Feegrade And Co Private Limited

Versus

Commissioner Of Customs

Customs Appeal No. 20970 of 2015 decided on 17-10-2025

CUSTOMS, EXCISE AND SERVICE TAX

APPELLATE TRIBUNAL

HYDERABAD

REGIONAL BENCH - COURT NO. – I

Customs Appeal No. 20970 of 2015

(Arising out of Order-in-Appeal No. 117 & 118/2014 - VCH dated 16.09.2014 passed by Commissioner of Customs, Central Excise and Service Tax (Appeals), Visakhapatnam)

M/s Feegrade And Co Pvt Ltd.,

.. APPELLANT

Rungta House, Chaibasa Po,

Jharkhand – 833 201.

VERSUS

Commissioner Of Customs

.. RESPONDENT

Visakhapatnam - Customs

4th Floor, Customs House,

Port Area, Visakhapatnam,

Andhra Pradesh – 530 035.

WITH

Customs Appeal No. 20601 of 2015

(Arising out of Order-in-Appeal No. 180/2014 - 15 - VCH dated 19.01.2015 passed by Commissioner of Customs, Central Excise and Service Tax (Appeals), Visakhapatnam)

M/s Feegrade And Co Pvt Ltd.,

.. APPELLANT

Rungta House, Chaibasa Po,

Jharkhand – 833 201.

VERSUS

Commissioner Of Customs

.. RESPONDENT

Visakhapatnam - Customs

4th Floor, Customs House,

Port Area, Visakhapatnam,

Andhra Pradesh – 530 035.

WITH

Customs Appeal No. 20602 of 2015

(Arising out of Order-in-Appeal No. 181/2014 – 15- VCH dated 19.01.2015 passed by Commissioner of Customs, Central Excise and Service Tax (Appeals), Visakhapatnam)

M/s Feegrade And Co Pvt Ltd.,

.. APPELLANT

Rungta House, Chaibasa Po,

Jharkhand – 833 201.

VERSUS

Commissioner Of Customs

.. RESPONDENT

Visakhapatnam - Customs

4th Floor, Customs House,

Port Area, Visakhapatnam,

Andhra Pradesh – 530 035.

AND

Customs Appeal No. 20603 of 2015

(Arising out of Order-in-Appeal No. 182/2014 – 15 - VCH dated 19.01.2015 passed by Commissioner of Customs, Central Excise and Service Tax (Appeals), Visakhapatnam)

M/s Feegrade And Co Pvt Ltd.,

.. APPELLANT

Rungta House, Chaibasa Po,

Jharkhand – 833 201.

VERSUS

Commissioner Of Customs

.. RESPONDENT

Visakhapatnam - Customs

4th Floor, Customs House,

Port Area, Visakhapatnam,

Andhra Pradesh – 530 035.

APPEARANCE:

Shri S.C. Choudhury, Advocate for the Appellants.

Shri K. Sreenivasa Reddy, Authorised Representative for the Respondent.

CORAM: HON’BLE Mr. A.K.

JYOTISHI, MEMBER (TECHNICAL)

HON’BLE Mr. ANGAD PRASAD, MEMBER (JUDICIAL)

FINAL ORDER No. A/30427-30430/2025

Date of Hearing:03.07.2025

Date of Decision:17.10.2025

[ORDER PER: A.K. JYOTISHI]

M/s Feegrade And Co Private

Limited (hereinafter referred to as Appellant) are in appeal against the

Order-In-Appeal No. 117 & 118/2014 dated 16.09.2014, 180-182/2014-15 dated

19.01.2015 (impugned order).

2. The issue, in brief, is that the appellant had entered into contract with

foreign buyers for supply of Iron Ore of certain specifications, where the final

price was payable depending on the actual quantity received, quality, actual Fe

percentage determined as per CIQ report at the discharge Port, in terms of

mutually agreed terms and conditions. The final payment was based on final

commercial invoice to be issued by the appellant in terms of finally determined

quality, quantity etc., in accordance with the contract. The Department, at the

time of export, kept the assessment provisional based on provisional invoice

furnished by the appellant as also for the purpose of testing certain para-meters

like moisture content and Fe percentage. For the purpose of provisional

assessment, necessary bond and security as directed by the Department was also

executed by the appellant. Subsequently, based on the test report of CIQ at the

discharge port and on receipt of final payment based on final commercial invoice

issue by the appellant to the foreign buyers, the appellant approached the

Department for finalization of their provisional assessment.

