Anil Art And Craft

Versus

State Of Uttar Pradesh

WRIT TAX No. - 5924 of 2025 decided on 20-11-2025

HIGH COURT OF JUDICATURE AT ALLAHABAD

WRIT TAX No. - 5924 of 2025

M/S Anil Art And Craft

.....Petitioner(s)

Versus

State Of Uttar Pradesh And

Another

.....Respondent(s)

Counsel for Petitioner(s)

: Pranjal Shukla

Counsel for Respondent(s) :

C.S.C.

Along with:-

Writ Tax No.5931 of 2025

M/s Poonam Creation Vs. State of U.P. and another

Court No. - 3

HON'BLE SAUMITRA DAYAL SINGH, J.

HON'BLE INDRAJEET SHUKLA, J.

1. Heard Sri Pranjal Shukla, learned counsel for the petitioner and Sri Arvind Mishra, learned counsel for the revenue and peruse the record.

2. Present petition has been filed to assail the order dated 15.10.2025 passed by Assistant Commissioner, State Tax, Bhadohi Sector-1, Uttar Pradesh cancelling the petitioner's registration.

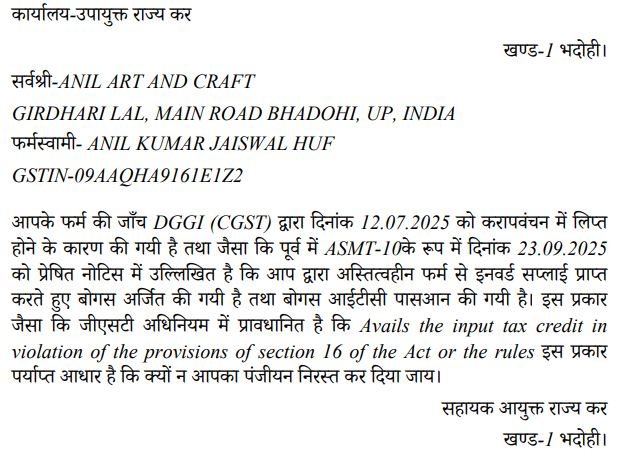

3. Earlier the petitioner was issued show cause notice by said authority dated 08.10.2025. For ready reference that notice is extracted below:-

FORM GST REG -17

[(See Rule 22(1)]

Reference No.:1ZA0910250544250 Date: 08/10/2025

To

Registration Number (GSTIN/UIN) 09AAQHA9161E1Z2

Anul Kumar Jaiswal HUF

O. Girdhari Lal, Main Road Bhadohi, Bhadohi, UP, India, Bhadohi, Bhadohi, Uttar Pradesh-221401Show Cause Notice for Cancellation of Registration

Whereas on the basis of information which has come to my notice, it appears that your registration is ilable to be cancelled for the following reasons:

1. Others

Remarks:

Avails the input tax credit in violation of the provisions of section 16 of the Act or the rules.

You are hereby directed to furnish a reply to the notice within seven working days from the date of service of this notice.

You are hereby directed to appear before the undersigned authority on 15/10/2025 at 12:27.

If you fail to furnish a reply within the stipulated date or fail to appear for personal hearing on the appointed dated and time, the case will be decided ex parte on the basis of available records and on merits.

Kindly refer the supportive document attached for case specific details.

Place: Uttar Pradesh

Date: 08/10/2025Jyoti Singh

Assistant Commissioner

Bhadohi Sector-1

4. The petitioner submitted a detailed reply dated 15.10.2025. Briefly, it may be noted that the petitioner explained that the survey was conducted by the DGGI (an authority under the CGST Act, 2017). It was further pointed out that the said proceeding was pending. The petitioner was cooperating in the same. Therefore, he prayed the proceeding be dropped pending the action by DGGI.

