Goods Exported but Payment not Received from the Foreign Customer:

There are various benefits which are provided to the exporters under GST law, Customs & FTP law, like refund of IGST or accumulated ITC under GST, duty drawbacks under Customs and RoDTEP benefit under the FTP. The reason for providing these benefits to the exporter is that they help in earning the foreign currency (FOREX) to the government. But what if these export proceeds are not realised? In this article we will discuss this situation when the goods are exported by the Indian Exporter to their foreign customer and the various export benefits are availed by the said exporter but the payments are not realised from the foreign customer.

Time period allowed under FEMA

for realisation of export proceeds:

As per para 1 of Regulation 9

of Foreign Exchange Management (Export of Goods & Services) Regulations, 2015

the amount representing the full export value of goods / software/ services

exported shall be realised and repatriated to India within nine months or within

such period as may be specified by the Reserve Bank, in consultation with the

Government, from time to time, from the date of export, provided.

Accordingly, in case of export whether export of goods or services the export proceeds should be realised within 9 months.

What constitutes export of

goods/services?:

Before going into detailed discussions let’s have a look into the definition

of export of goods & export of services. As per the definition of export of

goods the term "export of goods" with its grammatical variations and cognate

expressions, means taking goods out of India to a place outside India. Further,

for the transaction to be considered as “export of service” the following

conditions are to be fulfilled;

(i) the supplier of service is located in India;

(ii) the recipient of service is located outside India;

(iii) the place of supply of service is outside India;

(iv) the payment for such service has been received by the supplier of service

in convertible foreign exchange; or in Indian rupees wherever permitted by the

Reserve Bank of India and

(v) the supplier of service and the recipient of service are not merely

establishments of a distinct person in accordance with Explanation 1 in section

8;

From reading the above two definitions we found that the condition for realisation of payment in the convertible foreign exchange is only for the export of service but not for the export of goods. The definition of export of goods does not specify any condition for the realisation of export proceeds. Here the question comes: From where the requirement for the realisation of export proceeds arose in case of export of goods?

Rule 96B plays an important

role here:

As per rule 96B(1) of CGST

Rules, 2017 where any refund of unutilised input tax credit on account of export

of goods or of integrated tax paid on export of goods has been paid to an

applicant but the sale proceeds in respect of such export goods have not been

realised, in full or in part, in India within the period allowed under the FEMA,

the person to whom the refund has been made shall deposit the amount so

refunded, to the extent of non- realisation of sale proceeds, along with

applicable interest within 30 days of the expiry of the said period, failing

which the amount refunded shall be recovered in accordance with the provisions

of section 73 or

74 of the Act, as the case

may be, as is applicable for recovery of erroneous refund, along with interest

u/s 50.