3. The Department, in general, calculated the net quantity of export taking into

account the moisture content, as determined by their lab i.e. CRCL, based on

sample taken at the time of export and thereafter proceeded to examine the final

invoice and proof of receipt of payment in the form of Bank Realisation

Certificate (BRC). While re-determining the value, they did not dispute the rate

per Metric Tonne of ore, as declared, at the time of export but re-computed the

total export quantity itself keeping in view the moisture content determined by

the CRCL, which was lower than the declared moisture content at the time of

export or even lower to moisture content shown in the CIQ report at discharge

Port. Since, the appellant had paid duty provisionally and also deposited

certain additional amount as directed by the Department based on provisional

invoice at the time of provisional assessment, they approached for refund of

excess payment in terms of the statutory provisions. Based on their assessment,

Department re-worked out the total duty payable and amount already paid to

compute the amount of refund admissible. It is the grievance of the appellant

that the said refund amount has been wrongly computed in as much as while

recomputing the same, they had not taken note of the fact that there was no

occasion for the department to doubt the transaction value in the first place or

BRC and therefore BRC value or realised value for the consignment should have

been taken as the basis for deciding the final duty payable and it was not open

to them to re-compute the entire duty liability in the manner in which they have

re-computed the refund amount by re-determining the quantity of export leading

to grant of lesser refund than what they are otherwise eligible for.

4. Learned Counsel for the appellant has mainly submitted that it is not

disputed that the entire consignment has been exported in terms of contract

between the appellant and the importer abroad. It is also not disputed that they

have realised only the sum as reflected in their final invoices as well as BRC

from their buyer, who is not a related person. It is also not disputed that the

transaction value declared by them in terms of per Metric Tonne of ore at the

time of export has been found correct or not acceptable to the Department.

Therefore, when there was no reason to doubt the transaction value, the

Department could not have again re-computed the value for the purpose of

computing customs duty payable by resorting to Rule 4 and 5 of Export Valuation

Rules. It was already pointed out that no grounds were adduced or any

opportunity given before re-computation clarifying as to what was the ground on

which the transaction value was not found admissible. He further submits that

the variation in quantity due to moisture content is of no consequence post

10.10.2007, as old Section 14 covering the valuation of goods for import and

export has been rescinded with a new concept of transaction value, wherein,

there is a specific provision as to under what circumstances, a transaction

value can be rejected and the value for the purpose of payment of customs duty

could be re-computed and in what manner. One of the major criteria is to explain

the reasons as to the ground for doubting the declared transaction value, as

also the rationale and basis for adopting a particular method under Rule 4 or 5

for re-computing the value. Further, when duty is payable on advalorem basis,

redetermination of quantity is not required and the final value received towards

the consignment from buyer has to be taken as the transaction value. He has also

relied on many case laws, including in their own case, decided by this Bench. He

is relying on the case of VGM Exports vide Final Order No. A/30317-30324/2024

dated 06.05.2024. He is further submitting that during the export, they had

deposited 20% of duty, as additional revenue deposited, to cover any excess duty

payment that may become payable on account of finalisation of assessment and

since it was a provisional assessment, such deposits were not in the nature of

duty and only a revenue deposit and in view of the same, they are also entitled

to get interest. He has relied on certain case laws viz - Indore Treasure Market

City Pvt. Ltd., VS Commissioner of CGST and Central Excise, Indore vide Final

Order No. 50125 of 2024 dated 11.01.2024 [2024 (24) Centax 469 (TriBang)] and

Parle Agro Pvt Ltd., Vs Commissioner, CGST, Noida [2022 (380) ELT 219 (Tri-All)]

as also the Co-ordinate Bench decision in appeal no. C/75029/2020 vide Final

Order No. 76970/2024 dated 09.09.2024.

5. Learned AR on the other hand has mainly submitted that the Adjudicating

Authority has rightly accepted the CRCL report for the purpose of determining

moisture content in the exported goods and accordingly recomputed the value of

the consignment.

6. Heard both the sides and perused the records.

7. Since in all these appeals, the issues are more or less similar and impugned

Order-in-Originals and Order-in-Appeals have also analysed and decided the

matter more or less on similar lines and also the terms of contract being more

or less similar, we proceed to decide all these appeals by way of common order.

8. However, before we proceed, some of the admitted factual positions in these

appeals, which has not been disputed, need to be highlighted. The transaction

value per Metric Tonne, as declared at the time of export, has not been doubted

by Department. It is a case of provisional assessment where provisional duty and

certain additional amount was paid at the time of export on provisional basis.

