A N Enterprises

Versus

Additional Commissioner

WRIT TAX No. - 366 of 2021 decided on 19-11-2024

Court No. - 2

Case :- WRIT TAX No. - 366 of 2021

Petitioner :- M/S A.N.

Enterprises

Respondent :- Additional Commissioner And 2 Others

Counsel for Petitioner :- Suyash Agarwal

Counsel for Respondent :- C.S.C.

Hon'ble Piyush Agrawal,J.

1. Heard Mr. Suyash Agarwal for the petitioner and Mr. Ravi Shanker Pandey, learned ACSC for the State -respondents.

2. By means of present petition, the petitioner is assailing the order dated 26.11.2020 passed by respondent no. 1 in GST Appeal No. 2275 of 2019 (A.Y. 2019-20).

3. Learned counsel for the petitioner submits that the petitioner is a registered dealer having GSTIN No. 09BOCPA6668F1ZX and engaged in the trade of scrap. The petitioner in the normal course of business has sold aluminum cable through tax invoice no. 55 dated 29.9.2019 along with E-way Bill No. 4510 8748 1110 dated 29.9.2019 and G.R. No. 371 dated 29.9.2019. During transit on its onward journey, the goods were intercepted and on its physical verification, it is alleged that in stead of aluminum cable, PVC Aluminum mixed cable (Feeder Cable) was found. On the said pretext, the goods were seized and proceedings under Section 129 of the Act was initiated. He submits that aluminum cable was in transit which has HSN Code - 8544 and same rate of tax is upon PVC aluminum mixed cable (Feeder cable). The petitioner has no intention to evade the payment of tax. Hence the proceeding is illegal and arbitrary in manner. He submits that against the proceedings under Section 129 of the Act, an appeal was filed in which new ground was taken that the goods in question was under valued. He submits that no show cause notice was issued in respect of under valuation of the goods and for the first time the said plea was taken before the appellate authority. He submits that the Commissioner, Commercial Tax on 9.5.2018 has issued a circular stating therein that the goods shall not be detained on the ground of under valuation.

4. In support of his submission, he relied upon the judgement of this Court passed in Writ Tax No. 33 of 2022 (M/s Shamhu Saran Agarwal and company Vs. Additional Commissioner Grade -2 and others) decided on 31.1.2024.

5. Per contra, learned ACSC has supported the impugned order.

6. After hearing learned counsel for the parties, the Court has perused the records.

7. On perusal of the records, it shows that the goods in question were accompanying with all the relevant documents i.e. e-way bill, GR, tax invoice etc. and in the e-way bill, the HSN Code 8544 were specifically been mentioned and quantity 3520 was mentioned. There was no difference in HSN Code and quantity as well as the tax leviable on the goods in question. However only on the ground that on physical verification PVC Aluminum Mixed Cable (Feeder Cable) was found, the goods were detained.

8. Further before the appellate authority, new ground in respect of under valuation of the goods, was taken. The Commissioner, Commercial Tax, UP by way of Circular dated May 9, 2018 has specifically stated that no goods shall be detained on the ground of under valuation.

9. This Court in the case of M/s Shamhu Saran Agarwal (supra) has held as under:-

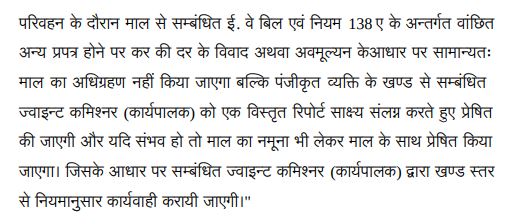

"4. It is evident from the circular issued by the Commissioner, Commercial Tax, Uttar Pradesh dated May 9, 2018 that the goods are not to be detained on the ground of under valuation. The relevant paragraph of the aforesaid circulate is extracted below:-

5. Furthermore, Mr. Agarwal, appearing for the petitioner, has relied upon a judgment of the Kerala High Court in the case of Hindustan Coca Cola Private Limited vs. Assistant State Tax Officer reported in 2020 NTN (73)-58 wherein the Kerala High Court held as follow:-

“7. From the perusal of the aforementioned findings, it is irresistibly concluded that in case of a bonafide dispute with regard to the classification between a transitor of the goods and the squad officer, the squad officer may intercept the goods and detain them for the purpose of preparing the relevant papers for effective transmission to the judicial assessing officers and nothing beyond. In the present case, it is a case of bonafide miscalculation as to whether the goods would be exigible to 12% or 28%. The judgment cited in N.V.K Mohammed Sulthan Rawtger's case (supra) was also a case where the petitioner firm was a manufacturer of 'Ground Betel Nuts (Arecanuts)' and registered with the Tamil Nadu under the Goods and Service Tax Act. The goods were intercepted by the inspecting authority to be in contravention of the misbranding. By relying upon the decision in J.K Synthetics Limited V. Commercial Taxes Officer, 1994 (4) SCC 276, it was held that the charging provisions must be construed strictly but not the machinery provisions which would be construed like any other statute.”

6. In the present case, there is no dispute that the invoice, e-way bill and all other relevant documents were accompanied with the goods. Furthermore, there was no mismatch in the description of the goods with the documents. The only ground for detention of the goods was that the valuation of the goods as per the invoice was not correct. In my view, this is not a valid ground for detaining the goods as the officer concerned was not competent to carry out such detention.

7. In the event of under valuation, appropriate notice under Sections 73 or 74 of the Uttar Pradesh Goods and Service Tax Act, 2017 (hereinafter referred to as “the Act”) is required to be issued as per the procedure provided therein. If the Court holds such a detention to be valid, it would be open to the authorities to carry out detention on their whims and fancies. The detention of the goods in such a scenario is not envisaged under the Act and the officers have not been vested with such a power to detain the goods and thereafter impose penalty under Section 129 of the Act. Specific provisions have been provided for detection of under valuation and the GST officials have to adhere to the same. It is to be noted that only after issuance of notice under Sections 73 or 74 of the Act, if the goods are found under valued, penalty can be imposed.

8. Accordingly, imposition of penalty under Section 129 of the Act on the speculation that the goods are under valued cannot be allowed.

9. In light of the above, impugned orders dated December 20, 2020 and September 17, 2021 are quashed and set-aside. Consequential reliefs to follow. In the event any deposit has been made by the petitioner to the authorities, the same shall be returned to the petitioner within four weeks from date."

10. In the present case, the respondent authority has failed to bring on record any material that the goods mentioned in the tax invoice accompanying with the goods, has different HSN Code and different rate of tax or mentioned in the detention memo dated 1.10.2019. Once this fact is not disputed that HSN Code and rate of tax is similar, no adverse inference can be drawn. The petitioner would not gain in not mentioning correct description of items or state would loose its legitimate tax.

11. Further, so far as the ground taken in respect of under valuation of the goods is concerned, the circular of the Commissioner, Commercial Tax, Uttar Pradesh dated May 9, 2018, covers the issue in favour of the petitioner.

12. In view of the aforesaid facts and circumstances of the case as well as law laid down by this Court, the impugned order dated 26.11.2020 cannot be sustained in the eyes of law and same is hereby quashed.

13. The writ petition succeeds and is allowed.

14. Any amount deposited by the petitioner in the present proceeding shall be refunded to the petitioner.

Order Date :- 19.11.2024