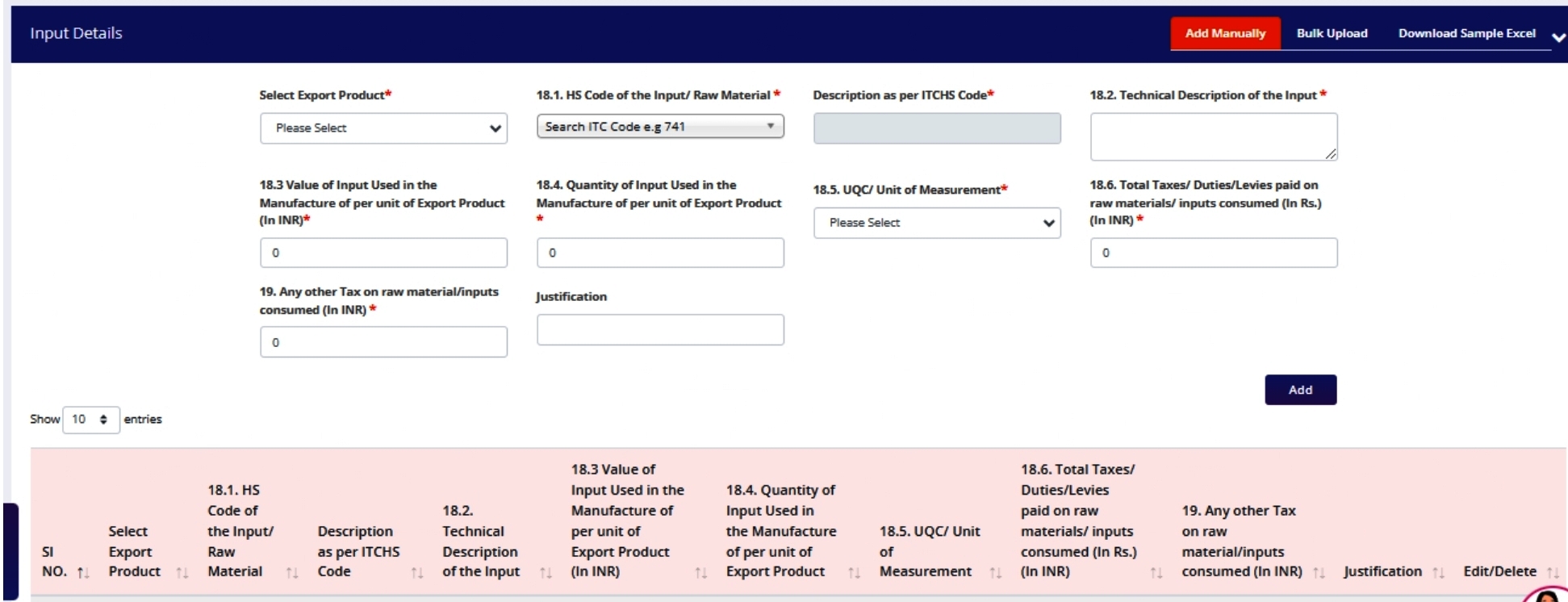

3. Input Details

|

Sl No. |

Item Field |

Description |

|

18 |

Incidence of Taxes/ Duties/ Levies Borne by the Export Product on account of prior stage cumulative taxes on raw materials/ inputs consumed in the manufacturing of export product. |

This section requires you to determine the proportion of taxes that were levied on the raw materials used in the production of the exported product, and which ultimately contribute to the final cost of that exported product. |

|

|

Inputs |

Inputs are to be listed which have been used in the manufacture of the exported product under proper ITC HS codes at 8-digit level. |

|

18.A |

HS Code of the Input/ Raw Material |

The HS Code at 8- digit level of the inputs used in manufacture of the exported product is to be written. |

|

18.B |

Description of the Input |

|

|

18.C |

Value of the Input used in the Manufacture of per unit of Export Product (Rs.) |

This part asks you to determine the total cost (in Rupees) of each material used to make one unit of your exported product. |

|

18.D |

Quantity of Input used in the manufacture of per unit of Export Product |

This part asks you to determine the amount/quantity of each material used to make one unit of your exported product. |

|

18.E |

UQC/ Unit of Measurement |

The response should be standardised to one of the Unit Quantity Code (UQC) to represent the unit of measurement for a particular product |

|

18.F |

Total Taxes/ Duties/ Levies paid on raw materials/ inputs consumed. |

This section requires you to determine the total amount of taxes that were levied on the raw materials used in the production of the exported product. |