There is some dispute as regards the coverage and liability on account of

execution of bond, wherein the Department feels that it was incumbent upon

appellant to accept the CRCL moisture report in terms of said bond, whereas, the

appellant’s submission is that the bond was only binding on them to pay the

differential duty, if any, after finalisation of provisional assessment, and

that the CRCL test report in respect of moisture content was relevant only to

the extent to determine the Fe content, as more than 64% Fe content would have

covered the consignment under the restricted category, as iron ore above 64% Fe

content was a canalised item. Therefore, there is no binding on them in terms of

said bond to accept moisture content as determined by CRCL for the purpose of

re-determining the quantity of goods exported.

9. We have perused the relevant contracts covering the exports under different

Shipping Bills, where same standard terms and conditions regarding quality,

price adjustment for Fe content, bonus / penalty for impurities, payment

methods, method of sampling and analyse etc., have been agreed upon. It also,

interalia, provides that the weight as determined by the CIQ shall be final and

clause 9(a), para 3 of contract further provides that CIQ analysis (for moisture

and composition) shall be final. Therefore, what is to be understood that while

the price declared at the time export was provisional and was dependent on the

mutually agreed terms and conditions between the exporter / appellant and the

importer in foreign country after it’s analysis at the time of unloading at

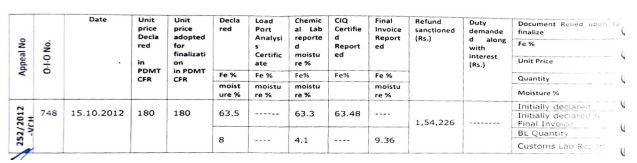

discharge Port by designated agency (CIQ). We find that Commissioner (Appeals)

has gone through each of the parameters declared by the appellant provisionally

and the ones adopted by the Adjudicating Authority for computing the total duty

payable at the time of finalisation of Shipping Bills. The same is reproduced

below for ease of reference:

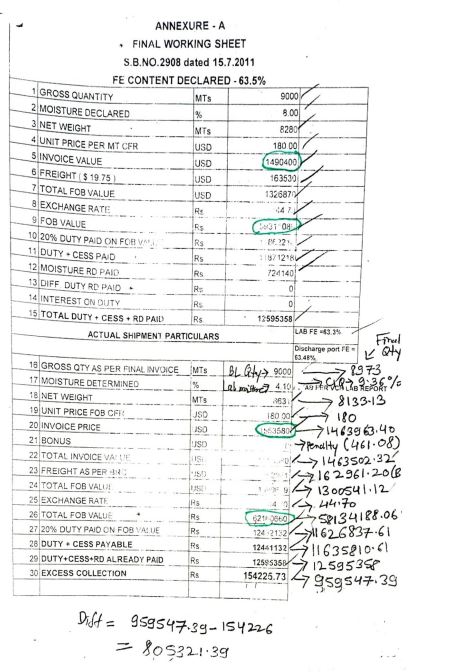

Further, in order to understand the method of computing the duty payable by the

Department, we have also gone through the calculation sheet adopted by the

Refund Sanctioning Authority for deciding the refund amount on conclusion of

finalisation of Bill of Entry. We have taken up Order-in-Original No. 748/2012

dated 15.10.2012, which is the subject matter of Order-in-Appeal No. 181/2014

and covered in appeal no. C/20602/2015 as a reference case. The computation is

indicated below for ease of reference:like image

From the perusal of the above, it is obvious that there is not much dispute

regarding the Fe content of iron ore fines, as declared or as found in terms of

CRCL report or for that matter in terms of final invoice, as thus treated as

within the tolerance. The Department has also not contested the slight variation

in percentage of Fe content as determined by CIQ. They have also not disputed

unit price per Metric Tonne as declared at the time of export in the final

invoice, being same. The Adjudicating Authority has, however, taken for the

purpose of computation, the moisture content as determined by the CRCL and has

ignored the moisture content as per CIQ report. There is no dispute in so far as

unit price, however, the dispute is on account of the net weight i.e 8631 MT

arrived at by the Adjudicating Authority as per moisture content declared by the

CRCL i.e 4.10% whereas, the net quantity in terms of contract has been decided

as 8133.13 MT taking into account the CIQ’s determination of moisture 9.36%.

Therefore, it is apparent that based on this method of computation, the

Department arrived at a higher FOB value, as compared to lower FOB value which

was taken by the appellant for the purpose of raising final commercial invoice

as per terms and conditions of contract and as a consequence, the excess payment

computed was determined by the Adjudicating Authority as only Rs. 1,54,226/-

whereas, as per the appellant it should have been Rs. 9,59,547.39 and therefore

they have been deprived of refund of Rs. 8,05,321.39/-.

