Master the GST Refund Process: Secure What’s Rightfully Yours

Bonjour readers! Running a business comes with its fair share of challenges, and managing taxes is undoubtedly one of them. Imagine this: you’ve paid excess GST, and that money could be working for your business, yet it’s stuck in the system. The good news? GST refunds are designed to give you relief, ensuring your funds flow back to where they belong-your pocket.

Navigating the refund process may seem daunting at first, but with the right guidance, it can be a straightforward journey. From understanding the doctrine of “unjust enrichment” to knowing which forms to file and when, every detail matters. Refunds under GST not only ease financial burdens but also help maintain healthy working capital-something every thriving business needs.

This article is your go-to guide for decoding the GST refund process. So, let’s dive in, demystify the GST refund mechanism, and unlock the benefits that can keep your business growing stronger every day!

Who Can Claim a Refund and How?

Under Sub-section (1) of Section 54 of the CGST Act, 2017, read with Sub-rule (1) of Rule 89 of the CGST Rules, the following guidelines apply:

1. Eligible Persons

Any person (“claimant”) except those notified u/s 55 (e.g., UNO, Multilateral Financial Institution, Consulate or Embassies), can claim a refund for the following amounts:

Balance in the electronic cash ledger (as per Section 49(6)).

Tax, interest, penalty, fees, or other amounts paid.

Note: Refunds of IGST paid on goods exported out of India follow separate provisions (Rule 96 of the CGST Rules).

2. Application Process

Claimant shall file an application electronically in FORM GST RFD-01.

This application must be filed within two years from the relevant date.

3. Key considerations:

Refund claims are subject to the provisions of Rule 10B of the CGST Rules, 2017 (i.e. Aadhaar authentication).

Ensure proper documentation to avoid delays or rejections.

Understanding the Relevant Date

The "relevant date" is critical for determining the two-year limit for filing refund claims. Explanation (2) of Section 54 outlines how the relevant date varies depending on the type of claim:

|

Scenario |

Relevant date |

|

Goods Exported Out of India |

- By Sea or Air: Date when the ship or aircraft leaves India. - By land: Date when the goods pass the frontier. - By Post: Date of dispatch of goods by the concerned Post Office to a place outside India. |

|

Deemed Exports |

Date on which the return is filed related to such deemed export. |

|

Zero-Rated Supplies to SEZ developer/ Unit |

Due date of filing return u/s 39 (i.e. GSTR-3B) related to such supplies. |

|

Export of Services |

- Payment Received After Supply: Date of receipt of payment in convertible foreign exchange or INR (RBI-permitted). - Payment Received in Advance: Date of issuing the invoice. |

|

Refund Due to Judicial Orders |

Date of communication of such judgment, decree, order, or direction of the Appellate Authority, Tribunal, or any Court. Due date of filing return u/s 39 for the period in which the refund claim arises. |

|

Refund of Unutilized Input Tax Credit (ITC) - Inverted duty structure |

|

|

Provisional tax Payment |

Date of adjustment of tax after the final assessment. |

|

Person other than supplier |

Date of receipt of goods or services by such person. |

|

Any Other Case |

Date of payment of tax. |

Scenarios where refunds are available

Refund claims may arise in the following scenarios:

1. Deemed exports

2. Zero-rated supplies (Export of goods/services& Supplies to SEZ Developer/Unit) without payment of tax.

3. Zero-rated supplies with payment of tax.

4. Refund of accumulated input tax credit due to inverted duty structure.

5. Refund under section 77 of the CGST Act, 2017 (e.g., treating an intra-state supply as inter-state and vice versa).

6. Refund due to judicial orders (e.g., judgment, decree, order, or direction from appellate authority, tribunal, or any court).

7. Net refund of advance tax paid by casual taxable person or non-resident taxable person at the time of registration.

8. Refund of excess balance in the E-cash ledger.

9. Refund of taxes paid on purchases by UNO, Consulate or Embassy specified under section 55 of the CGST Act, 2017.

10. Refund of additional IGST paid due to upward revision in price of goods subsequent to exports.

11. Refund of tax paid on a supply not provided (either wholly or partially) and for which no invoice was issued ora refund voucher has been issued.

