Ernst & Young Ltd.

Versus

Assistant Commissioner

W.P.(C) 7469/2025 decided on 15-09-2025

IN THE HIGH COURT OF DELHI AT NEW DELHI

Date of Decision: 15th September, 2025

W.P.(C) 7469/2025

ERNST AND YOUNG LIMITED

.....Petitioner

Through:

Mr. Kamal Sawhney, Mr. Deepak

Thackur, Ms. Aakansha Nadhwani &

Mr. Rishwabh Mishra, Advs.

versus

ASSISTANT COMMISSIONER, DIVISION-VASANT

KUNJ &

ANR.

.....Respondents

Through:

Mr. Aditya Singla SSC CBIC with Mr.

Ritwik Saha, Ms.Arya Suresh Nair,

Ms. Shreya Lamba&Mr. Raghav

Bakshi, Advs.

CORAM:

JUSTICE PRATHIBA M. SINGH

JUSTICE SHAIL JAIN

Prathiba M. Singh, J. (Oral)

1. This hearing has been done through hybrid mode.

2. The Petitioner has filed the present writ petition under Article 226 of the Constitution of India, inter alia, challenging the non-grant of interest to the Petitioner on refunds which have been paid to the Petitioner in terms of the following Orders-in-Originals:

| Financial Year | Date of Order-in-Original |

| 2017-2018 | 19th June 2023 |

| 2018-2019 | 19th June 2023 |

| 2019-2020 | 19th June 2023 |

| 2021-2022 | 24th August, 2023 |

3. On 27th May, 2025, this Court directed both the parties to examine the decision of this Court in W.P.(C) 7485/2024 titled as M/s G.S. Industries v. Commissioner of Central Tax and GST Delhi West and make submissions before this Court.

4. Mr. Kamal Sawhney, ld. Counsel for the Petitioner had handed over a chart, in terms of which, the interest is to be calculated. The said chart for the period 2017-18, 2018-19, 2019-20 and 2020-21 had also been handed over to Mr. Aditya Singla, ld. SSC.

5. According to the Petitioner, the interest amount computed would be as under :

| Serial No. | Year | Interest Rates Applicable | Amount of Refund Claimed |

| 1. | 2017-18 | Interest @ 9% | Rs. 18,27,919/- |

| 2. | 2018-19 | Interest @ 9% | Rs. 41,84,122/- |

| 3. | 2019-20 | Interest @ 9% | Rs. 33,37,715/- |

| 4. | 2020-21 | Interest @ 9% | Rs. 31,05,158/- |

6. The total interest claim is to the tune of Rs 28,40,242/-. As per the Petitioner, the computation of the same is as under as on date:-

| Sl. No | Year | Interest Amount |

| 1. | 2017-2018 | Rs 4,67,396/- |

| 2. | 2018-2019 | Rs 9,46,759/- |

| 3. | 2019-2020 | Rs 5,86,250/- |

| 4. | 2021-2022 | Rs 2,75,380/- |

7. At this stage, the Court had put to Mr. Aditya Singla, ld. SSC for the Respondent as to what would be the interest payable in terms of the decision in W.P. (C) No. 7485/2024 titled M/s G.S. Industries vs. Commissioner of Central Tax and GST Delhi West.

8. Mr. Aditya Singla, ld. SSC submits that the matter may be remanded to the Adjudicating Authority for computing the interest in terms of M/s G.S. Industries (Supra).

9. In M/s G.S. Industries (Supra), this Court has already observed as under:-

10. The Court has considered the matter. The provisions that are relevant in determining the interest on delayed refunds are covered by Section 54 and 56 of the Central Goods and Services Tax Act, 2017 (hereinafter ‘CGST Act’). For ease of reference, the same is extracted below:

Section 54 of the CGST Act

“54. Refund of tax.— (1) Any person claiming refund of any tax and interest, if any, paid on such tax or any other amount paid by him, may make an application before the expiry of two years from the relevant date in such form and manner as may be prescribed: Provided that a registered person, claiming refund of any balance in the electronic cash ledger in accordance with the provisions of sub-section (6) of section 49, may claim such refund in the return furnished under section 39 in such manner as may be prescribed.

