GST Implications on RWA

A Resident Welfare Association (RWA), is a non-governmental organization (NGO) formed by residents of a specific locality or housing society to represent their interests and manage community welfare, such as maintenance, security, and social issues. Resident Welfare Associations (RWAs) are organizations that provide maintenance and upkeep for societies, apartment complexes, and residential colonies in India. The Resident Welfare Association (RWA) provides various services, such as security, maintenance of common areas, facilities, etc., to their members. The question that usually arises here is whether GST is applicable to these services provided by an RWA to its members? In this article we will discuss the GST implications on the services provided by RWA to its members.

Registration requirements & Exemptions available for RWA:

If the turnover of a housing society is above 20 lakhs, it needs to take

registration under GST in terms of

Section 22 of the CGST Act, 2017. However,

taking registration does not mean that the housing society has to compulsorily

charge GST in the monthly maintenance bills raised on its members. In respect of

RWA there is exemption provided under serial number 77 of

Notification No.

12/2017 CT(R) which states that service provided by an unincorporated body or a

non- profit entity registered under any law, to its own members by way of

reimbursement of charges or share of contribution

(a) as a trade union;

(b) for the provision of carrying out any activity which is exempt from the levy of GST or

(c) up to an amount of seven thousand five hundred rupees per month per member for sourcing of goods or services from a third person for the common use of its members in a housing society or a residential complex.