12. Finalization of provisional assessment.

13. Unregistered person who has borne the incidence of tax.

14. Excess tax payment or any other amount paid.

15. Refund on ‘any other ground’ using RFD-01

Scenarios Where Refunds Are Not Available

Refund claims will not be entertained in the following cases:

If the claim amount does not exceed Rs. 1,000.

No refund of unutilized ITC for zero-rated supplies made with tax payment.

Common Mistakes to Avoid

1. Incomplete Documentation: Ensure all required invoices, forms, and proofs are included.

2. Missed Deadlines: Track relevant dates carefully to avoid missing the two-year filing limit.

3. Incorrect Claim Categories: Ensure you apply for the correct type of refund (e.g., inverted duty structure vs. zero-rated supply).

Documentation Requirement for Refund Claims

Avoiding mistakes starts with understanding the specific documentation required for different scenarios. Proper documentation is the backbone of a successful refund claim under GST. Rule 89(2) of the CGST Rules prescribes the documentation required in different scenarios. Missing or inaccurate documents are among the top reasons for delays or rejections. Application in FORM GST RFD-01 shall be accompanied by the following information, documents &evidences, and certificate in Annexure 1 & 2 of the form to establish that the refund is actually due to the applicant.

Let’s outline the key documents needed to ensure a smooth refund process in different scenarios:

|

Scenario |

Information/ Documents required |

|

(a) If refund becomes due as a result of an Order passed by the proper officer or an Appellate Authority or Appellate Tribunal or any court |

i) The reference number of the order and a copy of the order, OR ii) Reference number of the payment of the amount i.e. pre-deposit as specified in section 107(6) and section 112(8) claimed as refund. |

|

(b) Refund on account of export of goods (without payment of tax) other than electricity. |

Information required to be furnished in Statement-3 attached in Annexure-1 of FORM GST RFD-01: ➣ number and date of shipping bills or bills of export, and ➣ number and the date of the relevant export invoices |

|

(ba) Refund on account of export of electricity (without payment of tax) |

Information required to be furnished in Statement-3B attached in Annexure-1 of FORM GST RFD-01: ➣ number and date of the export invoices, ➣ details of energy exported, ➣ tariff per unit for export of electricity as per agreement Documents required to be attached: ➣ copy of statement of scheduled energy for exported electricity by Regional Energy Account. ➣ copy of agreement detailing the tariff per unit. |

|

(bb) & (bc) Refund on account of upward revision in price of such goods subsequent to exports |

Information required to be furnished in Statement-9A & 9B attached in Annexure-1 of FORM GST RFD-01: ➣ number and date of export invoices ➣ number and date of shipping bills or bills of export ➣ number and date of Bank Realisation Certificate (BRC) or foreign inward remittance certificate (FIRC) issued by Authorised Dealer-I Bank in respect of such shipping bills or bills of export ➣ the details of refund already sanctioned under sub-rule (3) of rule 96 of the CGST Rules. ➣ the number and date of relevant supplementary invoices or debit notes issued subsequent to the upward revision in prices. ➣ details of payment of additional amount of IGST, in respect of which such refund is claimed. ➣ number and date of FIRC issued by AD-I Bank in respect of additional foreign exchange remittance received. Documents required to be attached: ➣ Copies of the export invoices. ➣ Copies of the shipping bills or bills of export. ➣ Copies of BRC or FIRC related to the shipping bills or bills of exports issued by Authorized Dealer-I Bank. ➣ Copies of relevant supplementary invoices or debit notes or credit notes issued due to price revisions. ➣ Proof of payment of the additional IGST including any interest paid. ➣ Copies of FIRC issued for additional foreign exchange received due to price revisions. ➣ Certificate issued by a practicing CA/ CMA to the effect that the said additional foreign exchange remittance is on account of such upward revision in price of the goods subsequent to exports ➣ Copy of contract or other documents, indicating requirement for the revision in price of exported goods and the price revision thereof. ➣ A reconciliation statement, reconciling the value of supplies declared in supplementary invoices/ debit notes/ credit notes issued along with relevant details of BRC or FIRC issued by AD-I Bank. |