|

19 |

Any other Tax on raw material/ inputs consumed (with justification) |

Proper calculation for such is to be attached. |

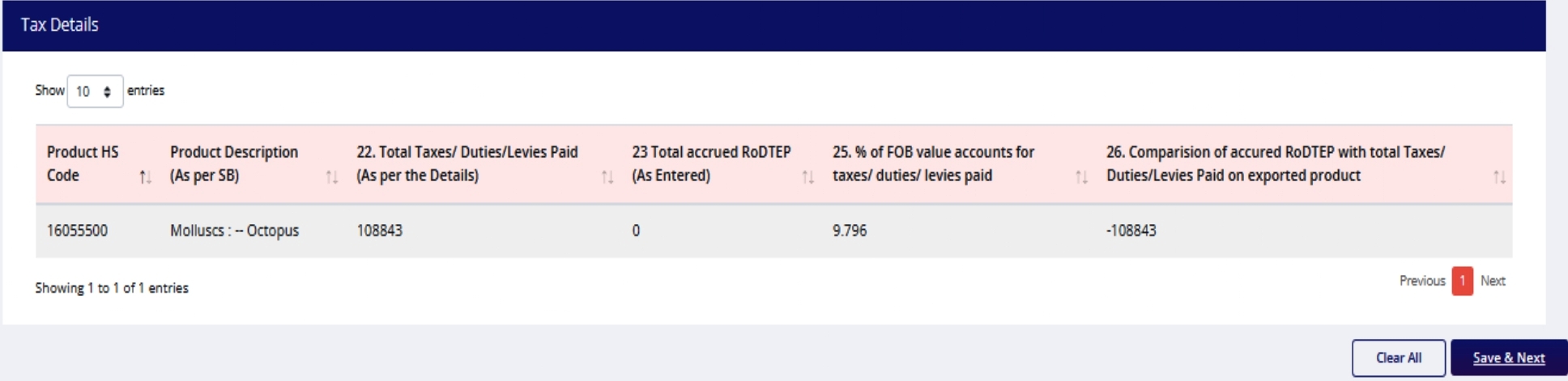

4. Tax Details

|

Sl No. |

Item Field |

Description |

|

22, 23,25, 26 |

Total Taxes/ Duties/Levies Paid on exported product during the period 01.04.2023 to 31.03.2024 |

It will be calculated and displayed by the system itself, based on the figures provided before. |

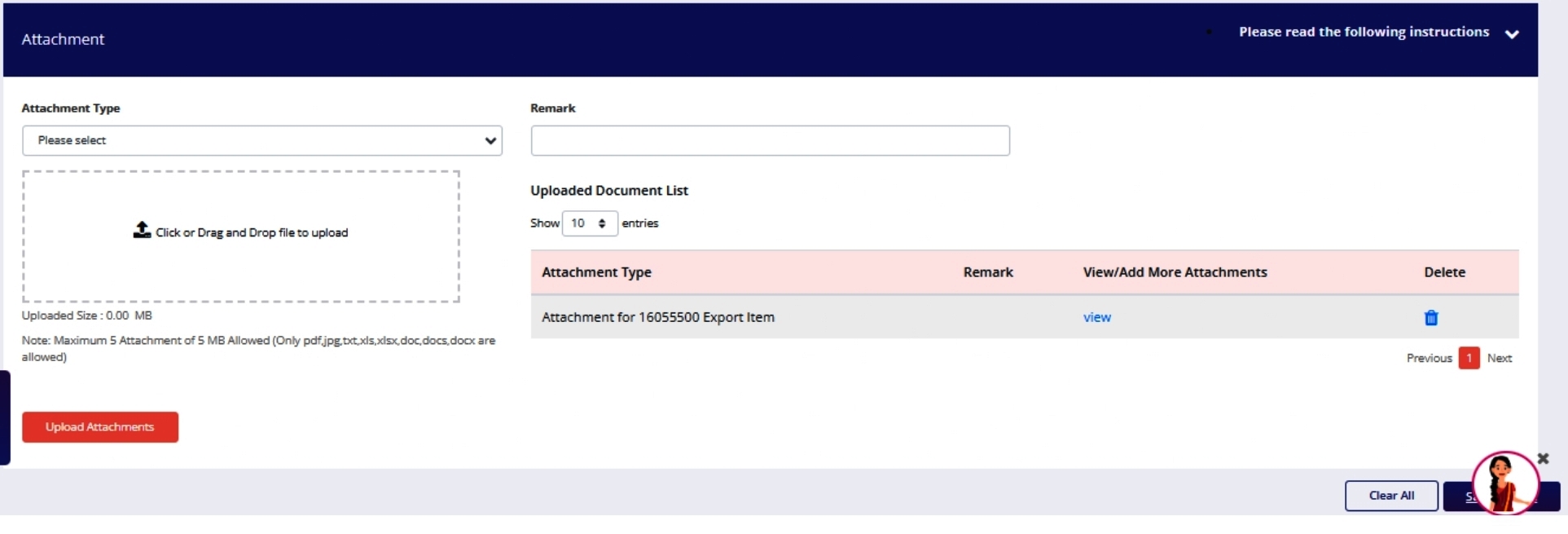

5. Attachment

|

Item Field |

Description |

|

Attachments |

Relevant attachments in the form of PDF, Excel, etc. related to relevant calculations/ information are to be uploaded. |

