Bharat Mint And Allied Chemicals

Versus

State of U.P.

WRIT TAX No. - 2527 of 2025 decided on 30-05-2025

Neutral Citation No. - 2025:AHC:93927-DB

Chief Justice's Court

Case :- WRIT TAX No. - 2527 of 2025

Petitioner :- Bharat Mint

& Allied Chemicals

Respondent :- State of U.P. and another

Counsel for Petitioner :- Abhinav Mehrotra,Bhavna Mehrotra,Satya

Vrata Mehrotra

Counsel for Respondent :- C.S.C.

Hon'ble Arun Bhansali,Chief

Justice

Hon'ble Kshitij Shailendra,J.

1. This writ petition has been filed by the petitioner aggrieved of the notice dated 25.02.2025 issued by respondent no. 2 under Section 74 of the Goods and Services Tax Act, 2017 (for short 'the Act') to the petitioner. The petitioner was earlier issued a notice under Section 73 of the Act, indicating as many as ten issues. The petitioner filed reply to the said show cause notice on all the aspects raised.

2. In the order passed under Section 73 (9) of the Act dated 20.02.2025, the authority in relation to the issues raised in Point Nos. 1, 6, 8 & 10 observed that as further investigation is required, a fresh notice would be issued and on rest of the aspects, the plea raised/response filed by the petitioner was accepted, where after the present notice under Section 74 of the Act has been issued.

3. Submissions have been made that the notice issued under Section 74 of the Act is without jurisdiction and deserves to be quashed and set aside, inasmuch as, none of the ingredients as required for issuance of notice under Section 74 of the Act are neither present nor have been alleged in the notice and, therefore, the notice is bad.

4. Reliance has been placed on an order passed by this Court in M/s Vadilal Enterprises Ltd. Vs. State of U.P. And 2 others: Writ Tax No. 2486 of 2025, decided on 23.05.2025.

5. Learned Standing Counsel contested the submissions made. It was indicated that it is not necessary to make allegations in the notice under Section 74 of the Act by using the language of Section 74 of the Act. The facts themselves speak for the ingredients and, therefore, the plea raised in this regard has no substance. However, it is not denied that the facts of order passed in the case of M/s Vadilal Enterprises Ltd. (Supra), are similar to the present case.

6. We have considered the submissions made by learned counsel for the parties and have perused the material available on record.

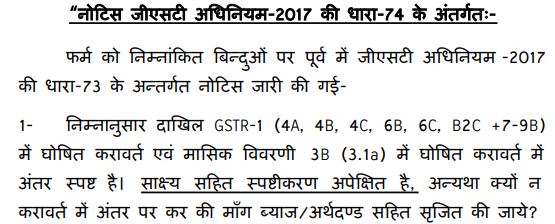

7. The notice issued by the respondents under Section 74 of the Act reads as under:

| Sr. | Issue | Taxable Value |

| A | B2B Supply | 1808927201.20 |

| B | B2C Supply (if any) (GSTR1_7+GSTR1_5A_5B) | 0.00 |

| C | Advances Received (if any) (GSTR1_11A_1) | 0.00 |

| D | Sub Total (A)+(B)+(C) | 1808927201.20 |

| E | Credit/Debit Note (if any) (GSTR1_9B) | 2521305.23 |

| F | Advances adjustment if any (GSTR1_11B_1) | 0.00 |

| G | Subtotal (D)-[(E)+(F)] | 1806405895.97 |

| H | Outward taxable supplies (other than zero rated, nil rated and exempted) (GSTR3B_(3.1A)) | 1560634258.47 |

| I | Difference (G) - (H) | 245771637.50 |

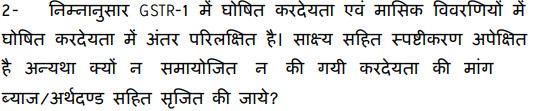

| Sr | Issue | SGST | CGST | IGST | CESS | TOTAL |

| A | B2B Tax | 73224424.03 | 73224424.03 | 41915460.40 | 0.00 | 188364308.46 |

| B | B2C Tax (if any) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| C | Advances Received (if any) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| D | Subtotal (A) + (B) + (C) | 73224424.03 | 73224424.03 | 41915460.40 | 0.00 | 188364308.46 |

