Gameloft Software Private Limited

Versus

Assistant Commissioner Of Central Tax

W.P.(C) 16315/2025 decided on 28-10-2025

IN THE HIGH COURT OF DELHI AT NEW DELHI

Date of decision: 28th October, 2025

W.P.(C) 16315/2025 & CM APPL. 66751/2025

GAMELOFT SOFTWARE PRIVATE LIMITED

.....Petitioner

Through: Mr.

Kishore Kunal & Mr. Aditya

Rathore, Advs.

versus

ASSISTANT COMMISSIONER OF CENTRAL

TAX,

RANGE 152 & ANR.

.....Respondents

Through: Mr.

Akash Verma, SSC, CBIC.

CORAM:

JUSTICE PRATHIBA M. SINGH

JUSTICE SHAIL JAIN

PRATHIBA M. SINGH,

J. (ORAL)

1. This hearing has been done through hybrid mode.

CM APPL. 66751/2025 (for exemption)

2. Allowed, subject to all just exceptions. Application is disposed of.

W.P.(C) 16315/2025

3. The present petition has been filed by the Petitioner under Articles 226 and

227 of the Constitution of India, inter alia, seeking expeditious disposal of

the refund applications filed by the Petitioner.

4. The case of the Petitioner is that the Petitioner had paid an excess amount

of Integrated Goods and Services Tax (hereinafter, ‘IGST’) during the

period from April, 2019 to June, 2020 of a sum of Rs. 1,87,84,018/-. The refund

applications themselves were filed in April, 2022 but were rejected vide orders

dated 6th July, 2022 and 7th July, 2022 citing certain deficiencies. Revised

refund applications were filed on 30th March, 2023 and 31st March, 2023 and no

deficiency memo was issued in terms of the timelines fixed within the 15 days.

5. However, thereafter, a deficiency memo was issued on 11th April, 2023 merely

stating that the “supporting documents were incomplete”. Thereafter,

representations have been written by the Petitioner but to no avail and the

refund applications continued to remain pending.

6. Heard. As per the statutorily prescribed procedure, the refund applications

have to be dealt with in a particular manner within the prescribed timelines as

per law. The scheme of the Act and Rules has been analysed by this Court in

W.P. (C) 7485/2024 titled ‘MS G S Industries v. Commissioner of

Central Tax and GST Delhi West’. The relevant portion of the said

decision reads as under:

“10. The Court has considered the matter. The provisions that are relevant in determining the interest on delayed refunds are covered by Section 54 and 56 of the Central Goods and Services Tax Act, 2017 (hereinafter ‘CGST Act’). For ease of reference, the same is extracted below:

Section 54 of the CGST Act

“54. Refund of tax.— (1) Any person claiming refund of any tax and interest, if any, paid on such tax or any other amount paid by him, may make an application before the expiry of two years from the relevant date in such form and manner as may be prescribed: Provided that a registered person, claiming refund of any balance in the electronic cash ledger in accordance with the provisions of sub-section (6) of section 49, may claim such refund in the return furnished under section 39 in such manner as may be prescribed.

******

(5) If, on receipt of any such application, the proper officer is satisfied that the whole or part of the amount claimed as refund is refundable, he may make an order accordingly and the amount so determined shall be credited to the Fund referred to in section 57.

******(7) The proper officer shall issue the order under subsection (5) within sixty days from the date of receipt of application complete in all respects.”

Section 56 of the CGST Act

“56. Interest on delayed refunds.—If any tax ordered to be refunded under sub-section (5) of section 54 to any applicant is not refunded within sixty days from the date of receipt of application under sub-section (1) of that section, interest at such rate not exceeding six per cent. as may be specified in the notification issued by the Government on the recommendations of the Council shall be payable in respect of such refund from the date immediately after the expiry of sixty days from the date of receipt of application under the said sub-section till the date of refund of such tax:

Provided that where any claim of refund arises from an order passed by an adjudicating authority or Appellate Authority or Appellate Tribunal or court which has attained finality and the same is not refunded within sixty days from the date of receipt of application filed consequent to such order, interest at such rate not exceeding nine per cent. as may be notified by the Government on the recommendations of the Council shall be payable in respect of such refund from the date immediately after the expiry of sixty days from the date of receipt of application till the date of refund.

Explanation. ––For the purposes of this section, where any order of refund is made by an Appellate Authority, Appellate Tribunal or any court against an order of the proper officer under sub-section (5) of section 54, the order passed by the Appellate Authority, Appellate Tribunal or by the court shall be deemed to be an order passed under the said sub-section (5).”11. The entire scheme for grant of refunds under CGST Act has been considered by this Court in Bansal International v. Commissioner of DGST (W.P.(C) 11629/2023, decided on 21st November, 2023) and the relevant portion of the judgement is extracted below:

“31. It is important to note that the rate of interest as specified in the main provision of Section 56 of the CGST Act and the proviso to Section 56 of the CGST Act is materially different. Whereas, the main provision of Section 56 of the CGST Act provides for an interest at the rate not exceeding 6% per annum, the proviso to Section 56 of the CGST Act stipulates interest at the rate not exceeding 9% per annum.