5. By means of the impugned order, after taking note of the reply submitted by the petitioner, respondent no.2 has observed that reply is 'not satisfactory'. It is surprising that by such an unreasoned order, the petitioner's registration has been cancelled. For ready reference that order is extracted below:-

FORM GST REG-19

[See rule 22 (3))]

Reference Number:-ZA0910251251414 Date: 15/10/2025

To

Name: ANIL KUMAR HUF

Address: O. Girdhari Lal, Main Road Bhadohi, Bhadohi, UP, India, Bhadohi, Bhadohi, Uttar Pradesh-221401

(GSTIN/UIN) 09AAQHA9161E1Z2

Application Reference Number (ARN) AA091025033710N Date: 15/10/2025Order for Cancellation of Registration

This has reference to show cause notice issued dated 08/10/2025.

Whereas reply to the show cause notice has been submitted vide AA091025033710N dated 15/10/2025; and whereas, the undersigned on examination of your reply to show cause notice and based on record available with this office is of the opinion that your registration is liable to be cancelled for following reason (s):

1. Others

Remarks:

REPLY IS NOT SATISFACTORY

The effective date of cancellation of your registration is 08/10/2025.

2. Kindly refer to the supportive document(s) attached for case specific details:- Not Applicable3. It may be noted that a registered person furnishing return under sub-section (1) of section 39 of the CGST Act, 2017 is required to furnish a final return in FORM GSTR-10 within three months of the date of this order.

4. You are required to furnish all your pending returns.

5. It may be noted that the cancellation of registration shall not affect the liability to pay tax and other dues under this Act or to discharge any obligation under this Act or the rules made thereunder for any period prior to the date of cancellation whether or not such tax and other dues are deterimined before or after the date of cancellation.

Place: Uttar Pradesh

Date: 15/10/2025Jyoti Singh

Assistant Commissioner

Bhadohi Sector-1

6. It is a self apparent truth that respondent no.2 has acted carelessly in complete defiance of the minimum requirement of procedural law, inasmuch as, absolutely no reason has been assigned to reject the explanation furnished by the petitioner. By stating that the reply is "not satisfactory", the said respondent-authority has only indicated the conclusion but has made no disclosure of the reason, to reach that conclusion.

7. It is a sine qua non and absolutely fundamental to procedural law as may be plain to a law student that such a requirement is non-negotiable. Therefore, we are at loss to understand what would have compelled respondent no.2 to pass such a non-speaking order.

8. We are equally mindful that the order of cancellation of registration causes deep adverse impact on the conduct of business of any registered individual. Neither the petitioner shall remain entitled to issue Tax Invoices nor may be entitled to avail tax ITC or to pass on ITC. Under the GST regime, it announces the economic death of the business entity.

9. On query made, learned standing counsel states that respondent no.2 may be permitted to withdraw the order and pass appropriate reasoned order.

10. While the court appreciates

the fairness on part of learned standing counsel, we cannot leave the matter at

that. Accordingly, the impugned order is set-aside. With respect to the

proceeding that may be continued or conducted pursuant to the show cause notice

dated 08.10.2025 we provide as below:-

(i) Let this order be communicated to the Commissioner, Commercial Tax, Uttar

Pradesh within one week along with a copy this petition, by the learned standing

counsel.

(ii) The Commissioner, Commercial Tax, Uttar Pradesh may first issue appropriate order to transfer the cancellation proceeding to an officer well informed in law, who may conduct and conclude the proceeding strictly in accordance with law.

(iii) The Commissioner, Commercial Tax, Uttar Pradesh may take notice of this occurrence and issue appropriate administrative instructions to all the officers/authorities under the GST to ensure that such action is not repeated in future by other proper officers/authority (dealing with matters on cancellation of registration ), except at risk of appropriate administrative action.

(iv) The above instructions (to be issued by the Commissioner) would necessarily provide for penal consequences that may be followed if such orders are passed by authorities, in future.

11. It is expected that the necessary instructions/circular would be issued by the Commissioner within a period of 15 days from the date of communication of this order.

12. We note, this is not a stray case that has come before us. Since last more than one month, often we have been confronted with similar situation where orders cancelling registration have been passed without assigning any reason or without affording due opportunity to file reply and hearing.

13. It may also be noted, in such cases minimum time be given to the noticee to furnish reply and the orders may be passed after affording due opportunity of hearing in the time bound manner without granting any undue advantage.

14. The writ petition is allowed.

(Indrajeet Shukla,J.) (Saumitra Dayal Singh,J.)

November 20, 2025