| E | Credit/Debit Note (if any) | 178278.31 | 178278.31 | 0.00 | 0.00 | 356556.6 |

| F | Advance adjustment if any | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| G | Subtotal (D)-[E) +(F)] | 73046145.72 | 73046145.72 | 41915460.40 | 0.00 | 188007751.84 |

| H | Outward taxable supplies (other than zero rated, nil rated and exempted) | 79848405.83 | 79848405.83 | 22383814.00 | 0.00 | 182080625.66 |

| I | Difference (G) - (H) |

- 6802260. 11 |

- 6802260. 11 |

19531646.40 | 0.00 | 5927126.18 |

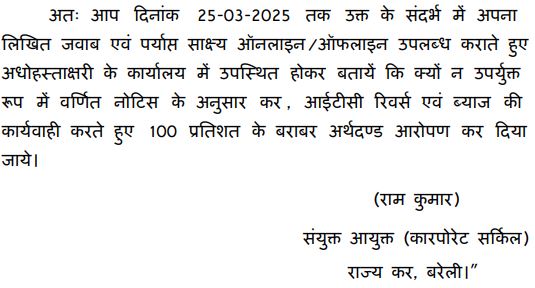

| S.No. | Issue | Taxable Value |

| A | EWB Total Tax (in lakhs) | 2043.49 |

| B | GSTR-3B Total Tax (in lakhs) | 1939.25 |

| C | Difference (A-B) (in lakhs) | 104.24 |

| Tax rate % | Turn over | Tax period | Act | POS (Place of Supply | Tax | Interest | penalty | Others/ RITC | TOTAL | ||

| From | To | ||||||||||

| 1 | Apr-20 | Mar-21 | SGST | NA | 12014260 | 9527144 | 12014260 | 0 | 33555664 | ||

| 2 | Apr-20 | Mar-21 | CGST | NA | 12014260 | 9527144 | 12014260 | 0 | 33555664 | ||

| 3 | Apr-20 | Mar-21 | IGST | UP | 34246367 | 27156900 | 34246367 | 0 | 95649634 | ||

| TOTAL | 58274887 | 46211187 | 58274887 | 0 | 162760961 | ||||||

8. This Court in the case of M/s Vadilal Enterprises Ltd. (Supra) wherein the same officer in identical circumstances had adopted the similar method i.e. while deciding the notice under Section 73 of the Act, finding paucity of time, left the issues undecided and issued notice under Section 74 of the Act, came to the following conclusion:

"8. A bare perusal of the language indicated therein clearly reflects that a reference to notice issued under Section 73 has been made and that the explanation filed, could not be verified and, therefore, further explanation was expected. The very fact that the respondents have sought further explanation and not a word has been indicated that the petitioner, inter alia has committed fraud,has given wilful misstatement or has suppressed material facts, which are the ingredients based on which provisions of Section 74 of the Act can be invoked necessarily shows lack of requisite ingredients in the notice.

9. In view of the above fact situation, the jurisdictional aspect for invoking provisions of Section 74 of the Act insofar as the present notice is convened, being not present, the same cannot be sustained.

10. Consequently, the petition is allowed.

11. Notice issued under Section 74 of the Act is quashed and set aside. However, the respondents would be free to take appropriate/ fresh proceedings in accordance with law. "

9. The present case is squarely covered by order in the case of M/s Vadilal Enterprises Ltd. (Supra).

10. Consequently, the writ petition is allowed. The notice issued under Section 74 of the Act is quashed and set aside. However, the respondent would be free to take appropriate/fresh proceedings in accordance with law.

Order Date :- 30.5.2025

(Kshitij Shailendra, J) (Arun Bhansali, CJ)