Renting of Immovable Property-RCM or FCM

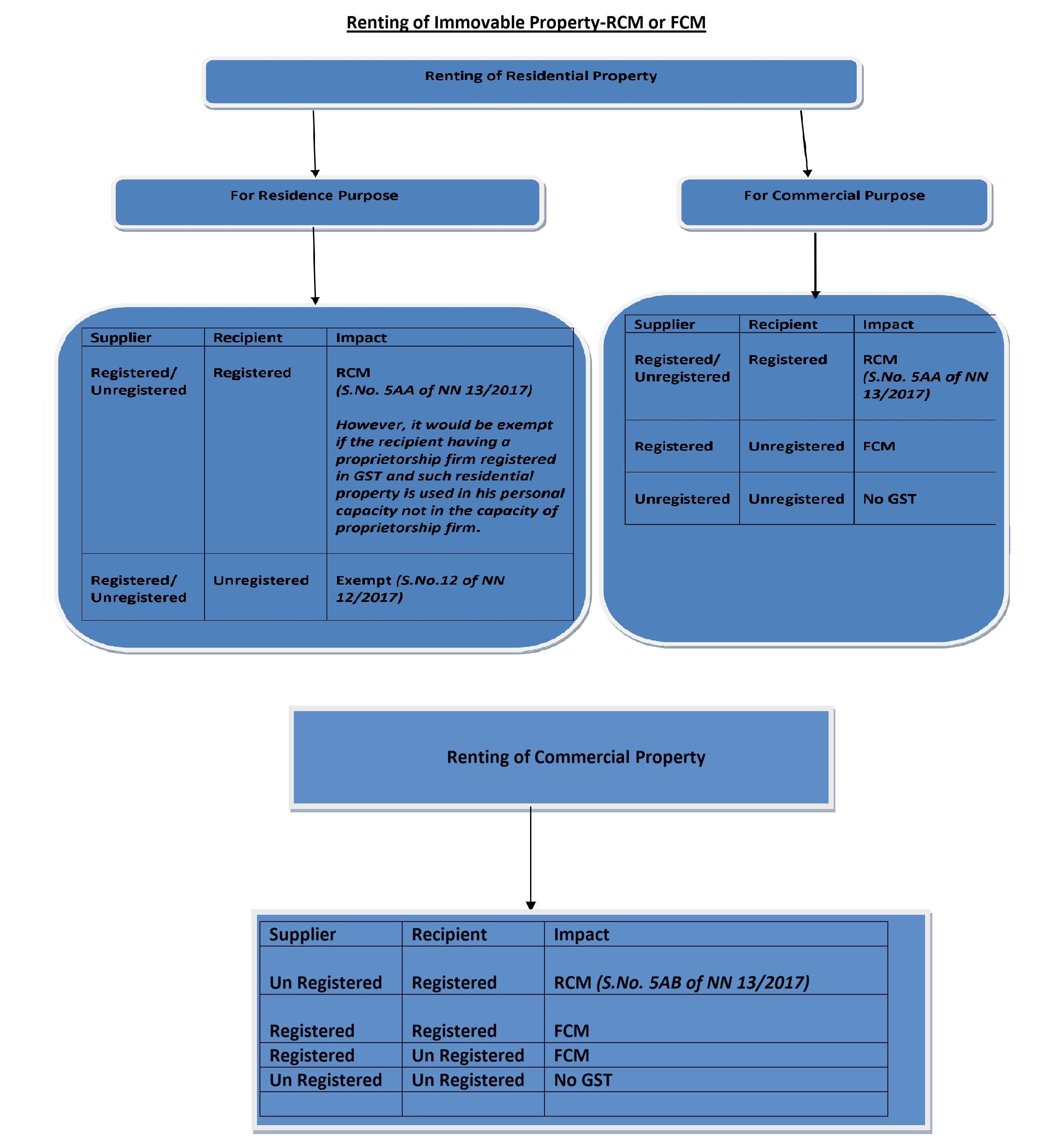

The renting of immovable property is a very crucial matter for discussion as from time to time many amendments are came under GST in respect of renting of immovable property. As per section 7(1)(a) of CGST Act 2017 the expression supply includes all forms of supply of goods or services or both such as sale, transfer, barter, exchange, licence, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business. Accordingly, the renting of immovable property would be considered as supply under GST. Further, the Schedule II of CGST Act 2017 contains the list of the activities or transactions which shall be treated as supply of goods or supply of services and as per clause(b) of para 2 of schedule II of CGST Act 2017 "any lease or letting out of the building including a commercial, industrial or residential complex for business or commerce, either wholly or partly, is a supply of services". Hence the renting of immovable property whether residential property or commercial property would be treated as supply of service. In this article we are going to understand the GST implications on renting of residential property & renting of commercial property with the help of following diagram;

|

|

Disclaimer: The information given in this article is solely for purpose of understanding the law. It is completely based on the interpretation of the author and cannot be constituted as a legal advise, the author of this article and Lawcrux team is not responsible for any legal issues if arises on the basis of the interpretation given above.