10. We find that essentially it is a case where the contract for supply of iron

ore has certain parameters as regards Fe content, moisture content etc., and has

also prescribed certain tolerance for the same. It has also prescribed for

certain bonus and penalty in the event of those parameters being met or not met.

It has also provided for payment, both provisional and final, and basis for

arriving at the final price. Therefore, it is obvious that once there is a

contract, which is dependent on determination of the net quantity and certain

quality parameters in a manner understood to both exporter and importer, the

final invoice has to be raised in accordance with the agreed upon terms and

conditions and accordingly a final invoice has been raised in this case also and

the payments have been received to that extent only as evidenced by the BRC,

which is a document which indicates the realisation in terms of particular

export consignment under the cover of a particular shipping bill(s). This

document, per se, has not been doubted. We also note that in any case, the

re-computation of the quantity has got no meaning when the duty itself is on

advalorem basis and therefore what is important is to see whether there was any

ground for doubting the declared transaction value in the first place or

otherwise. In this case, no grounds were existing at the time of declaration, as

obviously neither Department nor the appellant were sure about what would be the

final price in terms of the negotiated, mutually agreed contract covering the

said consignment. It was at the time of finalisation of provisional assessment,

when the final invoice and the BRC were submitted to the Department, they could

have raised any objection as regards non-acceptance of the said transaction

value or BRC and thereafter they could have proceeded as provided under the

Export Valuation Rules following certain prescribed procedure and thereafter

could have adopted the value of either identical goods or similar goods. We find

that no such activities have been undertaken, and finalisation is based & relied

on re-computation of quantity based on the moisture content as determined by the

CRCL. We find much force in the submissions of the appellant that in terms of

contract, the quantity has to be determined in terms of the moisture content

adopted by the importer in terms of CIQ. Moreover, we also find that when the

export duty is leviable on ad valorem basis, the re-computation of the quantity

based on the moisture content has no meaning, as has been held in their own case

in the Appeal No. 25373/2013 by this Bench. We have perused the judgment passed

by the Hyderabad Bench in the bunch of appeals, vide Final Order No.

A/3031730324/2024 dated 21.06.2024, wherein, interalia, all these issues were

deliberated upon and it was, interalia, held that irrespective of the quantity

of ore exported, as the export duty is on ad valorem basis, the value for export

duty has to be taken as per transaction value only. It was held that in all such

cases, transaction value has been followed by the appellant including present

appellant. The relevant paras are cited below:

11. Therefore, in all these cases, the contracts are clearly specifying these parameters. From the documentary evidence provided by way of invoices, it is seen that based on the moisture content arrived at by CIQ, the appellant has reduced the quantity and arrived at the DMT quantity. There is no dispute that the appellant has realised only the value shown in the total value shown in the invoices. Therefore, it is clear that the transaction value has been followed by the appellant. This also meets the requirement as specified in the Circular No. 12/2014 dated 17.11.2014. Hence on this count the Appeal stands allowed.

12. Another point to be considered is that in this case the Export duty is on advalorem basis, which is dependent on the value of the consignment exported. Irrespective of the quantity of DMT exported, the fact remains that the appellant has received the export proceeds only for the net quantity shown in their Invoices. Hence, the value for Export Duty has to be taken as per Transaction Value only. Admittedly, as per the Para 11 of the Order-in-Original, the transaction value is not doubted. Hence, even on considering this fact, the impugned order cannot be sustained.

11. We, therefore, find that the

issue of modifying or re-determining the quantity in final invoice based on

moisture content as per CIQ report, has been followed consistently, especially

when the amount received is in accordance with the said quantity in terms of the

contract. We also note that great deal of emphasis has been placed on Bond

executed by the appellant at the time of provisional assessment. We find that

the bond is primarily for binding exporter to pay the differential duty, if any,

on final assessment of duty and not for accepting moisture content of CRCL.

