Metal Scrap- Everything You Need to Know

Every company who is engaged in manufacture of goods must have some transactions relating to waste & scrap. Such scrap can be of any form like plastic scrap, metal scrap, scrap of paper or paperboard, corrugated boxes scrap, scrap of glass, scrap of rubber etc. Recently, the 54thGST council Meeting was held on 09.09.2024, wherein the major changes in GST was recommended in relation to metal scrap. The said changes are now notified by the Central Government by issuing a Notification which shall come into force with effect from 10.10.2024. In this article we are going to discuss in detail about those changes in GST provisions in relation to Metal Scrap.

In

54th GST Council Meeting it was recommended that the Reverse

Charge Mechanism (RCM) to be introduced on supply of metal scrap by unregistered

person to registered. Further it was also recommended that the TDS would be

applicable under GST on supply of metal scrap by registered person to another

registered person. In view of the above recommendations of GST council, the

Central Government has issued two notifications, which shall come into force

w.e.f 10.10.2024;

I.

Notification No. 06/2024-Central Tax (Rate) dated 08.10.2024

II.

Notification No. 25/2024-Central Tax dated 09.10.2024

I. The Notification No. 06/2024-Central Tax (Rate) dated 08.10.2024 has amended the Notification No. 04/2017-Central Tax (Rate) which is the Principal Notification of RCM applicability u/s 9(3) in respect of the goods specified therein. The new serial number 8 has been inserted in NN 04/2017CT(R). The said serial number 8 of NN 04/2017 CT(R) is laid down as follows;

|

S.No |

Tariff item, sub-heading, heading or Chapter |

Description of supply of Goods |

Supplier of goods |

Recipient of supply |

|

8 |

72, 73, 74, 75, 76, 77, 78, 79, 80 or 81 |

Metal scrap |

Any unregistered person |

Any registered person. |

The above serial number 8 of NN 04/2017CT(R) states that if the metal scrap which is covered under chapter 72 to 81 is supplied by the person who is not registered under GST to another person who is registered under GST, then in such situation RCM would be applicable on such transaction. Hence the registered recipient has to deposit the tax under RCM.

In this respect the following two

questions are generally arises;

(i) What would be the rate of tax applicable for such RCM.

(ii) Whether the recipient would be eligible to claim ITC of such RCM deposited

by him.

Rate of tax of RCM in respect of Metal Scrap:

In this respect it is important to know that by inserting the serial number 8 in

the Notification No.04/2017 CT(R) the Government has just shifted the liability

to pay tax from the supplier to the recipient. Hence the rate of tax which is

generally applicable on the supply of metal scrap covered under

chapter 72 to 81

of custom tariff act, would be applicable in this situation. Currently as per

Notification No 01/2017 CT(R), the rate of tax in respect of supply of metal

scrap covered under chapter 72 to 81 is 18%, hence the RCM would also required

to be paid @ 18% in such situation.

Eligibility of ITC of RCM deposited on Metal Scrap:

There is no restriction provided in respect of claim of ITC of RCM deposited by

the registered recipient from the supplies received from unregistered person.

Hence the recipient can claim the ITC of tax deposited by him under RCM subject

to condition that he has self invoice as per the requirement of clause (f) of

sub section 3 of section 31 of CGST Act which states that a registered person

who is liable to pay tax under section 9(3) or

section 9(4) shall issue an

invoice in respect of goods or services received by him from the supplier who is

not registered.

II.

To enable the TDS provisions in case of supply of metal scrap received from

registered person the Notification No. 25/2024-CT dated 09.10.2024 has been

issued which has amended the Notification No. 50/2018-CT dated 13.09.2018 and

inserted a clause (d) in the said notification. The said clause (d) is laid down

as follows;

“(d) any registered person receiving supplies of metal scrap falling under

Chapters 72 to 81 in the First Schedule to the Customs Tariff Act, 1975 (51 of

1975), from other registered person”

Thus as per above clause (d), if the registered person has received the metal scrap (covered under chapter 72 to 81 of custom tariff) from another registered person, then such registered person is required to deduct TDS u/s 51 from the payment made to the supplier.

Relevant Provisions of TDS contained in CGST Act & CGST Rules 2017:

In this respect it necessary to refer the provisions of

section 51 of CGST Act

2017 which states that TDS at the rate of one per cent is required to be

deducted from the payment made or credited to the supplier of taxable goods or

services or both, where the total value of such supply, under a contract,

exceeds Rs. 2,50,000/- . In other words TDS @2% (1% under each head) is to be

deducted, however if the total value of such supply under a contract is upto

2,50,000/- then in such situation no TDS would be deducted. Further as per the

proviso to section 51(1) no deduction shall be made if the location of the

supplier and the place of supply is in a State which is different from the state

of registration of the recipient. Sub section 2 of

section 51 of CGST Act

states that the amount deducted shall be paid to the Government by the deductor

within 10 days following the end of the month in which such deduction is made.

Further as per Rule 12 of CGST Rules 2017 any person required to deduct tax u/s 51 shall submit an application in FORM GST REG-07 for the grant of registration through the common portal and the proper officer may grant registration after due verification and issue a certificate of registration in FORM GST REG-06. Also it is important to know that as per provisions of Rule 66 of CGST Rules 2017, the person who is required to deduct TDS u/s 51 shall furnish a return in FORM GSTR-7. The details of which shall be available to each deductee on the common portal for claiming the amount of tax deducted in his electronic cash ledger. The TDS certificate shall also be made available to the deductee on the common portal in FORM GSTR-7A.

