Scrutiny of GST Returns

As we know that the person who is registered under GST, has to file GST Returns. There are different types of GST returns like GSTR-1, GSTR-3B, GSTR-4, GSTR-5, GSTR-6, GSTR-7, GSTR-9 etc. depending upon the type of the taxpayer. After submission of GST returns by the taxpayer if the proper officer seems any inconsistencies or errors in the information declared in these returns, then the proper officers will conduct the scrutiny of these GST returns. In this article we will discuss about the scrutiny process and responsibility of the taxpayer to respond such scrutiny notice.

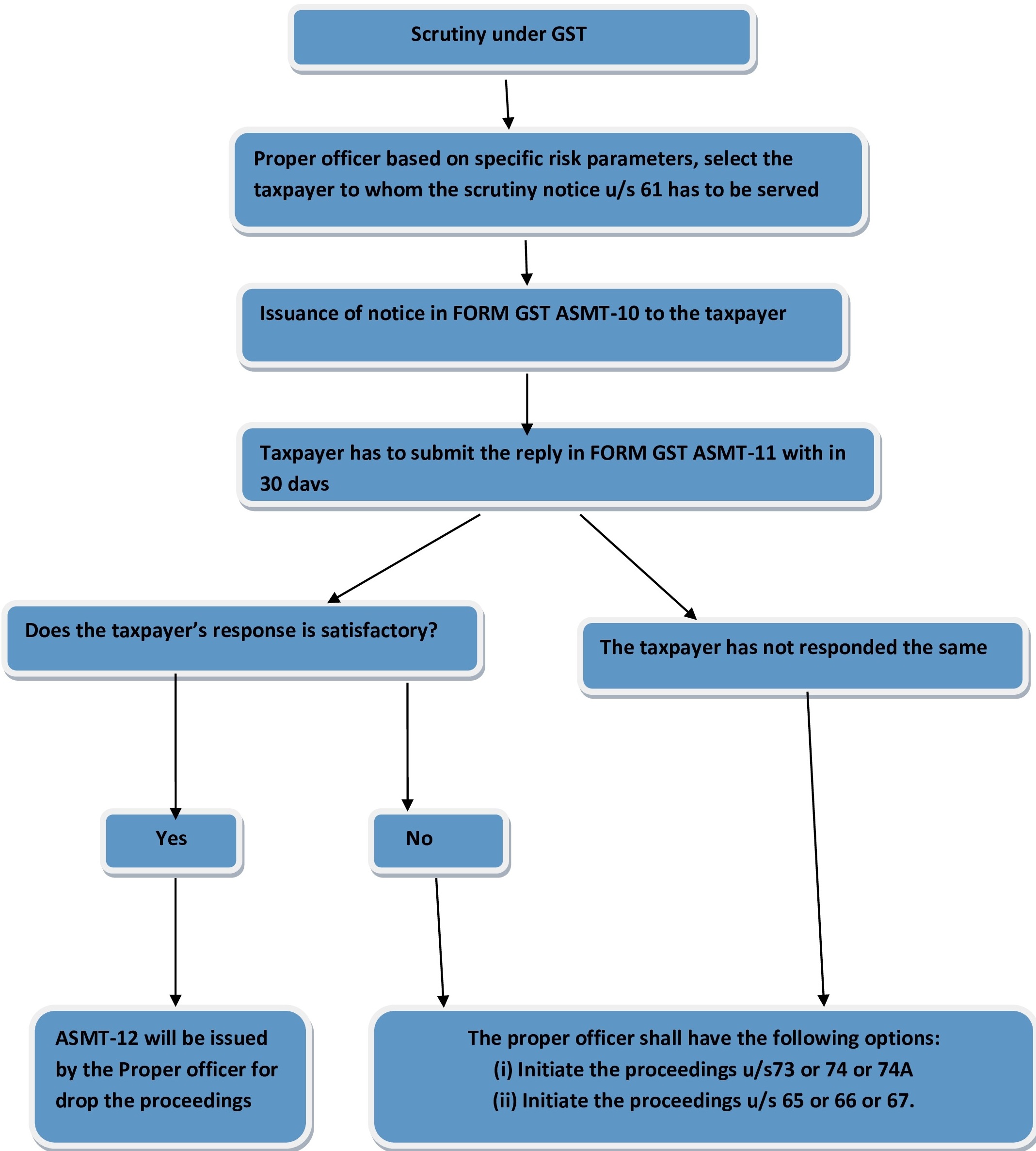

Section 61 of CGST Act 2017 contains the provisions related to the scrutiny of GST returns. As per section 61(1), the proper officer may scrutinize the return and related particulars furnished by the registered person to verify the correctness of the return and inform the taxpayer about such discrepancies noticed. Further, as per sub rule 1 of Rule 99 of CGST Rules 2017 in case of any discrepancy, the proper officer shall issue a notice to the said person in FORM GST ASMT-10, informing him of such discrepancy and seeking his explanation thereto within such time, not exceeding 30 days from the date of service of the notice or such further period as may be permitted by him and also, where possible, quantifying the amount of tax, interest and any other amount payable in relation to such discrepancy. Thus from the above provisions it is clear that if during the scrutiny of GST returns, the discrepancies are observed by the proper officer then he shall issue a notice in FORM GST ASMT-10 to the taxpayers for which the taxpayer has to submit the explanations within 30 days from the date of serving the notice. As per Rule 99(2) of CGST Rules 2017 the taxpayer has to submit his explanations in FORM GST ASMT-11 to the officer. Where the explanation furnished by the registered person is found to be acceptable, the proper officer shall inform him in FORM GST ASMT-12. The issuance of FORM GST ASMT-12 means the proceedings in respect of notice issued in FORM GST ASMT-10 has been concluded.

However, if the proper officer is

not satisfied with the explanations submitted by the taxpayer then in such

situation the proper officer has the following options available with him:

(i) To initiate the proceedings u/s

73 or

74 or

74A of CGST Act 2017 by issuing

a show cause notice to the taxpayer OR

(ii) To Recommend the case to initiate the proceedings u/s

65 or

66 or