|

(c) Refund on account of the export of services; |

Information required to be furnished in Statement-2 ( Export of services with payment of tax) or Statement-3 (Export without payment of tax (accumulated ITC)), as the case may be, attached in Annexure-1 of FORM GST RFD-01 ➣ number and date of invoices and the relevant BRC or FIRC |

|

(d) & (f) Supply of goods made to a Special Economic Zone unit or a Special Economic Zone developer |

Information required to be furnished in Statement-4 (On account of supplies made to SEZ unit or SEZ Developer (on payment of tax)) or Statement-5 (On account of supplies made to SEZ unit or SEZ Developer (without payment of tax)), as the case may be, attached in Annexure-1 of FORM GST RFD-01: ➣ number and date of invoices Documents required to be attached: ➣ Invoices that carrying an endorsement as specified under 2nd Proviso to Rule 46. ➣ declaration to the effect that tax has not been collected from the SEZ unit or the developer |

|

(e) & (f) Supply of services made to a Special Economic Zone unit or a Special Economic Zone developer; |

Information required to be furnished in Statement-4 ( On account of supplies made to SEZ unit or SEZ Developer (on payment of tax)) or 5 (On account of supplies made to SEZ unit or SEZ Developer (without payment of tax)), as the case may be, attached in Annexure-1 of FORM GST RFD-01: ➣ number and date of invoices Documents required to be attached: ➣ Invoices that carrying an endorsement as specified under 2nd Proviso to Rule 46. ➣ A declaration to the effect that tax has not been collected from the SEZ unit or the developer, the format of which is attached in FORM GST RFD-01. |

|

(g) Deemed exports |

Information required to be furnished in Statement-5B depending upon the refund type i.e., on account of deemed exports claimed by supplier or on account of deemed exports claimed by recipient, as the case may be, attached in Annexure-1 of FORM GST RFD-01: ➣ number and date of invoices Documents required to be attached: ➣ Such evidences notified in this behalf ➣ A declaration to be submitted by the recipient or the supplier, as the case may be, the format of which is attached in FORM GST RFD-01. |

|

(h) Refund of any unutilized ITC on account of inverted duty structure (where the credit has accumulated on account of the rate of tax on the inputs being higher than the rate of tax on output supplies, other than nil-rated or fully exempt supplies) |

Information required to be furnished in Statement-1A attached in Annexure-1 of FORM GST RFD-01: ➣ number and the date of the invoices received and issued during a tax period to which such claim pertains. |

|

(i) Refund arises on account of the finalization of provisional assessment |

➣ reference number of the final assessment order. ➣ copy of the said order |

|

(j) Refund u/s 77 (where transaction considered as intra-state supply but subsequently held to be inter-state supply or vice versa) |

Information required to be furnished in Statement-6 attached in Annexure-1 of FORM GST RFD-01: ➣ statement showing the details of transactions |

|

(k) Excess payment of tax & interest, if any, or any other amount paid |

Information required to be furnished in Statement-7 attached in Annexure-1 of FORM GST RFD-01: ➣ details of the amount of claim |

|

(ka) & (kb) refund claimed by an unregistered person where the agreement or contract for supply of service has been cancelled or terminated |

Information required to be furnished in Statement-8 attached in Annexure-1 of FORM GST RFD-01: ➣ details of invoices viz. number, date, value, tax paid and details of payment ➣ details of payment received from the supplier against cancellation or termination of such agreement Documents required to be attached: ➣ copy of the invoices ➣ proof of making the payment to the supplier ➣ copy of agreement or registered agreement or contract, as applicable, entered with the supplier for supply of service, ➣ the letter issued by the supplier for cancellation or termination of agreement or contract for supply of service ➣ Proof that payment has been received from the supplier on cancellation or termination of agreement/ contract ➣ A Certificate issued by the supplier to the effect that:

|

Before we proceed with the detailed procedure for refund claims under the GST Act, we will first discuss the key concept of the doctrine of unjust enrichment, which plays a crucial role in determining whether the refund amount will be credited to the claimant's bank account or transferred to the Consumer Welfare Fund u/s 57. Let's explore this concept in detail.

