GST Dues Recovery Under Section 79 - The Countdown Starts Now

Introduction: The Clock Starts Ticking After a Demand Order

Receiving a GST demand order isn’t the end of the road-it’s the beginning of a countdown. Under the CGST Act, taxpayers are given three months from the date of service of such an order to clear their dues. But if you think the department waits passively during this time, think again.

Sections 78 and 79 of the CGST Act, along with a suite of procedural rules, arm tax officers with a range of recovery mechanisms-ranging from deduction from government payments to full-blown auctions of your property. This article walks you through these provisions and explains how each recovery method works in practice.

It All Starts Here: Section 78 – When Recovery Gets Triggered

You may think you have some breathing room after a tax order is issued-but Section 78 of the CGST Act sets the clock ticking.

According to this provision:

“Any amount payable by a taxable person in pursuance of an order under GST law must be paid within 3 months from the date of service of that order.”

And here’s the kicker:

If you don’t pay within 3 months, the department is empowered to initiate recovery proceedings-no further reminders required.

But wait-there’s a proviso too. If the proper officer believes it’s in the interest of revenue, they can ask you to pay even before the 3 months are over, provided they record their reasons in writing.

☠ So, if you receive a demand order, the recovery engine is already revving in the background.

What Happens Next? Section 79 Kicks In

Once the recovery process is triggered under Section 78, Section 79 of the CGST Act takes over, laying down the actual methods of recovery. And they aren’t subtle. Here’s how the department can collect the dues:

But before diving into the specific tools, it’s important to understand a new procedural layer that connects the dots between default and recovery-Rule 142B.

Rule 142B: The Department’s First Strike-DRC-01D Intimation Before Recovery

Inserted via Notification No. 38/2023–Central Tax, dated 04.08.2023, Rule 142B adds a fresh weapon to the department’s recovery arsenal. It creates a formal intimation mechanism before any recovery action is taken under Section 79.

Here's how it works:

When any tax or interest becomes recoverable under Section 79, whether under Section 75 read with Rule 88C (difference in tax liability and outward supply as per GSTR-1 and 3B) or otherwise, and remains unpaid, the proper officer shall issue an intimation in Form GST DRC-01D electronically on the portal.

The intimation directs the defaulting taxpayer to pay the specified amount within 7 days of the notice.

This amount is then posted in Part-II of the Electronic Liability Register in Form GST PMT-01.

Most critically, this intimation itself is treated as the recovery notice, eliminating the need for a separate notice before action.

If the dues remain unpaid after 7 days, the officer is empowered to initiate recovery under any of the rules available-Rule 143 to Rule 147, Rule 155, Rule 156, Rule 157, or Rule 160.

Why it

matters:

Rule 142B ensures quick and procedural escalation of unpaid

tax/interest-especially in automated or data mismatch cases-without waiting for

lengthy adjudication or reminders. It shortens the window between detection and

action.

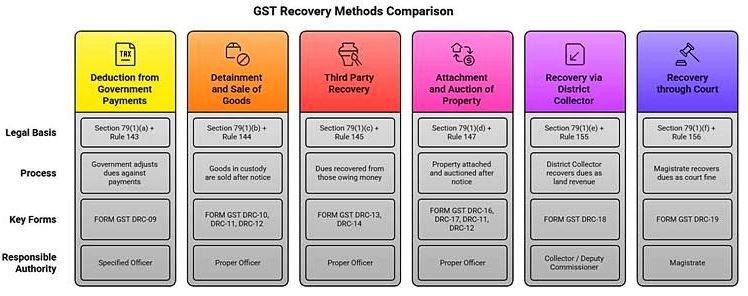

💣6 Strong Recovery Tools Under GST

Once Section 79 kicks in, these are the go-to recovery weapons in the department’s arsenal:

1. Deduction from Government Payments

If you are owed money by the government (e.g., contractor bills), the department can adjust your dues against those payments.

If any amount is unpaid by the defaulter, the proper officer issues FORM GST DRC-09 to the specified officer.

