Agrawal Agro Centre

Versus

State Of Chhattisgarh

WPT No. 101 of 2019 decided on 22-07-2025

2025:CGHC:34773

HIGH COURT OF CHHATTISGARH AT BILASPUR

WPT No. 101 of 2019

M/s Agrawal Agro Centre Through

Its Proprietor Sanjay Kumar Agrawal S/o Shri

Ramkumar Agrawal, Aged About 49 Years, Kotwali, Raigarh, District- Raigarh,

Chhattisgarh., District : Raigarh, Chhattisgarh

... Petitioner.

versus

1 - State Of Chhattisgarh Through

Secretary, Department Of Commercial Tax/gst,

Mantralaya, Mahanadi Bhawan, New Raipur, District- Raipur, Chhattisgarh.,

District :

Raipur, Chhattisgarh

2 - Commissioner State Tax,

Department Of Commericial Tax, Gst Bhawan, North Block,

Sector-19, Atal Nagar, District- Raipur, Chhattisgarh., District : Raipur,

Chhattisgarh

3 - Joint Commissioner (Appeal)

State Tax, Jai Ambe Complex, Opposite New Bus Stand,

Raipur, Road Bilaspur, Chhattisgarh., District : Bilaspur, Chhattisgarh

4 - Assistant Commissioner State

Tax, Kelo Vihar Colony, Raigarh, District- Raigarh,

Chhattisgarh., District : Raigarh, Chhattisgarh

... Respondents

For Petitioner : Mr. Amit Soni appears on behalf of Mr. Sunil Otwani, Adv.

For Respondents/State : Mr. Dilman Rati Minj, Govt. Advocate.

SB : Hon'ble Shri Justice Deepak Kumar Tiwari

Order on Board

22.07.2025

1. The petitioner has filed this petition under Article 226 of the Constitution of India and prayed for the following reliefs:

"10.1 That, this Hon'ble Court may kindly be pleased to issue a suitable writ/direction for setting aside not only the order but also revision proceeding bearing number revision/01/2019/176 pending before the respondent No.2. The order dated 01.06.2019 (Annexure-P/1).

10.2 That, this Hon'ble Court may kindly be pleased to grant any other relief(s)/order(s)/direction(s) in favour of the petitioner, which may deem fit and proper in the facts and circumstances of the case, in the interest of justice.

10.3 That, this Hon'ble Court may kindly be pleased to order refund of the Pre-deposit amount.

10.4 Cost of the Petition."

2. Learned counsel for the petitioner submits that the petitioner is proprietorship firm which is duly registered under the provisions of Chhattisgarh Goods and Service Tax Act, 2017 (for short the "Act 2017"). On 22.05.2019, the Assistant Commissioner, Raigarh while exercising power vested under the Act 2017 has intercepted the vehicle bearing Registration No.CG-10-C-4353 and after inspection of the documents has reached to the conclusion on the basis of presumption that the goods were transported twice on the strength of same e-way bill and invoice, as a result of which, the order was passed by the Assistant Commissioner on 22.05.2019 imposing tax and penalty upon the petitioner. He submits that against the said order, the petitioner preferred an appeal under Section 107 of the Act 2017 which was allowed by the order dated 30.05.2019. However, learned Commissioner has passed the impugned order dated 01.06.2019 (Annexure-P/1) by virtue of which the order passed by the Appellate Authority was stayed. He submits that learned Commissioner has wrongly passed the said order by exercising the power vested under Section 108 of the Act 2017 suo motu and same has been passed in a cryptic manner without assigning any reason.