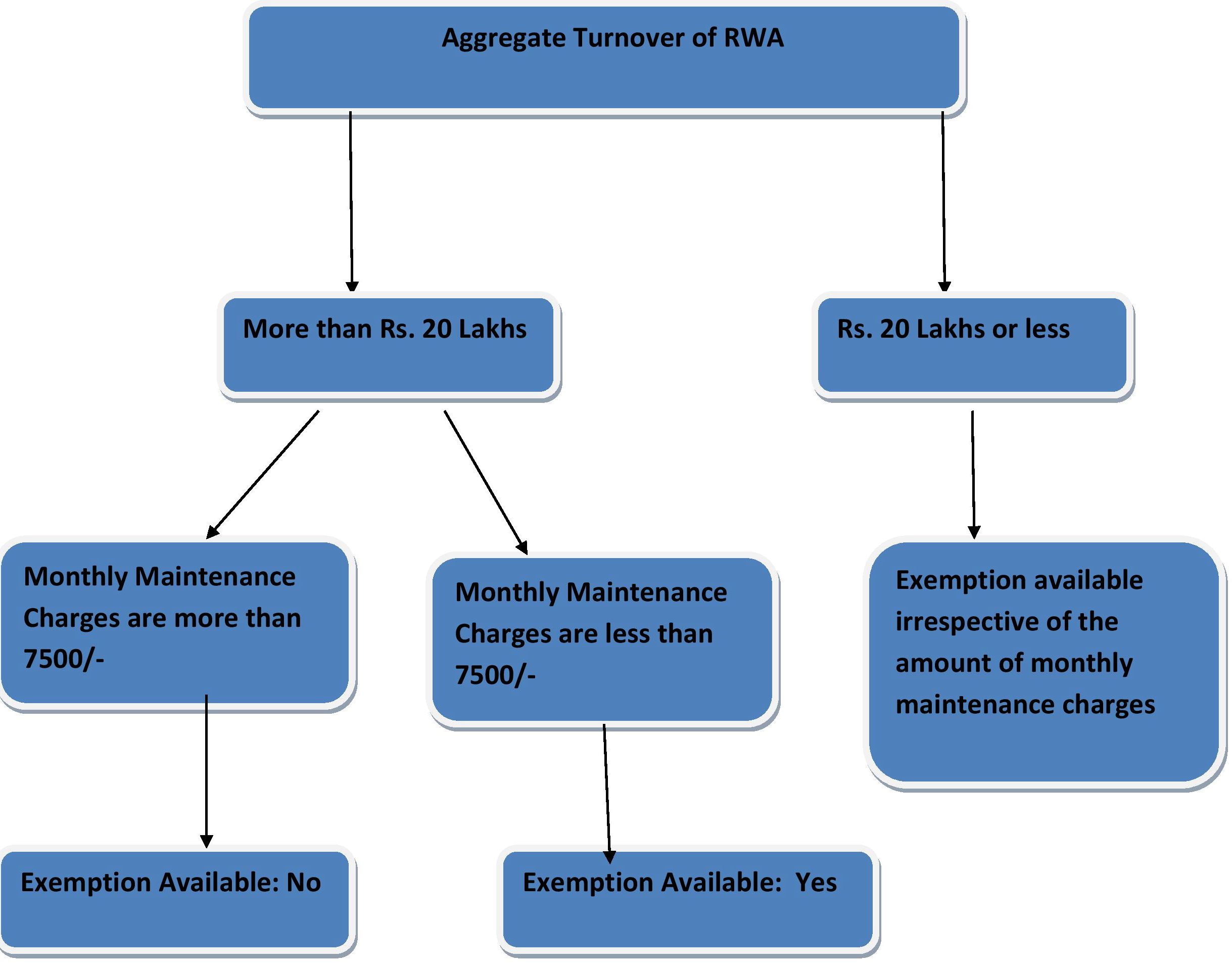

In view of the provision contained at (c) above, a society may be registered under GST, however if the monthly contribution received from members is less than Rs. 7,500/ - , no GST is to be charged by the housing society on the monthly bill raised by the society. However, GST would be applicable if the monthly contribution exceeds Rs. 7,500/ -.

On other hand it may be a situation that RWA has aggregate turnover less than Rs.20 lakh but the amount recovered from the members as monthly contribution is more than Rs. 7500/- per month per member, then in such situation no GST would be applicable even though the amount is more than 7500/-. The same was also clarified by CBIC vide serial number 2 of Circular No.109/28/2019 that if aggregate turnover of an RWA does not exceed Rs.20 Lakh in a financial year, it shall not be required to take registration and pay GST even if the amount of maintenance charges exceeds Rs. 7500/- per month per member. RWA shall be required to pay GST on monthly subscription/ contribution charged from its members, only if such subscription is more than Rs. 7500/- per month per member and the annual aggregate turnover of RWA by way of supplying of services and goods is also Rs. 20 lakhs or more.

Let us summarise the same with help of following diagram:

Further as per Section 23 (1) of the CGST Act, 2017, the following persons shall not be liable for registration, namely:-

(a) any person engaged exclusively in the business of supplying goods or services or both that are not liable to tax or wholly exempt from tax under this Act or under the IGST Act;

(b) an agriculturist, to the extent of supply of produce out of cultivation of land.

Thus, if the turnover of the society is less than Rs.20 Lakhs or even if the turnover is beyond Rs. 20 lakhs but the monthly contribution of individual members towards maintenance is less than Rs. 7,500/- (such services being exempt) and the society is providing no other taxable service to its members or outsiders, then the society (essentially Exclusively providing wholly exempt services) need not take registration under GST.

In this respect the another question that commonly arises is that if the monthly bill is say Rs. 9,000/- (and the same is on account of services for common use of its members), will GST be applicable on Rs. 9,000/- or Rs. 1,500/- which is in excess of Rs. 7500/-. In such cases, exemption is available up to an amount of Rs. 7,500/- and GST would be applicable on the entire amount of Rs, 9000/- and not on [Rs.9000 - Rs. 7500] = Rs. 1500/-. The same was also clarified in serial number 5 of Circular No.109/28/2019 that the exemption from GST on maintenance charges charged by a RWA from residents is available only if such charges do not exceed Rs. 7500/- per month per member. In case the charges exceed Rs. 7500/- per month per member, the entire amount is taxable.

Availability of Input Tax Credit (ITC) for RWAs:

RWAs can avail of ITC on the following:

Inward supplies: GST paid on supplies received by RWA from vendors like on taps, pipes, other sanitary/hardware fillings etc.

Capital goods: GST paid on purchase of equipment, fixtures, appliances, generators, water pumps, lawn furniture etc.

Input services: GST paid on services like repair and maintenance services, security and housekeeping availed by RWA.

Disclaimer: The information given in this article is solely for purpose of understanding the law. It is completely based on the interpretation of the author and cannot be constituted as a legal advise, the author of this article and Lawcrux team is not responsible for any legal issues if arises on the basis of the interpretation given above.