That officer is directed to deduct your GST dues from amounts payable to you.

The "specified officer" is broadly defined to include officers of:

Central Government

State Governments

Union Territories

Local Authorities

Government-owned or controlled Boards, Corporations, or Companies

This method ensures that if you are due to receive funds from any government entity (say, as a contractor or vendor), your GST dues can be adjusted at source even without your consent.

2. Detainment and Sale of Goods

[Section 79(1)(b) + Rule 144 & Rule 144A]

If your goods are in government custody, they can be detained and sold to recover dues.

Officer → prepares Inventory + estimates market value

Sell only what's needed (dues + recovery costs).

Sale notice is issued in FORM GST DRC-10 (unless perishables/hazardous-then immediate sale).

You have 15 days to pay and stop the sale.

If unpaid, auction/e-auction proceeds.

Successful bidder receives FORM GST DRC-11, must pay within 15 days.

On payment, officer issues FORM GST DRC-12 (ownership transfer).

Re-auction if there are no/low bids.

Rule 144A kicks in when goods or the vehicle are detained/seized during transit under Section 129, and the penalty is not paid within 15 days of the order passed under Section 129(3), then the officer proceeds to sell/dispose the goods or conveyance so detained or seized.

This rule deals specifically with the recovery of penalty under Section 129 (for goods or conveyance detained or seized in transit), follows the same procedure as laid down in Rule 144. The only additional provision is:

“If the detained or seized goods are perishable, hazardous, or likely to depreciate in value over time, the proper officer may reduce the 15-day period for payment or auction, to safeguard revenue.”

3. Third Party Recovery

Department can recover dues from someone who owes you money or holds funds on your behalf.

PO issues notice in FORM GST DRC-13 to third party (‘they/them”) owing/holding money for you.

Requires them to pay Govt. instead of you, to the extent of your liability

They must comply - no need to produce documents

If they fail → they become defaulter

Officer can amend/revoke/extend notice anytime

Payment = good discharge of liability to you → FORM GST DRC-14 issued to them

If they make payment to you after notice = they become personally liable to Govt.

If they prove no money is/was due → not liable

4. Attachment and Auction of Property

Your movable or immovable property can be attached and auctioned if dues remain unpaid.

Officer may distrain/attach defaulter’s property (movable or immovable)

Property detained until dues (incl. costs) are paid

If unpaid after 30 days, property sold to recover dues

Officer prepares property list& estimates market value

Issues Order of attachment or distraint & sale notice in FORM GST DRC-16

Notice prohibits any transaction involving the attached property

Copy sent to relevant authorities to create encumbrance; removed only on officer's written instruction

For immovable property: attachment notice affixed on site until sale is confirmed

For movable property: officer seizes goods as per Chapter XIV; keeps in custody himself or authorises another officer

Auction process initiated (incl. e-auction) – notice in FORM GST DRC-17 – Includes property details and purpose of sale

If property is a negotiable instrument/share– sold via broker (not public auction)

Officer may demand pre-bid deposit from bidders; forfeited if highest bidder fails to pay

Minimum 15 days gap between auction notice and auction date; for perishable/hazardous goods, officer may sell immediately.

Claims/objections to attachment allowed

- Officer investigates; sale may be postponed

- Claimant must prove possession or legal interest on date of attachment

If satisfied property not owned by defaulter or held in trust, officer releases it (fully or partially)

If satisfied property belongs to defaulter or held for him, officer rejects claim and proceeds with sale

Successful bidder gets FORM GST DRC-11 (payment notice)

- Must pay within 15 days

- On payment, officer issues ownership certificate in FORM GST DRC-12

- Title transfers to bidder from date of certificate

If highest bid made by multiple persons and one is a co-owner, co-owner is preferred

Bidder pays stamp duty, taxes, fees on transfer

If defaulter pays before auction notice, auction canceled

If no/low bids, or poor participation - re-auction initiated

Note: Other Relevant Rules

Rule 148 – No officer or person involved in the sale process can directly or indirectly bid for or acquire interest in the property.

