Nova Homa Care

Versus

Addl. Commissioner

WRIT TAX No. - 1035 of 2025 decided on 09-10-2025

HIGH COURT OF JUDICATURE AT

ALLAHABAD

LUCKNOW

WRIT TAX No. - 1035 of 2025

M/S Nova Homa Care Thru.

Proprietor Shri

Sanjeev Jaiswal

.....Petitioner(s)

Versus

Addl. Commissioner Grade-2 Appeal

Iv State Tax

Lko. And Another

.....Respondent(s)

Counsel for Petitioner(s)

: Vikas Singh, Raja Babu Gupta

Counsel for Respondent(s) : C.S.C.

Court No. - 6

HON'BLE JASPREET SINGH, J.

1. Heard learned counsel for the

petitioner and learned Standing Counsel for the State.

2. Present petition has been filed challenging the order dated 11.12.2023 passed

under Section 73 of the U.P. Goods and Services Tax Act, 2017 (for short, 'the

GST Act') as well as the order dated 09.09.2025 whereby the appeal was dismissed

as being beyond limitation.

3. Contention of learned counsel for the petitioner is that no opportunity of

hearing was granted while passing the order under Section 73 of the GST Act. It

has also pointed out that in absence of any opportunity the order impugned

cannot be sustained and this issue was dealt by the Division Bench of this Court

passed in Writ Tax No.303 of 2024 [Mahaveer Trading Company vs. Deputy

Commissioner, State Tax and Anr; 2024:AHC:38820-DB].

4. Learned Standing Counsel, on the basis of the instructions, states that in so

far as the issue of opportunity of hearing is concerned, no date was fixed for

personal hearing.

5. Before adverting to the aforesaid submissions it will be appropriate to

notice the observations made by the Division Bench of this Court in Mahaveer

Trading Company (supra) wherein in paras-5 to 11 it was held that under:

"5. It is basic to procedural law under taxing statutes that opportunity of personal hearing must be provided to an assessee before any assessment/adjudication order is passed against him. Thus, we find it strange and wholly unacceptable merely because the substantive law has changed, the revenue authorities have changed their approach and are failing to observe that mandatory requirement of procedural law. They have thus denied opportunity of hearing to the assessee.

6. Section 75(4) of the Act reads as below:

"An opportunity of hearing shall be granted where a request is received in writing from the person chargeable with tax or penalty, or where any adverse decision is contemplated against such person."

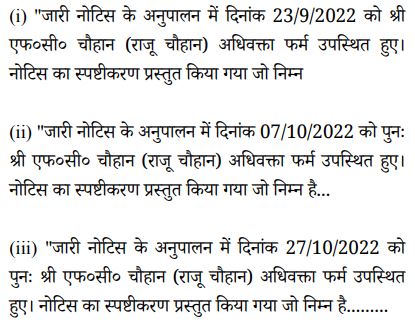

7. Perusal of the impugned order

reveals, the petitioner appeared before the competent authority on three dates.

With respect to those dates, the impugned order reads as below:

8. Thus, it is established on record that on all three dates, the petitioner had

been called to file its reply on the points specified in the respective

show-cause notice issued. The petitioner submitted its reply on each occasion.

Those replies have been extracted in the impugned order. After recording the

reply submitted on 27.10.2022, the adjudicating authority has chosen to deal

with the merits of the replies submitted and passed a merit order.

9. It transpires from the record, neither the adjudicating authority issued any

further notice to the petitioner to show cause or to participate in the oral

hearing, nor he granted any opportunity of personal hearing to the petitioner.

10. On query made, the learned Additional Chief Standing Counsel fairly submits,

in light of similar occurrences, noticed in other litigation, he had apprised

the Commissioner, Commercial Tax. In turn, the Commissioner, Commercial Tax,

Uttar Pradesh, has issued Office Memo No. 1406 dated 12.11.2024. The same has

been addressed to all Additional Commissioner to be communicated to all field

formations for necessary compliance. A copy of the same has been made available

to this Court. It reads as below:

"1. The column in which date of personal hearing has to be mentioned, only N.A. is mentioned without mentioning any date.

2. The column in which time of personal hearing has to be mentioned, only N.A. is mentioned without mentioning time of hearing.

3. In some cases, the date of personal hearing is prior to which reply to the Show Cause Notice has to be submitted this is non-est and this practice has to be discontinued. The date of reply to the Show Cause Notice has to be definitely prior to the date of personal hearing.

4. In some cases, the date of personal hearing is on the same date to which reply to the Show Cause Notice has to be submitted-this is non-est and this practice has to be discontinued. The date of reply to the Show Cause Notice has to be definitely prior to the date of personal hearing.

5. In all cases observed, the date of passing order either u/s 73(9)/74(9) etc. of the Act is not commensurate to the date of personal hearing. It is trite law that the date of the order has to be passed on the date of personal hearing. For eg., the date of furnishing reply to SCN is 15.11.2023 and date of personal hearing is 17.11.2023, then the date of order has to be 17.11.2023"

11. In view of the facts noted

above, before any adverse order passed in an adjudication proceeding, personal

hearing must be offered to the noticee. If the noticee chooses to waive that

right, occasion may arise with the adjudicating authority, (in those facts), to

proceed to deal with the case on merits, ex-parte. Also, another situation may

exist where even after grant of such opportunity of personal hearing, the

noticee fails to avail the same. Leaving such situations apart, we cannot allow

a practice to arise or exist where opportunity of personal hearing may be denied

to a person facing adjudication proceedings. "

6. Since the aforesaid dictum is applicable in the present facts and

circumstances, accordingly, the impugned orders cannot be sustained and the

orders dated 11.12.2023 & 09.09.2025 are accordingly quashed.

7. With the aforesaid, the present petition is allowed.

8. Matter is remanded to the assessing authority to pass fresh order after

giving an opportunity of hearing to the petitioner.

(Jaspreet Singh,J.)

October 9, 2025