LIBERTY OIL MILLS LTD.

Versus

JOINT COMMISSIONER

WRIT PETITION NO. 8317 OF 2025 decided on 02-09-2025

2025:BHC-AS:36650-DB

IN THE HIGH COURT OF JUDICATURE

AT BOMBAY

CIVIL APPELLATE JURISDICTION

WRIT PETITION NO.8317 OF 2025

Liberty Oil Mills Limited ...Petitioner

Versus

Joint Commissioner (Appeals

Thane)

GST & Central Excise, Mumbai & Ors. ...Respondents

Mr. Aditya Ajgaonkar a/w Ms.

Rupal Shrimal & Ms. Sristi Nimodia i/by

Mr. Pulkit Tyagi for the Petitioner.

Mr. Satyaprakash Sharma a/w Ms. Sangeeta Yadav & Mr. Umesh Gupta

for Respondent Nos.1 & 2.

CORAM : M. S. Sonak &

Jitendra Jain, JJ.

DATED : 2 September 2025

ORAL ORDER:-(Per M. S. Sonak, J.)

1. Heard Mr. Ajgaonkar instructed by Mr. Tyagi for the Petitioner and Mr. Sharma for Respondent Nos. 1 and 2.

2. Rule. The Rule is made returnable immediately at the request of and with the consent of the learned counsel for the parties.

3. The Petitioner challenges the order dated 27 January 2025 issued by the Joint Commissioner (Appeals), Thane, dismissing the Petitioner’s appeal against the Assistant Commissioner’s order dated 30 March 2023 on the ground that it was filed beyond the prescribed period of limitation of three months and the condonable period of one month.

4. The order against which the appeal was instituted before the Joint Commissioner (Appeals) is dated 30 March 2023. The Petitioner contends that this order was neither uploaded on the portal nor communicated to the Petitioner at any time. After the Petitioner received a show cause notice regarding the subsequent period sometime in August 2023, the Petitioner, by communication dated 16 August 2023, applied for a copy of the order dated 30 March 2023, since the same was referred to in the said show cause notice. This copy/order was supplied to the Petitioner on 17 August 2023, and within a month, i.e., on 11 September 2023, the Petitioner instituted an appeal before the Joint Commissioner (Appeals).

5. The Joint Commissioner (Appeals) called for a report from the Assistant Commissioner. The report referred to the dispatch of the order dated 30 March 2023 to the Petitioner. A copy of this report was duly furnished to the Petitioner, and the Petitioner made its submissions on the same, and reiterated knowledge of the order dated 30 March 2023 only on 17 August 2023.

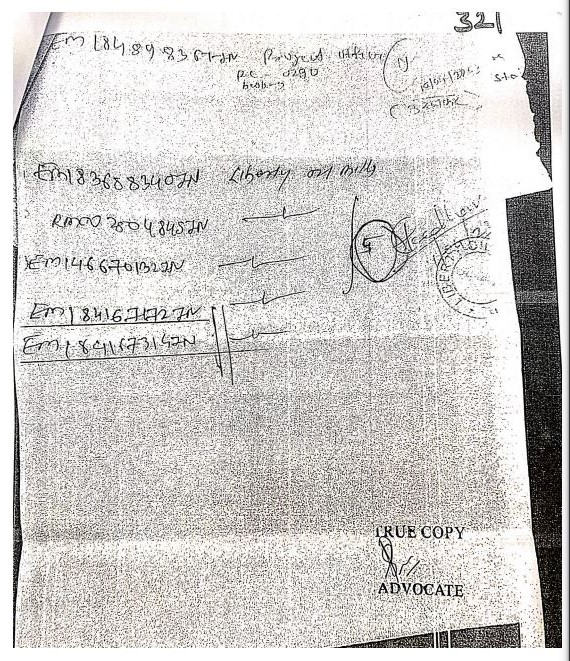

6. The Joint Commissioner (Appeals) also called for a report from the Postal Authorities. Such a report was furnished by the Postal Authorities and is now annexed to this petition at Exhibit-P (pages 319 to 321). The Joint Commissioner (Appeals) heavily relied upon this postal report to hold that the order dated 30 March 2023 was communicated to the Petitioner on 11 April 2023 and, therefore, the appeal which instituted on 11 September 2023 was barred by limitation and such delay was not even condonable given the provisions of Section 107 of the Maharashtra Goods and Services Tax Act, 2017 (MGST Act).

7. Mr. Ajgaonkar submitted that the copy of the postal report upon which the Joint Commissioner (Appeals) has placed heavy reliance was given to the Petitioner’s representative only on 23 December 2024, and the impugned order was made on 31 December 2024. He submitted that no effective opportunity was granted to the Petitioner to comment upon or dispute the correctness of the postal report, even though the report had several deficiencies.