Rule 149 – No sale on Sundays, govt. holidays, or notified local holidays.

5. Recovery via District Collector

The officer can issue a certificate to the District Collector, who will recover your dues like land revenue arrears.

Proper officer prepares signed certificate in FORM GST DRC-18 specifying dues

Sends to Collector /Deputy Commissioner / authorised officer

Recovery treated as arrears of land revenue

Action taken in district where defaulter:

Owns property, or

Resides, or

Carries on business

6. Recovery through Court

GST dues can even be collected like a court-imposed fine, with a Magistrate’s help.

Proper officer files application in FORM GST DRC-19 before the appropriate Magistrate

Magistrate recovers amount as if it were a fine imposed by the court

Proceedings are not bound by CrPC restrictions.

Where Do the Sale Proceeds Go?

[Applicable to Rule 144, Rule 144A & Rule 147 | As per Rule 154]

Whether the recovery is done by selling detained goods in transit (under Rule 144A), goods in custody (under Rule 144), or attached property (under Rule 147), the disposal of sale proceeds is governed by Rule 154.

Here’s how the amount recovered is appropriated:

1. Administrative Costs First

The first cut goes towards the administrative expenses of conducting the recovery and sale.

2. Then Toward Tax or Penalty

Next, the amount is adjusted against:

The recoverable tax/dues, or

The penalty u/s 129(3) (in transit seizure cases).

3. Then Any Other Dues

Any remaining balance is used to offset other liabilities under CGST, IGST, SGST/UTGST laws and rules.

4. Surplus? It’s Returned

If the owner is registered, the excess is credited to their electronic cash ledger.

If unregistered, it goes to their bank account.

But if the amount cannot be returned within 6 months (or within any extended time allowed), the balance must be transferred to the Consumer Welfare Fund.

This rule ensures sale proceeds are properly appropriated and any surplus is rightfully returned-reinforcing a fair and transparent recovery mechanism.

Miscellaneous Recovery Rules

In addition to the standard recovery procedures, there are specific provisions under the GST framework that address unique recovery situations.

Rule 146: Recovery through Execution of a Decree, etc.

Amount payable to defaulter under civil court decree (payment or sale for mortgage/charge)

Proper officer sends request in FORM GST DRC-15 to court

Court executes decree per Code of Civil Procedure, 1908 (5 of 1908)

Net proceeds credited towards GST recovery

Rule 157: Recovery from Surety

Any person becoming Surety for defaulter’s dues

treated as defaulter for recovery proceedings

Rule 160: Recovery from Company in Liquidation

Company under liquidation as per Section 88

Commissioner notifies liquidator via FORM GST DRC-24

Recovery of tax, interest, penalty, or other dues.

Conclusion: When the Department Knocks, Be Prepared

The recovery machinery under GST is anything but passive. Once a demand order is served, the law sets a precise timeline-and empowers tax authorities to act swiftly and decisively. From slicing your dues out of government payments to attaching your property or involving the Magistrate, the recovery mechanisms under Sections 78 and 79 are varied, far-reaching, and rigorously codified.

For taxpayers, the key takeaway is this: don't wait for reminders. The moment a demand is raised, the countdown begins. Whether it's responding to a DRC-10 or challenging an attachment in DRC-16, timely action can protect your assets and reduce the damage. Understanding how each tool works isn’t just academic-it’s your first line of defense.

In the world of GST, compliance delays come at a steep cost. Stay alert, stay proactive.

Note- The provisions covered under Section 79 set the stage for the recovery process, but GST recovery is a multi-step journey with many layers. In our next article, we will delve deeper into the subsequent recovery mechanisms - including installment payments, attachment of property, provisional attachments, and enforcement procedures that follow if dues remain unpaid. Stay tuned to understand the full scope of how GST dues are recovered and how you can best navigate these processes.

Disclaimer: The information given in this article is solely for purpose of understanding the law. It is completely based on the interpretation of the author and cannot be constituted as a legal advise, the author of this article and Lawcrux team is not responsible for any legal issues if arises on the basis of the interpretation given above.