Hind Paper House

Versus

The Commissioner State Goods And Service Tax

W.P.(C) 3294/2025 decided on 04-08-2025

IN THE HIGH COURT OF DELHI AT NEW DELHI

Date of decision: 4th August 2025

W.P.(C) 3294/2025 & CM APPL. 15563/2025

HIND PAPER HOUSE

.....Petitioner

Through:

Mr. Vijay Gupta, Mr. Arihant Jain &

Mr. Hari Om Thakur, Advs.

versus

THE COMMISSIONER STATE GOODS AND

SERVICE TAX

DELHI & ANR.

.....Respondents

Through:

Ms. Vaishali Gupta, Adv. for

R/GNCTD.

CORAM:

JUSTICE PRATHIBA M. SINGH

JUSTICE SHAIL JAIN

Prathiba M. Singh, J. (Oral)

1. This hearing has been done through hybrid mode.

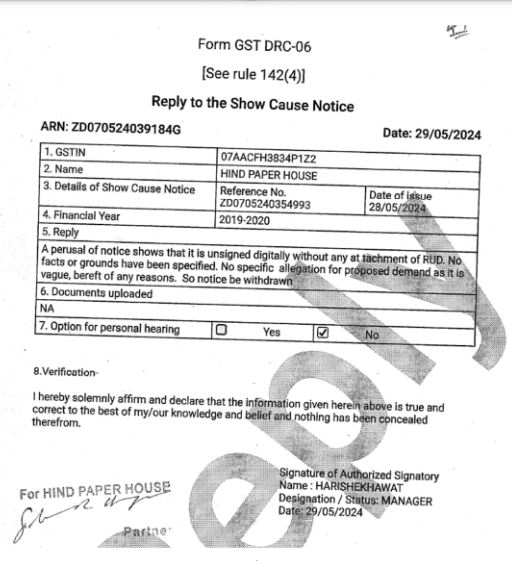

2. The present petition challenges the impugned Show Cause Notice dated 28th May, 2024 (hereinafter “impugned SCN”) as also the consequential order dated 24th August, 2024 (hereinafter “impugned order”). The writ petition also challenges the order dated 16th December, 2024 by which the application for rectification by the Petitioner was also rejected.

3. The brief background is that a Form DRC-01 - Summary of the Show Cause Notice was issued on 28th May, 2024 and is stated to have been uploaded on the same date. The said Form DRC-01 raised a demand of Rs. 4,04,61,076/- in respect of the tax period April, 2019 to March, 2020. A date for personal hearing was also fixed on 28th June, 2024 at 11:00 a.m. As per the said Form DRC-01, the impugned SCN along with supporting documents was attached and uploaded along with the said Form. However, as per the Petitioner, neither the impugned SCN nor the supporting documents had been uploaded along with Form DRC-01.

4. The Petitioner challenges the order dated 24th August, 2024 on various grounds, inter alia, as under:

i. That the impugned SCN was not uploaded and only Form DRC-01 was uploaded that too without any Relied upon Documents (hereinafter “RUDs”).

ii. That the Form DRC-01 is not equivalent to a Show Cause Notice.

iii. That the RUDs were allegedly served through speed post on 15th June, 2024 only as per the Department which is also beyond the period of limitation.

iv. The impugned order was passed on 24th August, 2024 without providing a proper hearing.

v. That the Input Tax Credit was already reversed by the Petitioner and the said records were available with the Department prior to passing the impugned order.

5. On all these grounds quashing

of the impugned SCN and the impugned order is sought.

6. On behalf of the Respondent-Ms. Gupta, ld. Counsel has handed across a short

affidavit dated 30th July, 2025, signed by one Ms. Gomti Mattu, GSTO Ward 11,

Department of Trade & Taxes, GNCTD which states as under:

“3. It is humbly submitted that a Show Cause Notice (DRC-01) under section 73 of the DGST Act was issued to the petitioner on 28.05.2024 (Ref No. ZD0705240354993). At the relevant time, due to technical glitch in Emsigner, GSTN had removed the Emsigner integration with Assessment module in GST BOWEB portal, as a result of which detailed summary of DRC-01 which was generated from the portal was not issued and could not be attached with the Show Cause Notice dated 28.05.2024.

4. It is submitted that after removing the technical glitch on the portal, hard copy of the detailed summary along with the Show Cause Notice dated 28.05.24 was sent through speed post (ED2940507291N) on 13.06.2025. It is submitted, on an enquiry from the Department of Posts, a letter dated 07.04.2025 was received confirming the delivery of the Speed Post to the Petitioner on 15.06.2024.

A copy of the DRC-01 along with detailed summary dated 28.05.2024 is annexed herewith and marked as ANNEXURE-1.