Therefore, bond and any additional security provided by exporter is essentially

for binding him to ultimately pay the amount finally determined but it cannot be

construed that it binds exporter irrevocably to accept even the parameters like

moisture content as determined by CRCL having bearing on quality and quantity

etc., which is contrary to mutually agreed contract unless specifically covered

in the said bond in explicit manner. If that is the case, everything could have

been determined at the time of export itself based on parameters determined by

CRCL itself and therefore there would not have been any reason to resort to

provisional assessment. We feel that at most, the bond could have covered Fe

Content determination and if found above 64% it would have made the said export

restricted and liable to certain final action. That is not the case here. We

have also perused the judgment relied upon by Learned AR, M/s Aban Loyd Chiles

Offshore Ltd., Vs Union of India [2008 (227) ELT 24 (SC)] and Reliance Cellulose

Products Ltd., [1997 (93) ELT 646 (SC)]. The context and facts analysed and

observations made are not relevant to facts of the case as in the present

appeal, there is a contract which regulates the final price, hence full effect

has to be given to that contract. Therefore, the facts are distinguished. We

find that in the present appeals facts are more or less similar to earlier

decided matter in their own case and therefore following the ratio laid down in

their own case, we find that the order of the Commissioner (Appeals) upholding

the order of the Adjudicating Authority is not legally tenable and therefore

liable to be set aside.

12. The appellants have also requested that since they had deposited 20% of the

duty based on the declared value, as additional revenue deposit, to cover any

excess duty at the time of provisional assessment and therefore, said deposits

are in the nature of revenue deposits and therefore in the event of not getting

adjusted against the final payment of duty, the same is required to be refunded

along with interest, relying on certain judgements cited, supra. We find that

Section 18 of the Customs Act regulates the entire gamut of provisional

assessment of duty, including requirement to pay the additional duty, in case

finally assessed duty is higher than the amount deposited or return the amount

by way of refund, in case it held to be more than duty finally assessed.

Essentially, the provision is that when an assessment is done provisionally in

terms of Section 18, the exporter is required to furnish certain security, as

the proper Officer may deem fit, for the payment of deficiency, if any, between

the duty as may be finally assessed or re-assessed as the case may be and the

duty provisionally assessed. Thereafter, when the duty leviable on such goods is

assessed finally, then the amount paid towards the deficiency between the duty

provisionally assessed and finally assessed is required to be adjusted against

the duty finally assessed first and thereafter, if some amount of duty is still

required to be recovered then the exporter is required to pay by adjusting the

amount already paid, whereas, if the amount paid is in excess of duty finally

assessed, then the said amount will be refunded. Further, Section 18(4)

provides, subject to sub-section 5, that if any refundable amount referred to in

clause (a) of sub-section 2 of Section 18 is not refunded under that sub-section

within three months from the date of final assessment of duty finally, they

shall be paid interest on such un-refunded amount at such rate fixed by the

Central Government under Section 27(1) till the date of refund of such amount.

Therefore, the harmonious reading of the provisions under Section 18 would

indicate that it is a comprehensive provision to regulate as to how provisional

assessments are to be regulated. Therefore, whatever amount is paid as an

additional deposit or security at the time of provisional assessment are in the

nature of security or revenue deposit, which is required to be adjusted or

appreciated towards duty in case any deficiency is noted between the duty paid

at the time of provisional assessment and duty finally assessed. Therefore, it

is not in the nature of duty, per se. Further, this amount has not been referred

to as duty in Section 18 of the Customs Act itself and it has been referred to

as an “amount” and the refund is also required to be made in respect of the said

amount and that to within three months from the date of finalisation of the

provisional assessment. Therefore, in a situation, where, on finalisation of

provisional assessment excess payment do not get fully adjusted towards duty

payable and there being excess would be entitled to be refunded in terms of

Section 18(4) and would also be entitled for interest, as prescribed in this

regard, beyond three months from the date of finalisation of provisional

assessment. Thus, interest is also regulated by the Section 18(4) and there is

no need to provide any other method for determination of interest amount. We

also find force in the judgments cited by Learned Advocate in support of

entitlement of interest in respect of such excess payment.

13. Therefore, having regard to the various citations, as well as statutory

provision, we find that the amount of customs duty finally payable has to be

computed by the Refund Sanctioning Authority, based on the value/price received

by the appellant in terms of final commercial price and BRC and thereafter,

excess payments of any amount, if any, made by them has to be computed and

refunded along with applicable interest in accordance with the provisions under

Section 18(4) of Customs Act 1962. Further, this being an old matter, the

exercise to re-compute and grant of refund and interest thereon in accordance

with law has to be concluded within a period of two months by the Department

subject to appellant providing the relevant documents. The matter is remanded

back only for the re-quantification of refund and applicable interest in view of

observations made in earlier paragraphs.

14. Appeals are allowed by way remand with consequential reliefs, as per law.

(Pronounced in open court on 17.10.2025)

(A.K. JYOTISHI)

MEMBER (TECHNICAL)

(ANGAD PRASAD)

MEMBER (JUDICIAL)