6. Declaration

|

Item Field |

Description |

|

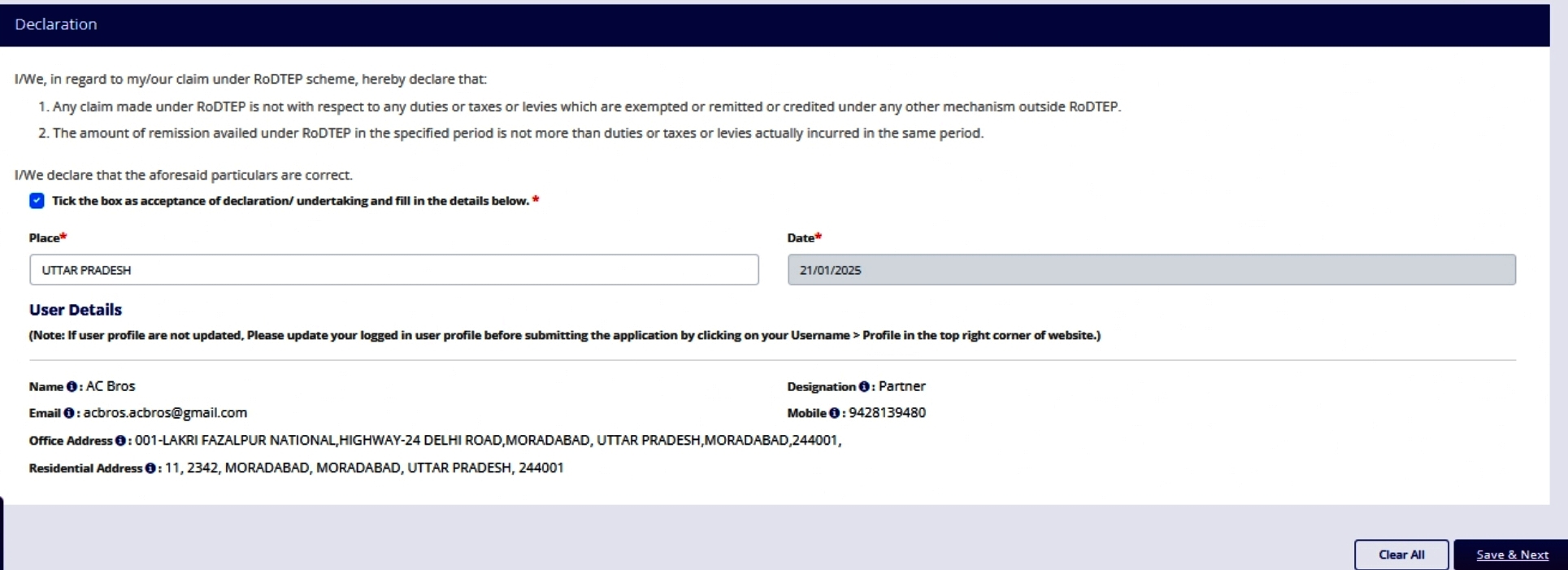

Declaration |

Check for the details being displayed and move forward with the declaration. |

27. Is it required for merchant exporters to also file ARR? In such a case, how should a merchant exporter get the details from the manufacturer?

Ans: Yes, merchant exporters who have availed over Rs 1 Cr. Of RoDTEP in the given financial year are expected to file ARR by tying up with the manufacturer supplier of the goods for providing the information. The rules of Para 3 of the general instructions given in this manual shall also apply for merchant exporters.

28. How shall we arrive at the tax amount claimed on the fuel used for transportation. For example, I have an invoice of transport charges from the transporter without any fuel consumption and associated taxation details.

Ans: The firm should follow the same reporting method that is used before the RoDTEP committee for fixation of RoDTEP rate. Alternatively, the firm may establish an approximation of arriving at fuel charges and associated taxation based on a survey with their transporters and the same may be used as a basis for calculation of transportation related refunds one full financial year. The details of such approximation should be kept ready for verification for the stipulated period.

29. If the actual claim amount received under the RoDTEP Scheme is less than the total RoDTEP claim value of Rs. 1 Cr or more, are the exporters required to file the Annual RoDTEP Return?

Ans: The exporters are required to file the annual RoDTEP Return if the the total RoDTEP claim value in more the Rs. 1 Cr or more. For example- If the total RoDTEP claim value is Rs. 1,00,00,000, however, the actual claim received is Rs. 95,00,000, the exporter is required to file the Annual RoDTEP Return.