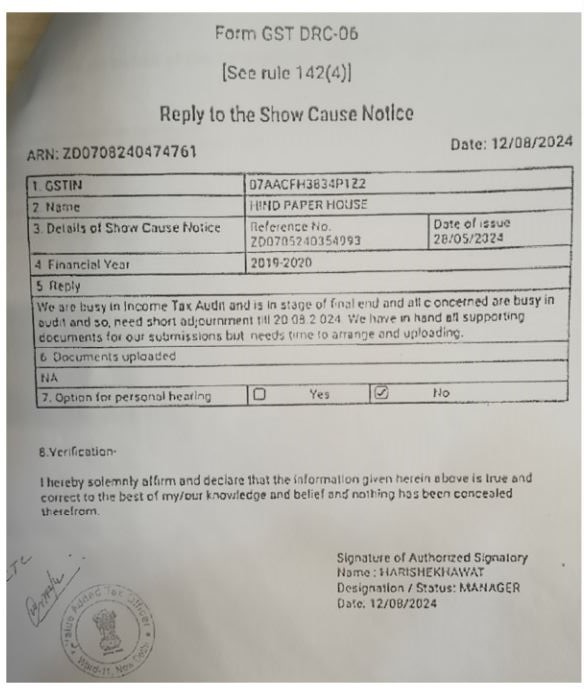

A copy of letter dated 07.04.2025 is annexed herewith and marked as ANNEXURE -2.5. It is submitted that a reply dated 12.08.2024 was submitted that by the Petitioner to the SCN dated 28.05.2024 wherein it stated that, "We are busy in Income Tax Audit and is in stage of final end and all concerned are busy in audit and so, need short adjournment till 20.08.2024. We have in hand all supporting documents for our submissions but needs time to arrange and uploading." It is humbly submitted that a perusal of the reply dated 12.08.2024 reveals that the petitioner was in receipt of the SCN along with the detailed summary as no such objection was raised by the Petitioner.

A copy of the reply dated 12.08.2024 is annexed herewith and marked as ANNEXURE -3.

6. That after following due process of law, Demand order dated 24.08.2024 was issued by the Respondent. The petitioner filed a rectification dated 24.11.2024 of the DRC-07 dated 24.08.2024 without any supporting documents and resultantly, the same was rejected.”

7. It is her submission that it

was due to a technical glitch that the RUDs was not uploaded on the portal,

though, the Form DRC-01 was itself uploaded on 28th May, 2025. The

RUDs along with the proper documents were served upon the Petitioner on 15th

June, 2024. The proof of delivery is also placed on record. In addition, it is

the stand of the Department that on three occasions, the Petitioner sought time

to file a reply and no reply on merits was forthcoming.

8. The Court has heard ld. Counsel for the parties. Clearly, the Form DRC-01

which was uploaded on the portal would not be sufficient for any party to file a

reply, as the details of the demand raised and the allegations against the

Petitioner have not been mentioned therein. The service of the RUDs, as per the

Department, itself happened on 15th June, 2024. This service is

disputed by the Petitioner. Since the speed post tracking receipt and the

register of the speed post from the postal depot has been placed on record along

with the short affidavit by the Department, in the opinion of this Court, the

same cannot be disputed.

9. The Petitioner repeatedly sought adjournments on 29th May, 2024,

12th August, 2024 as also on 22nd August, 2024. On all these

occasions, the Petitioner did not deal with the issue on merits. In the three

replies filed by the Petitioner including the last one i.e., on 22nd August,

2024, no substantive argument has been raised by the Petitioner. The first reply

was filed 29th May, 2024 wherein it was stated as under:

10. The second reply was on 12th August, 2024 in which it was stated as under:

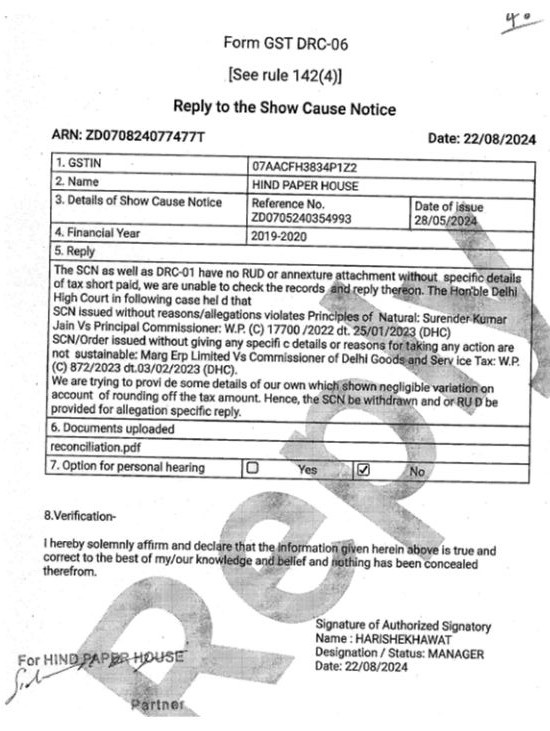

11. The last reply is dated 22nd August, 2024 in which it was stated as under:

12. According to the Petitioner, the summary report for notice 2019-20 which was

uploaded on 22nd August, 2024 would have shown that the Input Tax

Credit was reversed.

13. However, a perusal of the last reply also shows that the Petitioner again

sought time for filing a specific reply along with a request to provide the RUDs.

14. The impugned order itself was passed on 24th August, 2024. It is admitted

that the Petitioner did not appear at the hearing which was fixed and had merely

uploaded the reply along with the so-called summary report. According to the

Petitioner, no date of hearing was fixed on 24th August, 2024.

15. After considering the entire chronology of events, it is clear that there

have been errors both by the Department as also by the Petitioner. The initial

error of the Department, was not to upload the entire summary, the impugned SCN

along with the RUDs on the portal on 28th May, 2025. However, once

the physical copy of the same was received on 15th June, 2024 the

Petitioner chose not to file any detailed reply and kept seeking adjournments.

16. Under these circumstances, in the opinion of this Court, the impugned order

deserves to be set aside and the Petitioner deserves to be given a hearing

before the Adjudicating Authority.

17. The plea of the Petitioner that the impugned SCN is beyond limitation may

also be raised before the Adjudication Authority.

18. The short affidavit handed across by the Department is taken on record.

19. All contentions of the parties are left upon. The petition is disposed of in

these terms. Pending applications, if any, are also disposed of.

PRATHIBA M. SINGH

JUDGE

SHAIL JAIN

JUDGE

AUGUST 4, 2025