any duty has been

paid, such duty shall be refunded to the person by whom or on whose behalf it

was paid, if -

any duty has been

paid, such duty shall be refunded to the person by whom or on whose behalf it

was paid, if - | Previous |

Customs Act 1962

Levy of, and Exemption from, Customs Duties

Section 26: Refund of export duty in certain cases

Where on the exportation of any

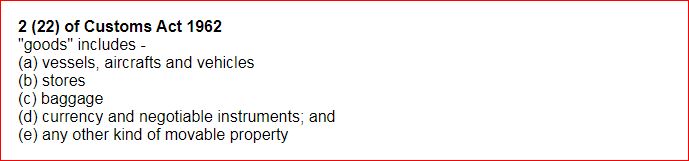

goods

any duty has been

paid, such duty shall be refunded to the person by whom or on whose behalf it

was paid, if -

(a) the goods are returned to such person otherwise than by way of re-sale;

(b) the goods are re-imported within one year from the date of exportation; and

(c) an

application for refund of such duty is made before the expiry of six months from

the date on which the

proper officer

makes an order for the clearance of the

goods.

makes an order for the clearance of the

goods.

| Previous |