67 of

CGST Act 2017.

Instructions for Scrutiny of

Returns:

To ensure uniformity in selection/ identification of returns for scrutiny,

methodology of scrutiny of such returns and other related procedures, the

following two instructions are issued by the board:

1.

Instruction No. 02/2022-GST:

Standard Operating Procedure (SOP) for Scrutiny of returns for FY 2017-18 and

2018-19, wherein various points have been covered like:

(i) How the returns to be selected for scrutiny.

(ii) Proper officer for scrutiny of returns.

(iii) Scrutiny Schedule.

(iv) Process of scrutiny by the Proper Officer.

(v) Timelines for scrutiny of returns.

(vi) Reporting and monitoring mechanism.

(viii) In addition to the above four annexures are given in the said

instruction, these are:

(a) Annexure-A – Scrutiny Schedule

(b) Annexure-B – Indicative list of parameters for scrutiny

(c) Annexure-C – Scrutiny register to be maintained by the proper officer

(d) Annexure-D – Monthly scrutiny progress report

2. Similarly the instruction no. 02/2023-GST was issued by the board for standard operating procedure for scrutiny of returns for FY 2019-20 onwards.

Steps to view notices on GST

portal:

Step 1: Login to the GST portal and go to the tab of “services” and select the

option of “user services” and then click on the tab “View Additional

Notices/Orders”.

Step 2: On clicking on “View Additional Notices”, the details of notices received

would be displayed.

Step 3: A taxpayer can view all the notices issued by the tax official by

clicking on ‘View’ option.

Consequences of not responding

to a Scrutiny Notice:

If the taxpayer does not respond to the scrutiny notice, then the tax officer

will take action under section 73 (non-fraudulent) and

74 (fraudulent). He can

issue a show-cause notice in FORM GST DRC-01 demanding the tax dues, together

with interest and penalty. The amount of penalty will vary depending upon the

grounds of the discrepancy found. Alternatively, the officer can recommend

audits under section

65,

66 or

67 of CGST Act 2017.

Conclusion: The entire process of scrutiny of returns can be understand with the help of following flow chart:

|

|

Disclaimer: The information given in this article is solely for purpose of understanding the law. It is completely based on the interpretation of the author and cannot be constituted as a legal advise, the author of this article and Lawcrux team is not responsible for any legal issues if arises on the basis of the interpretation given above.