******

(5) If, on receipt of any such application, the proper officer is satisfied that the whole or part of the amount claimed as refund is refundable, he may make an order accordingly and the amount so determined shall be credited to the Fund referred to in section 57.

******

(7) The proper officer shall issue the order under sub-section (5) within sixty days from the date of receipt of application complete in all respects.”

Section 56 of the CGST Act

“56. Interest on delayed refunds.— If any tax ordered to be refunded under sub-section (5) of section 54 to any applicant is not refunded within sixty days from the date of receipt of application under sub- section (1) of that section, interest at such rate not exceeding six per cent. as may be specified in the notification issued by the Government on the recommendations of the Council shall be payable in respect of such refund from the date immediately after the expiry of sixty days from the date of receipt of application under the said sub-section till the date of refund of such tax:

Provided that where any claim of refund arises from an order passed by an adjudicating authority or Appellate Authority or Appellate Tribunal or court which has attained finality and the same is not refunded within sixty days from the date of receipt of application filed consequent to such order, interest at such rate not exceeding nine per cent. as may be notified by the Government on the recommendations of the Council shall be payable in respect of such refund from the date immediately after the expiry of sixty days from the date of receipt of application till the date of refund.

Explanation. ––For the purposes of this section, where any order of refund is made by an Appellate Authority, Appellate Tribunal or any court against an order of the proper officer under sub-section (5) of section 54, the order passed by the Appellate Authority, Appellate Tribunal or by the court shall be deemed to be an order passed under the said sub-section (5).”

11. The entire scheme for grant of refunds under CGST Act has been considered by this Court in Bansal International v. Commissioner of DGST (W.P.(C) 11629/2023, decided on 21st November, 2023) and the relevant portion of the judgement is extracted below:

“31. It is important to note that the rate of interest as specified in the main provision of Section 56 of the CGST Act and the proviso to Section 56 of the CGST Act is materially different. Whereas, the main provision of Section 56 of the CGST Act provides for an interest at the rate not exceeding 6% per annum, the proviso to Section 56 of the CGST Act stipulates interest at the rate not exceeding 9% per annum.

32. The learned counsel also informed this Court that the interest at the rate of 6% per annum and 9% per annum has been notified for the purposes of Section 56 of the CGST Act and the proviso to the said section, respectively. Thus, there are two separate rates of interest specified under Section 56 of the CGST Act. The interest at the rate of 6% is payable for the period commencing from a date immediately after expiry of sixty days from the date of an application under Section 54(1) of the CGST Act, however, this rate is enhanced for the period covered under the proviso to Section 56 of the CGST Act. The proviso to Section 56 of the CGST Act expressly provides that an interest at the rate of 9% per annum would be payable from the date immediately after the expiry of sixty days from the receipt of an application, which is filed as a consequent to an order passed by the Appellate Authority, Adjudicating Authority, Appellate Tribunal or a court that has attained finality. This clearly indicates that if a person’s claim for refund is a subject matter of further proceedings, which finally culminate in orders upholding the applicant’s entitlement, and yet the payment is not made within a period of sixty days from an application filed pursuant to such orders, the person is required to be compensated at a higher rate of interest, of 9% per annum. This higher rate of interest would run from the date immediately after the expiry of sixty days of the filing of such an application – that is, the application filed pursuant to the orders of the appellate fora and not the first application.

33. It is clear from a plain reading of Section 56 of the CGST Act that whereas the main provision of Section 56 of the CGST Act refers to the rate of interest applicable on the amount of refund due, which remains unpaid even after sixty days from the date of application for refund; the proviso provides for an increased rate of interest for the period that commences from the date immediately after the expiry of sixty days from the date of application which is filed pursuant to the claim for refund attaining finality in appellate proceedings. Section 56 of the CGST Act, thus, works as follows. The applicant claiming a refund is entitled to interest at the rate of 6% per annum from a date immediately after the expiry of sixty days from making an application under Section 54(1) of the CGST Act. However, if a person’s claim is denied (or if granted is not accepted by the Revenue) and the order of the Adjudicating Authority is carried in appeal to the Appellate Authority or to the Appellate Tribunal/High Court, which finally upholds the claim, the applicant may have to file a second application to secure the refund. If such application for refund filed by the person consequent to succeeding before the Appellate Authority, Appellate Tribunal or court, is not processed within a period of sixty days of filing the application, the applicant would be entitled to a higher rate of 9% per annum commencing from the date immediately after the expiry of sixty days of his application filed pursuant to the appellate orders. However, this does not mean that the rate of 6% per annum is not payable for the period commencing from the date immediately after expiry of sixty days from his first application till sixty days after filing of his second application pursuant to the appellate orders. In another words, the proviso merely enhances the interest payable to a person for the period commencing from the date immediately after sixty days from the date of his application filed pursuant to its entitlement to refund claim attaining finality.”

