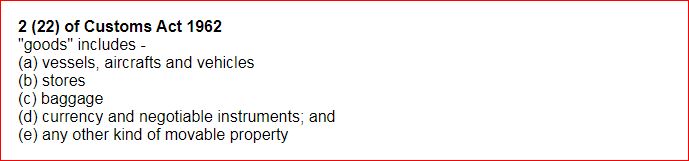

Customs Act 1962

Confiscation of goods and

conveyances and imposition of penalties

Section 116. Penalty for not

accounting for goods.

If any

goods

loaded in a

conveyance

loaded in a

conveyance

for importation

into

India

for importation

into

India

, or any goods transhipped under the provisions of this Act or

coastal goods

, or any goods transhipped under the provisions of this Act or

coastal goods

carried in a conveyance, are not unloaded at their place of destination in

India, or if the quantity unloaded is short of the quantity to be unloaded at

that destination, and if the failure to unload or the deficiency is not

accounted for to the satisfaction of the Assistant Commissioner of Customs or

Deputy Commissioner of Customs, the

person-in-charge

carried in a conveyance, are not unloaded at their place of destination in

India, or if the quantity unloaded is short of the quantity to be unloaded at

that destination, and if the failure to unload or the deficiency is not

accounted for to the satisfaction of the Assistant Commissioner of Customs or

Deputy Commissioner of Customs, the

person-in-charge

of the conveyance shall be

liable, -

of the conveyance shall be

liable, -

(a) in the case of goods loaded

in a conveyance for importation into India or goods transhipped under the

provisions of this Act, to a penalty not exceeding twice the amount of duty that

would have been chargeable on the goods not unloaded or the deficient goods, as

the case may be, had such goods been imported;

(b) in the case of coastal

goods, to a penalty not exceeding twice the amount of export duty that would

have been chargeable on the goods not unloaded or the deficient goods, as the

case may be, had such goods been exported.