Vadilal Enterprises Ltd.

Versus

State Of U.P.

WRIT TAX No. - 2486 of 2025 decided on 23-05-2025

Neutral Citation No. - 2025:AHC:87915-DB

Chief Justice's Court

Case :- WRIT TAX No. - 2486 of 2025

Petitioner :- M/S Vadilal

Enterprises Limited

Respondent :- State Of U.P. And 2 Others

Counsel for Petitioner :- Pooja Talwar

Counsel for Respondent :- C.S.C., Ankur Agarwal (SC)

Hon'ble Arun Bhansali,Chief

Justice

Hon'ble Kshitij Shailendra,J.

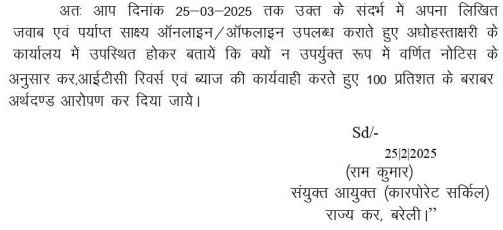

1. This writ petition is directed against notice dated 25.02.2025 issued under Section 74 of the Goods and Services Tax Act, 2017 (for short ‘the Act’) to the petitioner raising a demand of Rs.2601537910/-.

2. Challenge has been laid to the said notice inter alia on the ground that neither the ingredients as required under Section 74 of the Act are present nor have been alleged and, therefore, the notice is bad.

3. Submission have been made that on the issues for which a 74 notice has been issued, earlier a notice under Section 73 along with other aspects was issued to the petitioner to which response along with documents was filed. However, while passing the order on notice under Section 73 of the Act on 22.2.2025, it was observed that on account of the difference between the document produced during the departmental audit and during proceedings under Section 73, a detailed inquiry is required and for that a separate notice under Section 74 would be issued.

4. Whereafter the present notice has been issued wherein, no allegations, as required under Section 74 of the Act, have been made and, therefore, the notice is without jurisdiction and deserves to be quashed and set aside. Reliance has been placed on Ajnara Realtech Limited vs. State of Uttar Pradesh : 2025 NTN (Vol. 87)-521 which judgement in turn has relied on HCL Infotech Ltd. vs. Commissioner, Commercial Tax : 2024 86 NTN DX 751.

5. Learned Standing Counsel made vehement submissions that the material, which is on record, clearly reflects that there has been suppression on part of the petitioner and, therefore, the notice impugned cannot be said to be bad. Further submissions have been made that even if the ingredients as indicated under Section 74 of the Act, are not indicated in the same language, the substance of the notice has to be examined and, therefore, the petition deserves dismissal.

6. We have considered the submissions made by learned counsel for the parties and have perused the material available on record.

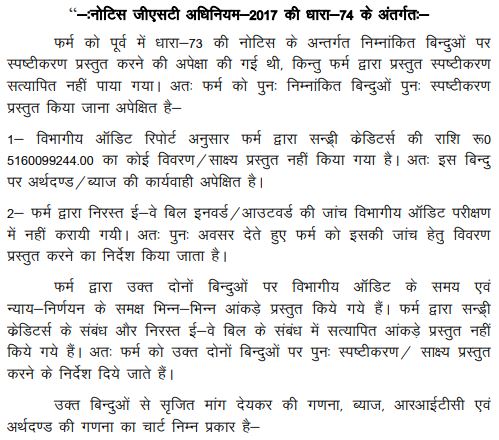

7. The notice issued by the respondents under Section 74 of the Act reads as under:

| Tax rate % | Turn over | Tax period | Act | POS (Place of supply) | Tax | Interest | Penalty | Others /RITC | TOTAL | ||

| From | To | ||||||||||

| 1 | Apr-20 | Mar-21 | SGST | NA | 465598328 | 369213096 | 465598328 | 0 | 1300409752 | ||

| 2 | Apr-20 | Mar-21 | CGST | NA | 465598328 | 369213096 | 465598328 | 0 | 1300409752 | ||

| 3 | Apr-20 | Mar-21 | IGST | UP | 257218 | 203970 | 257218 | 0 | 718406 | ||

|

Total |

931453874 | 738630162 | 931453874 | 0 | 2601537910 | ||||||

8. A bare perusal of the language indicated therein clearly reflects that a reference to notice issued under Section 73 has been made and that the explanation filed, could not be verified and, therefore, further explanation was expected. The very fact that the respondents have sought further explanation and not a word has been indicated that the petitioner, inter alia has committed fraud, has given wilful misstatement or has suppressed material facts, which are the ingredients based on which provisions of Section 74 of the Act can be invoked necessarily shows lack of requisite ingredients in the notice.

9. In view of the above fact situation, the jurisdictional aspect for invoking provisions of Section 74 of the Act insofar as the present notice is convened, being not present, the same cannot be sustained.

10. Consequently, the petition is allowed.

11. Notice issued under Section 74 of the Act is quashed and set aside. However, the respondents would be free to take appropriate/fresh proceedings in accordance with law.

Order Date :- 23.5.2025

(Kshitij Shailendra, J) (Arun Bhansali, CJ)