Audit under GST

Audit means the examination of records, returns and other documents maintained or furnished by the registered person under this Act or the rules made thereunder or under any other law for the time being in force to verify the correctness of turnover declared, taxes paid, refund claimed and input tax credit availed and to assess his compliance with the provisions of this Act or the rules made thereunder. Under GST Law, there are two sections containing the provisions of Audit. In this article we will discuss the types of audits under GST, procedure for conducting the audit and what are obligations & rights of the registered person whose audit is conducted.

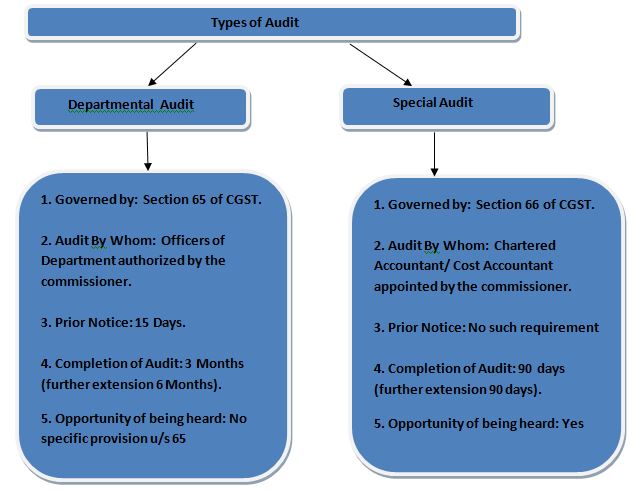

Types of Audit:

1. Audit by Tax Authorities (Departmental Audit Section 65)

(i) Firstly the proper officer authorised to conduct audit shall issue a notice in FORM GST ADT-01 to the auditee.

(ii) Said notice should be issued at least 15 working days prior to the conduct of audit.

(iii) The period of audit to be conducted shall be a financial year or part thereof or multiple years.

(iv) The audit shall be completed within 3 months (which can be further extended by a period not exceeding six months) from the date of commencement of the audit.

(v) The proper officer will inform the registered person of the discrepancies noticed/ observed in the audit and the said person may file his reply and the proper officer shall finalise the findings of the audit after due consideration of the reply furnished.

(vi) On conclusion of audit the proper officer shall inform the registered person within 30 days, about the findings and the reasons for such findings in FORM GST ADT-02.

(vii) In case of detection of tax not paid or short paid or erroneously refunded or ITC wrongly availed or utilised, the proper officer may initiate action u/s 73 or 74 or section 74A.

Judicial Pronouncements:

(i). Final audit report submitted without considering the reply to discrepancy notice:

In case of PBL Transport Corporation Private Limited Versus The Assistant Commissioner ST [2024(01)LCX0284] the Petitioner had filed reply to the discrepancy notice under Rule 101(4) of the APGST/CGST Rules, 2017, but without considering the same the Final Audit Report was submitted. The petitioner is challenging the Final Audit Report mainly on the ground of violation of the principles of natural justice.

The Andhra Pradesh High Court held that in view of Rule 101(4), it is evident that after informing about the discrepancies noticed, if the person files the reply, the same is to be considered and on such consideration, the findings of the Final Audit Report are to be furnished. Here, it is now not disputed that the petitioner filed the reply and the same was not considered while finalizing the findings of the audit. The Final Audit Report is therefore in violation of the principles of natural justice as also the statutory provisions.

The writ petition is partly allowed. The impugned Final Audit Report is quashed only on the said ground. The respondents shall now consider the petitioner’s reply to the discrepancy notice and shall finalize the audit report. Thereafter, they shall proceed further, in accordance with law.

(ii). Prior notice to conduct the audit:

In case of Vardhaman Gold versus The State of Andhra Pradesh[2023(11)LCX0368] the Andhra Pradesh High Court held that notice of information that the audit will be conducted is to be given to the registered person and such notice shall be not less than 15 working days, prior to the conduct of audit.

2. Special Audit (Section 66):

(i) If the Assistant Commissioner at any stage of scrutiny, inquiry, investigation, is of the opinion that the value has not been correctly declared or the credit availed is not within the normal limits, he shall issue a direction in FORM GST ADT-03 to the registered person to get his records audited by a chartered accountant or a cost accountant specified in the said direction.

(ii) The chartered accountant or cost accountant so nominated shall within the period of 90 days, submit a report of such audit to the said Assistant Commissioner. The period of 90 days can be further extended by 90 days.

(iii) The expenses of the special audit:

The expenses for examination and audit including the auditor’s remuneration will be determined and paid by the Commissioner.

(iv) On conclusion of the special audit, the registered person shall be informed of the findings of the special audit in FORM GST ADT-04.

(v) The taxable person will be given an opportunity of being heard in the findings of special audit. If the result in detection of unpaid/ wrong refund etc .The recovery will start against the registered person after this auditing.

3. Comparison between these two Audits:

|

|

4. Obligations of the Auditee:

The taxable person will be required to provide the necessary facility to verify the books of account/other documents as required to give information and assistance for timely completion of the audit.

Disclaimer: The information given in this article is solely for purpose of understanding the law. It is completely based on the interpretation of the author and cannot be constituted as a legal advise, the author of this article and Lawcrux team is not responsible for any legal issues if arises on the basis of the interpretation given above.