12. The stand of ld. Counsel for the Petitioner is that the deficiency memo was not issued within 15 days in terms of Rule 90 of Central Goods Services Tax Rules (hereinafter ‘CGST Rules’). Hence, the interest is liable to be granted for the entire period.

13. The stand of the Department is that the deficiencies were genuine and they were cleared only after two months i.e., when the documents were submitted and the same was duly acknowledged on 11th February, 2020.

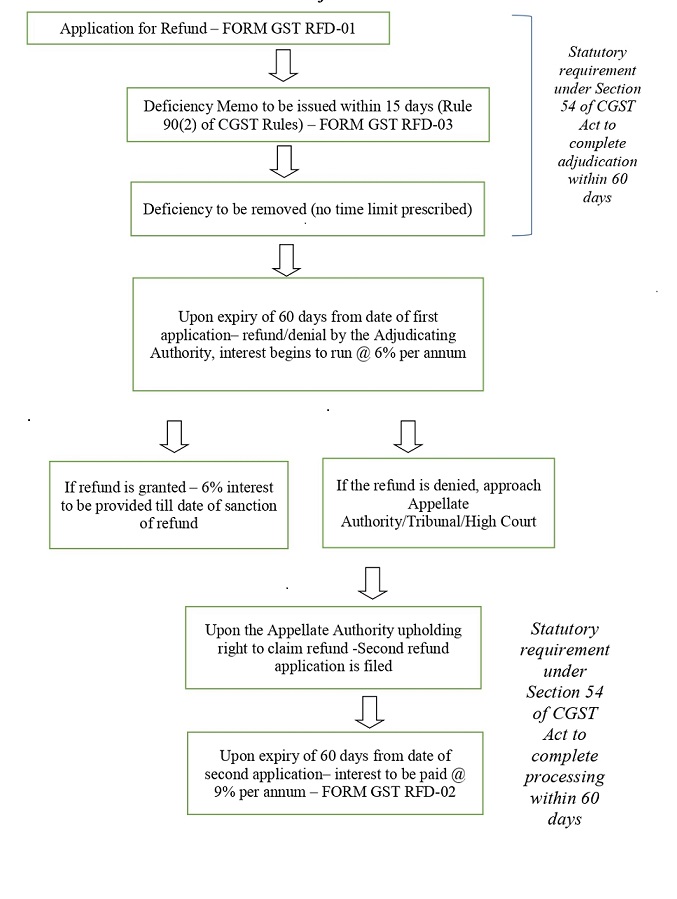

14. The scheme of payment of interest on delayed refunds can be illustrated in the following flow chart.

Note -1: For the period from FORM GST RFD-01 till the second refund application, 6% interest would be liable to be paid.

Note-2: If the second refund application is filed, then upon expiry of 60 days, interest would be liable to be paid @ 9% per annum.

Payment of Interest in an

Application for Refund under Section 56 of CGST Act read with Rule 90 of CGST

Rules

15. Considering the overall circumstances, this Court is of the view that the Petitioner cannot be denied the benefit of interest for delay caused due to the deficiency memo not having been issued within the stipulated period, i.e., between 4th/9th July, 2019 and 29th November, 2019. At the same time, the Petitioner also took about 74 days to respond to the deficiency memo i.e., between 29th November, 2019 and 11th February, 2020.”

10. In view thereof, the matter is remanded back to the Adjudicating Authority to compute the interest by applying the decision in GS Industries(Supra).

11. Let the computation be completed within two months and the interest be released to the Petitioner within one month thereafter.

12. All rights and remedies of the Petitioner are left open.

13. The present petition along with pending applications stands disposed of in the above terms.

PRATHIBA M. SINGH

JUDGE

SHAIL JAIN

JUDGE

SEPTEMBER 15, 2025