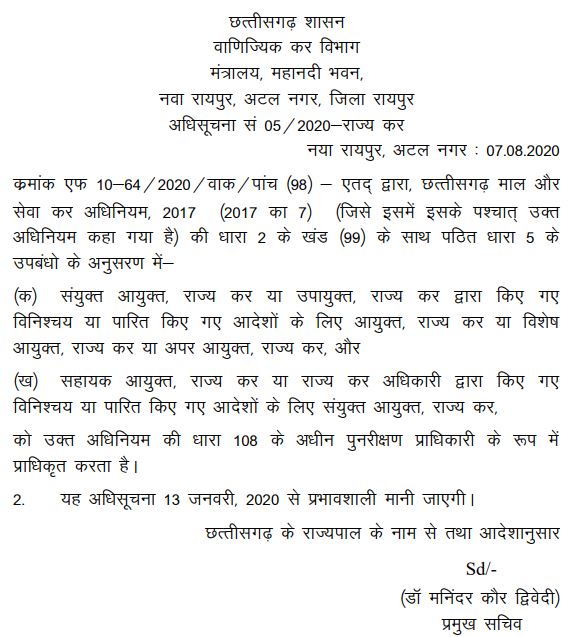

3. Learned counsel for the petitioner further submits that while passing the impugned order dated 01.06.2019 (Annexure-P/1) the competent Authority was not in existence as no notification was issued in terms of sub section (2) of Section 99 of the Act 2017 and same has been issued later on by the Order/Notification dated 07.08.2020 which is also filed by the respondent as Annexure-R/1. In such circumstances, the impugned order dated 01.06.2019 is void ab initio and the same deserves to be setaside.

4. Learned State counsel would fairly admit the fact that at the time of passing of order dated 01.06.2019, no notification was issued by the State Government in terms of sub section (2) of Section 99 of the Act 2017. He submits that by the Notification dated 07.08.2020 the Competent Officers were authorized as Revisional Authority by the State Government by virtue of sub Section (2) of Section 99 read with Section 5 of the Act 2017. He further submits that the matter may be remitted back to the concerned Authority for fresh adjudication and to pass speaking order.

5. Heard learned counsel for the parties and perused the documents annexed with the petition carefully.

6. Perusal of the impugned order dated 01.06.2019 (Annexure-P/1) and Notification dated 07.08.2020 would show that though the concerned Authority has passed the order, however, on the date of passing of such order, no notification was issued enabling the said Authority to pass such order. The Notification was issued on 07.08.2020, whereby, the concerned Officers were authorized as Revisional Authority. The said Notification was issued by virtue of sub section (2) of Section 99 read with Section 5 of the Act 2017 which is reproduced hereunder:-

7. Learned State counsel has filed the aforesaid Notification as AnnexureR/1 with his reply, from which, it appears that in terms of sub section (2) of Section 99 read with Section 5 of the Act 2017 the concerned Officers/Authorities have been authorized as Revisional Authority. Hence, it is crystal clear that on the date of passing of the impugned order the Authority who has passed the same was not the competent Authority.

8. Apart from the above, in the order impugned, no cogent reasons have been assigned for exercising power under Section 108 of the Act 2017 for suo motu revision. Section 108 of the Act 2017 empowers the Authority that if certain facts are not decided in appeal, the Authority may exercise its jurisdiction and in order to exercise such jurisdiction, the primary satisfaction should be recorded by the said Authority, as the order without reasons cannot be sustained. To give reasons is the rule of natural justice. The reason is the heartbeat of every conclusion and without the same it becomes lifeless.

9. In view of the above, the impugned order dated 01.06.2019 is not sustainable and the same is hereby set-aside. The concerned Authority is hereby directed to drop the revision proceedings forthwith. However, it is made clear that if law empowers to exercise revisional jurisdiction, then the respondents/competent Authority may exercise the same and after providing sufficient opportunity of hearing to the petitioner, the Authority may pass fresh order in accordance with law. Further, the proceeding, if any, is to be initiated against the petitioner, the same shall be initiated within 15 days from the date of receipt/communication of this order. Ordered accordingly.

10. With the aforesaid observation/direction, this petition is allowed to the extent indicated above.

Sd/-

(Deepak Kumar Tiwari)

Judge