Advisory for Taxpayers: New GST Provision for Metal Scrap Transactions:

As discussed above the person who is required to deduct TDS

u/s 51 is required

to submit an application for registration in

Form GST REG-07. However, since the

businesses dealing with Metal Scrap were earlier not required to deduct TDS

u/s

51 and accordingly, were not required to obtain registration earlier in

Form GST

REG-07, hence the common portal is not updated to enable the compliances of

registration through Form GST-REG-07 by these categories of persons who are

dealing in metal scrap.

Accordingly, an advisory has been issued by GST portal on dated 13.10.2024 the GST portal will soon be updated to enable compliance of registration through FORM GST REG-07 by these category of registered persons.

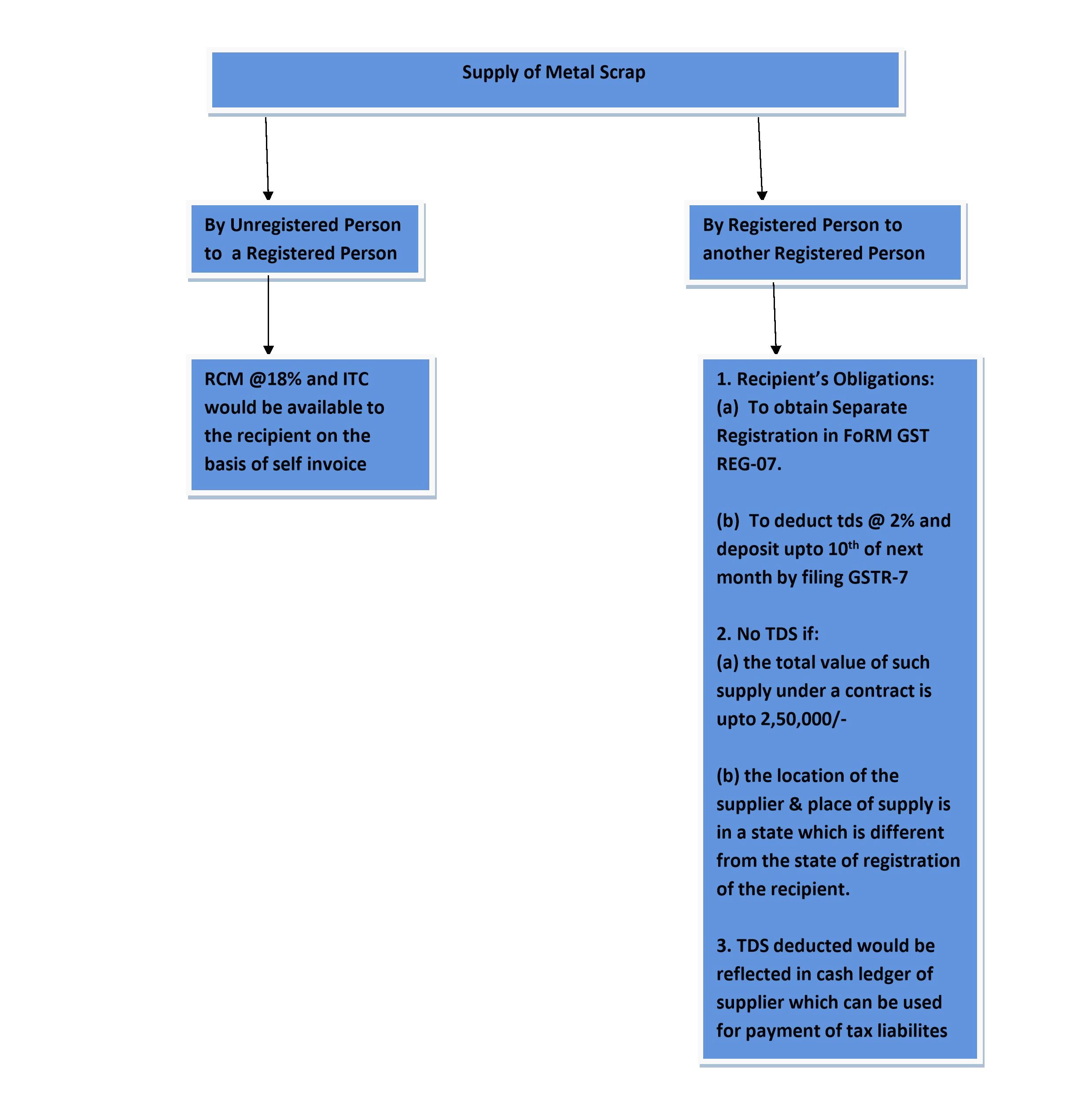

Now, before concluding this article, i would like to give a brief summary about the GST & TDS implications relating to Metal Scrap transactions which are applicable from 10.10.2024:

I.

Supply of Metal Scrap by un-registered person to registered person:

RCM would be applicable @18% and ITC would be available to recipient on the

basis of self invoice issued by the recipient.

II. Supply of Metal Scrap by registered person to another

registered person:

(a) TDS @2% is required to be deducted by the recipient from the payment made or

credited to the supplier;

(b) TDS is only required when the total value of such supply under a contract exceeds 2.5 Lacs;

(c) The person who is deducting TDS

(i.e., Recipient) is required:

(i) to obtain separate registration in Form GST REG-07.

(ii) to file Form GSTR-7 return on or before 10th of succeeding month and

discharge his TDS liability.

(d) Once GSTR -7 has been filed, GSTR-7A shall be issued acting as a Certificate of TDS deducted.

(e) The TDS deducted would be reflected in the cash ledger of supplier, which can be utilized by the supplier to discharge tax liabilities.

(f) No TDS if the location of the supplier and the place of supply is in a state which is different from the state of registration of the recipient.

Conclusion:

|

|

Disclaimer: The information given in this article is solely for purpose of understanding the law. It is completely based on the interpretation of the author and cannot be constituted as a legal advise, the author of this article and Lawcrux team is not responsible for any legal issues if arises on the basis of the interpretation given above.