32. The learned counsel also informed this Court that the interest at the rate of 6% per annum and 9% per annum has been notified for the purposes of Section 56 of the CGST Act and the proviso to the said section, respectively. Thus, there are two separate rates of interest specified under Section 56 of the CGST Act. The interest at the rate of 6% is payable for the period commencing from a date immediately after expiry of sixty days from the date of an application under Section 54(1) of the CGST Act, however, this rate is enhanced for the period covered under the proviso to Section 56 of the CGST Act. The proviso to Section 56 of the CGST Act expressly provides that an interest at the rate of 9% per annum would be payable from the date immediately after the expiry of sixty days from the receipt of an application, which is filed as a consequent to an order passed by the Appellate Authority, Adjudicating Authority, Appellate Tribunal or a court that has attained finality. This clearly indicates that if a person’s claim for refund is a subject matter of further proceedings, which finally culminate in orders upholding the applicant’s entitlement, and yet the payment is not made within a period of sixty days from an application filed pursuant to such orders, the person is required to be compensated at a higher rate of interest, of 9% per annum. This higher rate of interest would run from the date immediately after the expiry of sixty days of the filing of such an application – that is, the application filed pursuant to the orders of the appellate fora and not the first application.33. It is clear from a plain reading of Section 56 of the CGST Act that whereas the main provision of Section 56 of the CGST Act refers to the rate of interest applicable on the amount of refund due, which remains unpaid even after sixty days from the date of application for refund; the proviso provides for an increased rate of interest for the period that commences from the date immediately after the expiry of sixty days from the date of application which is filed pursuant to the claim for refund attaining finality in appellate proceedings. Section 56 of the CGST Act, thus, works as follows. The applicant claiming a refund is entitled to interest at the rate of 6% per annum from a date immediately after the expiry of sixty days from making an application under Section 54(1) of the CGST Act. However, if a person’s claim is denied (or if granted is not accepted by the Revenue) and the order of the Adjudicating Authority is carried in appeal to the Appellate Authority or to the Appellate Tribunal/High Court, which finally upholds the claim, the applicant may have to file a second application to secure the refund. If such application for refund filed by the person consequent to succeeding before the Appellate Authority, Appellate Tribunal or court, is not processed within a period of sixty days of filing the application, the applicant would be entitled to a higher rate of 9% per annum commencing from the date immediately after the expiry of sixty days of his application filed pursuant to the appellate orders. However, this does not mean that the rate of 6% per annum is not payable for the period commencing from the date immediately after expiry of sixty days from his first application till sixty days after filing of his second application pursuant to the appellate orders. In another words, the proviso merely enhances the interest payable to a person for the period commencing from the date immediately after sixty days from the date of his application filed pursuant to its entitlement to refund claim attaining finality.”

12. The stand of ld. Counsel for the Petitioner is that the deficiency memo was not issued within 15 days in terms of Rule 90 of Central Goods Services Tax Rules (hereinafter ‘CGST Rules’). Hence, the interest is liable to be granted for the entire period.13. The stand of the Department is that the deficiencies were genuine and they were cleared only after two months i.e., when the documents were submitted and the same was duly acknowledged on 11th February, 2020.

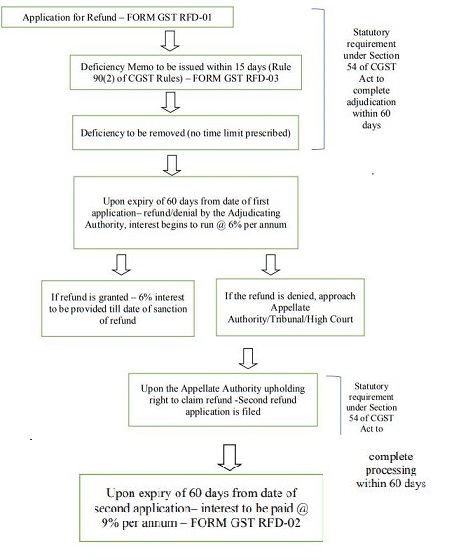

14. The scheme of payment of interest on delayed refunds can be illustrated in the following flow chart. Note -1: For the period from FORM GST RFD-01 till the second refund application, 6% interest would be liable to be paid.

Note-2: If the second refund application is filed, then upon expiry of 60 days, interest would be liable to be paid @ 9% per annum.Payment of Interest in an Application for Refund under Section 56 of CGST Act read with Rule 90 of CGST Rules

15. Considering the overall

circumstances, this Court is of the view that the Petitioner cannot be denied

the benefit of interest for delay caused due to the deficiency memo not having

been issued within the stipulated period, i.e., between 4th/9th July, 2019 and

29th November, 2019. At the same time, the Petitioner also took about 74 days to

respond to the deficiency memo i.e., between 29th November, 2019 and 11th

February, 2020.”

7. In addition, if there is delay by the Department in processing and granting

refunds, it has a cascading adverse effect on the business of the tax payers as

well. Under these circumstances, this Court is of the opinion that the

Respondent ought to take a decision expeditiously on the refund applications.

8. Accordingly, the Petitioner shall appear before the Department on 10th

November, 2025 either physically or virtually as may be communicated to the

Petitioner. If there are any deficiencies which have already been pointed out,

the same shall be cleared by the Petitioner and the refund orders shall be

passed within a period of one month in accordance with law. All rights and

remedies are left open.

9. Petition is disposed of in these terms. All pending applications, if any, are

also disposed of.

PRATHIBA M. SINGH

JUDGE

SHAIL JAIN

JUDGE

OCTOBER 28, 2025