What is the Doctrine of Unjust Enrichment?

“Unjust enrichment” refers to a situation where a person wrongfully retains money or benefits that rightfully belong to someone else, violating principles of justice, fairness, and good conscience. This concept ensures that no individual can gain an unfair advantage at the expense of other due to errors or misjudgments. In other words, it prevents someone from benefiting inappropriately from a situation.

The principle of unjust enrichment is embedded in the GST framework to prevent taxpayers from making unwarranted claims for refunds. While the term “unjust enrichment” is not explicitly mentioned in the CGST Act, it is implied in sections 54(5) and 54(8) of the CGST Act. Refunds are granted only if the claimant proves that the tax burden has not been passed on to others, given that GST is an indirect tax. Therefore, every refund claim (except in specified cases) must meet the unjust enrichment test.

➣ Exceptions to the Unjust Enrichment Test

As per Section 54(8) of the CGST Act, the unjust enrichment test is not required in the following cases:

(a) refund of tax paid on export of goods or services or both or on inputs or input services used in making such exports.

(b) refund of unutilised input tax credit u/s 54(3) i.e., on account of:

accumulated ITC due to inverted duty structure.

zero rated supplies made without payment of tax

(c) refund of tax paid on a supply which is not provided, either wholly or partially, and for which invoice has not been issued, or where a refund voucher has been issued

(d) refund of tax in pursuance of section 77 of the CGST Act.

(e) the tax or interest, if any borne, or any other amount paid by the applicant, if he had not passed on the incidence of such tax and interest to any other person, or

(f) the tax or interest borne by such other class of applicants as notified.

In all other cases, the unjust enrichment test must be satisfied before processing the refund.

➣ Declaration or Certificate for Refund Claims

To comply with the unjust enrichment principle, refund applicants must submit the following documents as per Section 54(4) of the CGST Act and Rules 89(2)(l) and 89(2)(m) of the CGST Rules, 2017:

Refund Amount ≤ Rs. 2 Lakhs:

A self-declaration by the claimant stating that the incidence of tax, interest, or any other amount claimed as a refund has not been passed on to another person.

Refund Amount > Rs. 2 Lakhs:

A Certificate issued by a Chartered Accountant (CA) or Cost and Management Accountant (CMA) in Annexure 2 of FORM GST RFD-01, certifying that the incidence of tax, interest, or other amounts claimed as refund has not been passed on to another person.

➣ Consumer Welfare Fund

As per Section 57 of the CGST Act, if the refund claim does not pass the test of unjust enrichment, the concerned refund amount is credited to the Consumer Welfare Fund instead of being paid to the applicant.