8. The postal report, as noted above, is at Exhibit-P pages 319 to 321 of the paper book. The most crucial annexure to this postal report is on page 321, and the scanned copy of the same is reproduced below for the convenience of reference:-

9. The above annexure to the postal report, as submitted by Mr. Ajgaonkar, suggests that Figure 5 overwrites Figure 4. Mr. Ajgaonkar admitted that on 11 April 2023, the Petitioner received four documents. He referred to the fourth document, which was also an order issued by the Assistant Commissioner for a different period on the same matter, and argued that, in response to this order, the Petitioner promptly filed an appeal, and the appeal was allowed by the Appellate Authority. Mr. Ajgaonkar stated that if the Petitioner had indeed received the fifth document, i.e., the order dated 30 March 2023, there should be no reason why the Petitioner would not have appealed within the prescribed time limit, as was done with the immediately preceding document.

10. Mr. Ajgaonkar submitted that it is only after the Petitioner received a show cause notice for the subsequent period, referring to the order dated 30 March 2023, that the Petitioner immediately applied for a copy of the order dated 30 March 2023 since the Petitioner had not received such an order. Admittedly, the order dated 23 March 2023 was not even uploaded to the department's website or portal.

11. In our judgment, considering the above circumstances, the Joint Commissioner (Appeals), should have granted an effective opportunity to the Petitioner for dealing with the postal report since ultimately, in the impugned order, much reliance has been placed on this document. Rather than remanding the matter on this issue, we have heard the learned counsel for the parties and by applying the test of preponderance of probabilities, which is precisely the test which the Joint Commissioner (Appeals) has adopted (by styling this test as one of appreciating circumstantial evidence), we think that the benefit should have been extended to the Petitioner rather than to the Respondents.

12. The postal document shows some overwriting, giving the impression that only the four documents were delivered by the postal authorities and not the fifth document, which is the order dated 30 March 2023. Furthermore, the Petitioner’s conduct in appealing the 4th document, a decision made by the Assistant Commissioner on the same issue, also indicates that the Petitioner was not otherwise inactive. If the Petitioner had indeed received the 5th document, that is, the order dated 30 March 2023, along with the other four documents on 11 April 2023, there would have been no reason for the Petitioner not to have appealed it within the prescribed period of limitation. The Petitioner has gained no undue advantage in the matter.

13. The record also shows that the Petitioner, upon coming to know that the order dated 30 March 2023 was made, immediately applied for a copy of the same and, upon its furnishing, instituted the appeal within less than a month. If all these circumstances are considered cumulatively, then we are inclined to accept the Petitioner’s case about the order dated 30 March 2023 not being served upon them on 11 April 2023, but that it was obtained by the Petitioner only on 17 August 2023. Thus construed, the appeal instituted by the Petitioner on 11 September 2023 could not have been said to be barred by the limitation prescribed under Section 107 of the MGST Act.

14. At this stage, we also record Mr. Ajgaonkar’s statement made on instructions that, for the inconvenience that might have been caused, the Petitioner is willing to pay some costs. He suggested that the Petitioner could be directed to pay some amount to a Government Hospital as a part of its corporate social responsibility instead of imposing any costs.

15. Mr. Ajgaonkar’s statement, made on instructions, that the Petitioner would donate an amount of Rs. 25,000/- to the Government K.E.M. Hospital within two weeks from today, is accepted. A compliance report must be filed in the Registry within four weeks and must also be produced before the Joint Commissioner (Appeals). The account details of the K.E.M. Hospital are as under: -

| Bank Account of Hospital | :- | Poor Box Charity Fund, K.E.M. Hospital, Mumbai |

| Bank Account Number of Hospital | :- | 99350100000877 (S.B.) |

| Bank and Branch | :- | Bank of Baroda, Parel Branch |

| Address. Tel. No. Fax. No. and e-mail of the concerned Bank | :- | Bank of Baroda, Madina Manzil, 88, Dr. Ambedkar Road, Mumbai – 400 012, Maharashtra, 022-24713820 dppare@bankofbaroda.com |

| MICR Code Number | :- | 400012246 |

| IFSC Number | :- | BARB0DBPARE (5th Letter is Zero) |

| PAN | :- | AAATK3087D |

| Type of Account | :- | Saving A/C |

16. For all the above reasons, we set aside the impugned order dated 27 January 2025 made by the Joint Commissioner (Appeals) and restore the Petitioner’s appeal to the file of the Joint Commissioner (Appeals) for adjudication on merits and in accordance with law. All contentions of all parties on the merits are explicitly left open.

17. The Rule is made absolute in the above terms.

18. All concerned are to act on an authenticated copy of this order.

| (Jitendra Jain, J.) |

(M. S. Sonak, J.) |