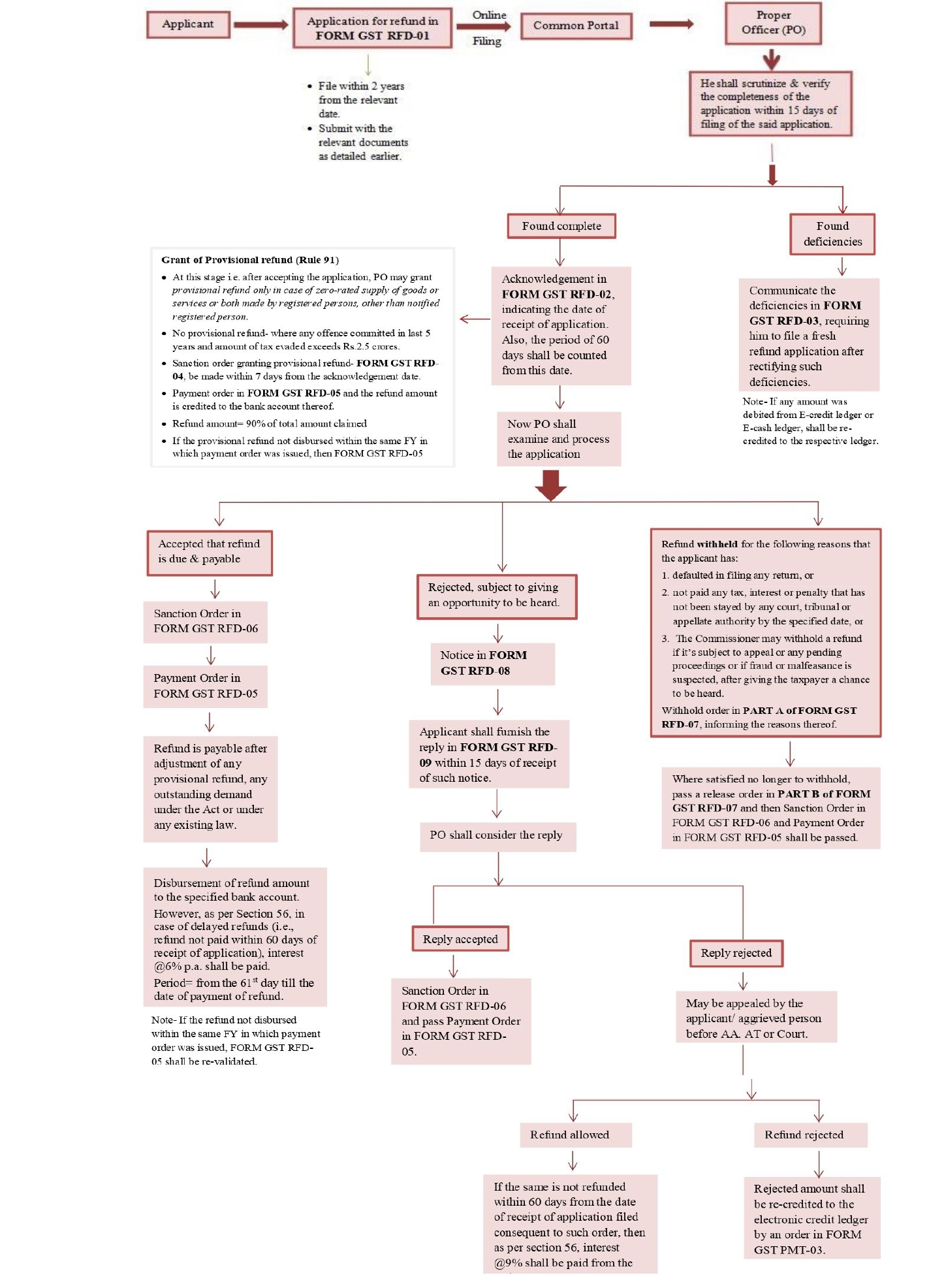

Refund Procedure: From Application to Final Credit

Next, we will outline the procedure from application submission to the final crediting of funds into the applicant's bank account, governed by the provisions of Sections 54 and 56 of the CGST Act and Rule 90, 91 to 94 of the CGST Rules, as illustrated in the following diagram.

Before reviewing the diagram, here are some key points to remember:

1. The refund process must be completed within 60 days of application filing, as indicated in the acknowledgment (FORM GST RFD-02).2. Upon filing a refund application related to ITC, the E-credit ledger will be debited by the corresponding amount.

3. Per Rule 90(5) & (6), the applicant may withdraw the refund application before the issuance of any refund-related order or notice by filing FORM GST RFD-01W. Any amount debited from the electronic credit or cash ledger will then be re-credited to the respective ledger.

|

|

Miscellaneous cases:

|

Scenario |

Application Form |

Max. time limit for filing application and relevant date |

Doctrine of Unjust Enrichment |

Amount of refund |

Documents & conditions |

|

Person holding UIN i.e., UNO, Consulate or Embassy (Section 55 & Rule 95) |

|

Within 2 years from the last day of quarter in which supply was received. |

NA |

Tax paid on inward supplies |

Statement of the inward supplies of goods or services or both in FORM GSTR-11. Conditions: ➣ Inward supplies were received from a registered person against a tax invoice. ➣ name and GSTIN or UIN of the applicant is mentioned in the tax invoice. ➣ Other specified conditions/ restrictions. If UIN of applicant is not mentioned in tax invoice, then copy of the invoice, duly attested by the authorized representative of the applicant. |

|

Refund to CTP or NRTP |

2 years from the relevant date Relevant date = refund, only after filing all returns pertaining to the period for which registration certificate is held. |

NA |

Advance paid (-) tax due |

Final return by CTP/ NRTP |

Key Legal Perspectives

This section provides an overview of key judicial insights regarding the GST refund filing process, highlighted below:

In Lenovo India Pvt. Ltd. vs. The Joint Commissioner of GST (Appeals-I) [2023(11)LCX0162], writ petitions were filed against certain orders rejecting refund claims for IGST paid on goods supplied to Special Economic Zone units. The rejection was partly due to the absence of supporting documentation at the time of filing the applications, although it was later submitted during the reply/personal hearing, which was deemed barred by the limitation period. The Madras High Court referred to Section 54(1) of the CGST Act, which clearly shows that the assessee can file an application within two years. The wording in the section, 'may make application before two years from the relevant date in such form and manner as prescribed,' implies that while the application may be filed within two years, it is not mandatory. In certain cases, a refund application can be submitted beyond the two-year period. The time limit under Section 54(1) is directory in nature and not obligatory. As such, even if an application is submitted after two years, the legitimate claim for refund by the assessee should not be denied in appropriate cases.

In Raghav Ventures v. Commissioner of Delhi Goods & Service Tax [2024(03)LCX0001], the Delhi High Court held that interest under Section 56 of the Act becomes payable if the refund is not processed within 60 days from the date of receipt of the application. The payment of interest is statutory and is automatically due without the need for a claim if the refund is delayed beyond 60 days. The interest cannot be denied even if the petitioner has not claimed it in FORM GST-RFD-01. The issue of interest arises only if the refund is not granted within the stipulated 60-day period, and the respondent must justify any delay. In this context, even if the petitioner has not specifically requested interest, the claim for interest cannot be denied, as it is mandatory under Section 56 of the Act. In light of this, the petitioner is entitled to statutory interest at the rate of 6%, starting from the day after the 60-day period until the refund is credited to the petitioner's bank account.

In Jian International v. Commissioner of Delhi Goods and Service Tax [2020(07)LCX0036],the Delhi High Court held that the petitioner’s refund application, filed on 4th November 2019, had not been processed within the statutory timelines. As no acknowledgment (FORM GST RFD-02) or deficiency memo (FORM GST RFD-03) was issued within the prescribed 15-day period, the application was deemed complete as per Rule 89 of the CGST/DGST Rules. The Court emphasized that allowing the respondent to issue a deficiency memo at this stage would effectively extend the refund process beyond the statutory time limits, impeding the petitioner’s right to claim interest. The respondent’s argument for a deficiency memo was rejected as it was seen as a hyper-technical plea, given that all relevant documents were provided. The Court thus ordered the respondent to pay the refund along with interest within two weeks.

In RK InfracorpPvt Ltd [2022(09)LCX0025], the Andhra Pradesh High Court, while hearing a petition challenging the GST department’s refusal to release an already sanctioned refund due to technical issues on the GST portal, directed the department to reconsider the refund claim. If the assessee is deemed eligible, the Court ordered the refund to be processed along with the applicable interest.

In Chromotolab And Biotech Solutions vs. Union Of India [2022(10)LCX0075], the assessee submitted a GST refund application under section 54 of the CGST Act, 2017, via the common portal on 28 December 2018. However, the physical submission of the application, along with the supporting documents, was made on 17 October 2019. The refund application was rejected on the grounds that it was filed after the two-year limitation period, considering the date of physical submission as the filing date.

The assessee challenged the rejection by filing a writ petition. The High Court observed that the application was filed on the common portal on 28 December 2018, and an ARN (Application Reference Number) was generated. The court noted that the Revenue had not taken any action on the application until the physical submission of documents. Since the application was filed in accordance with the prescribed process, the High Court ruled that the date of filing the application on the common portal should be considered the date of filing the refund claim, in compliance with Section 54 of the CGST Act and Rule 89 of the CGST Rules. The High Court ruled that the date the petitioner filed the application on the common portal should be treated as the official filing date for the refund claim, meeting the requirements of Section 54 of the CGST Act and Rule 89 of the CGST Rules. The court further clarified that the procedure evolved in Circular dated 15.11.2017 cannot operate as delimiting condition on the applicability of statutory provisions.

In Indian Oil Corporation Ltd. v. Commissioner of Central Goods & Services Tax [2023(12)LCX0073],the Petitioner, involved in bottling and distributing LPG for both domestic and industrial use, sought refunds for accumulated ITC from various tax periods. The bulk LPG, used as the principal input, and the bottled LPG supplied by the Petitioner are subject to GST at a rate of 5%. Despite acknowledging the refund applications, the Revenue Department did not process them and later rejected the claims, citing that both bulk and bottled LPG are the same product, taxed at the same rate, and invoking Clause (ii) of the proviso to Section 54(3) of the CGST Act.

The Hon'ble Delhi High Court ruled that the Petitioner’s claim for refund could not be denied based on Circular No. 135/05/2020-GST dated March 31, 2020, issued by the CBIC under Section 168(1) of the CGST Act. The Circular stated that refunds of accumulated ITC were not available when input and output supplies were the same. However, in this case, the Petitioner argued that although the tax rates on the principal input supply and output supply were the same, the tax rates on other input supplies differed. The Court directed the Revenue Department to process the refund application, along with the applicable interest, within six weeks from the date of the order. Consequently, the petition was allowed, and all pending applications were disposed of.

Conclusion

Mastering the GST refund process is essential for businesses seeking to manage their cash flow efficiently and ensure that excess tax payments don’t remain trapped in the system. By understanding the key steps-from eligibility criteria and proper filing procedures to the concept of unjust enrichment-businesses can navigate the complexities of the refund mechanism with confidence. Timely application submission, proper documentation, and adherence to the relevant rules are crucial to securing a smooth refund process.

Judicial rulings and government efforts have contributed to making the GST refund process more efficient. However, there's still a need for further simplification and measures that are more taxpayer-friendly. A well-functioning refund mechanism is essential not only for improving business operations and preventing capital blockage but also for creating a more favorable environment for economic growth in India. For this to happen, both taxpayers and tax authorities must work together to streamline procedures, increase transparency, and guarantee timely refunds.

With clear legal backing and the right knowledge, businesses can confidently navigate the GST refund process, ensuring they claim what’s rightfully theirs without unnecessary hurdles.

Refund in Case of Zero-Rated Supplies without payment of tax under bond or letter of undertaking and Inverted Duty Structure

Rule 89(4), (4A), and (5) pertain to refunds in the case of zero-rated supply of goods or services (or both) without payment of tax under a bond or letter of undertaking (LUT) and refunds on account of an inverted duty structure. These topics will be explained in detail in a separate article.

Disclaimer: The information given in this article is solely for purpose of understanding the law. It is completely based on the interpretation of the author and cannot be constituted as a legal advise, the author of this article and Lawcrux team is not responsible for any legal issues if arises on the basis of the interpretation given above.