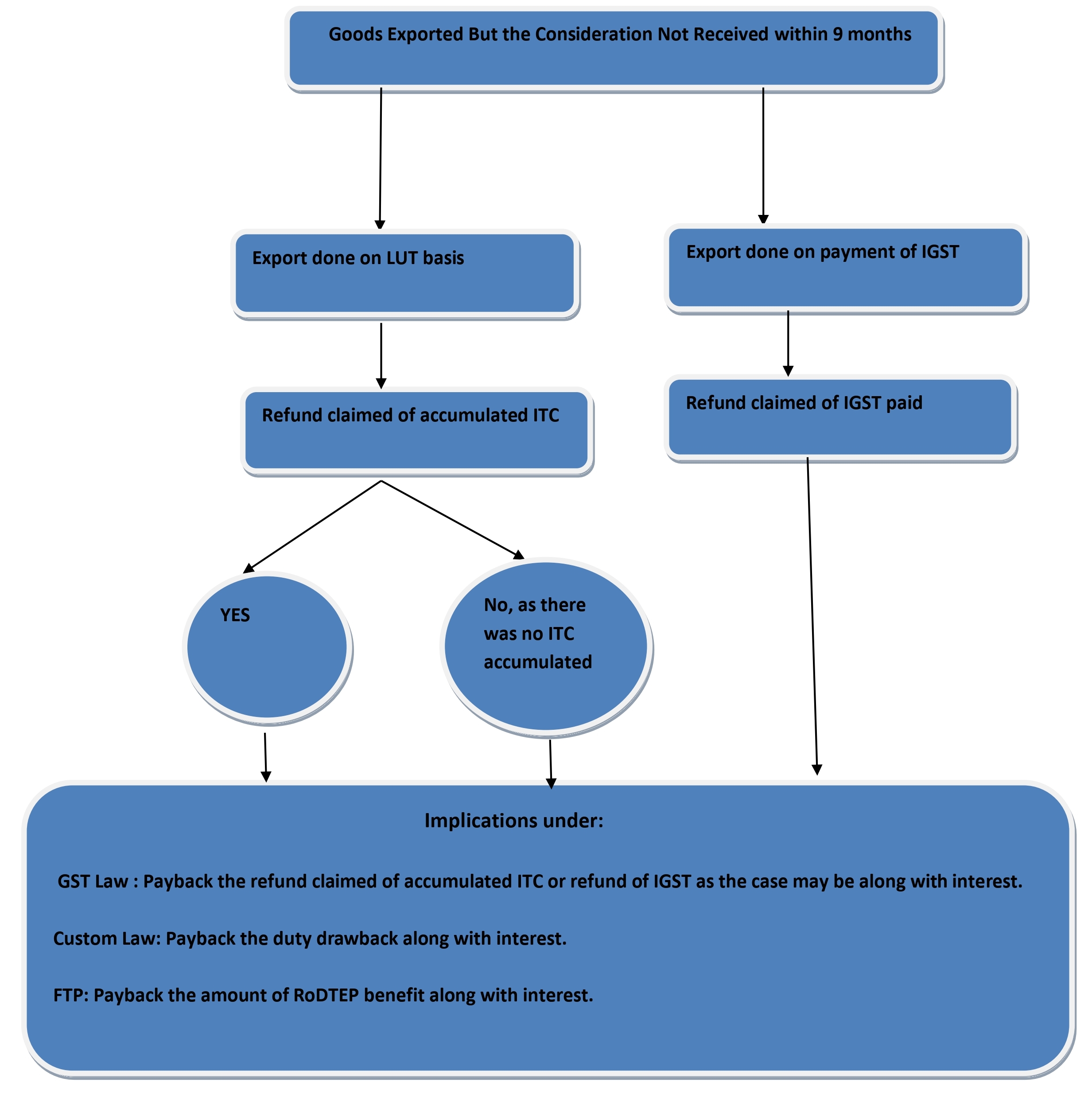

Thus as per rule 96B it is clear that when the goods are exported on payment of IGST and refund has been claimed of said IGST amount but the export proceeds are not realised within the time limit prescribed under FEMA then the exporter has to deposit the said amount. Similarly, if goods are exported on LUT basis and the refund of accumulated ITC is claimed by the exporter but the export proceeds are not realised within the time limit prescribed under FEMA then the exporter has to deposit the said refund amount.

One important point that is to be noted here is that Rule 96B does not cover the situation when the goods are exported on LUT basis but the ITC is not accumulated in the credit ledger and as the same is used in the domestic supplies. In this situation no refund is claimed by the exporter for unutilised ITC under GST and now if the export proceeds are not realised what would be the consequences under GST?

In the said situation since no refund of accumulated ITC is claimed by the exporter hence it is clear that rule 96B would not be applicable here, as the rule 96B covers the provisions for Recovery of refund of unutilised input tax credit or integrated tax paid on export of goods where export proceeds not realised. Accordingly the rule 96B does not have direct implications here.

However, it can be argued by the department that there is no supply involved in this case hence the ITC which was claimed on inputs need to be reversed. This stance of the department can be challenged on the ground that at the time of exporting the goods there was no way of knowing that the amount will be realised or not in the future, hence it should not be deemed that no supply was done during that time. Accordingly, there is no requirement to reverse the ITC of inputs.

Impacts of Non realisation of

Export Proceeds under Customs:

As we know that under the custom law the benefits in form of “Duty

Drawbacks” are available for the exporters. In this respect it is important to

know that like rule 96B of CGST

Rules 2017 there is a Rule 18

of the Customs and Central Excise Duties Drawback Rules, 2017 which states that

where an amount of drawback has been paid to an exporter or a person authorised

by him but the sale proceeds in respect of such export goods have not been

realised by or on behalf of the exporter in India within the period allowed

under the FEMA, such drawback shall be recovered.

Thus it is clear that the amount of the duty drawback availed by the exporter shall be paid back to the government in the event of non realisation of export proceeds within the time limit specified in the FEMA.

Impacts of Non realisation of

Export Proceeds under FTP:

As per para 2.54 of Foreign

Trade Policy 2023 if an exporter fails to realize export proceeds within the

time specified by RBI, they would be liable to return all benefits/incentives

availed against such exports along with applicable interest, penalty, etc. in

accordance with the provisions of FT (D&R) Act, Rules and the FTP 2023.

Thus from the above it is clear that all benefits availed by the exporter under FTP (like RoDTEP benefits) are to be paid by the exporter when the export proceeds are not realised within the time period allowed under FEMA.

What if the Export Proceeds

are Realised Subsequently:

Imagine a situation where the exporter Mr.A has exported some goods on

payment of IGST and claimed a refund of such IGST amount but the export proceeds

are not realised within the time limit prescribed under FEMA i.e., 9 months and

accordingly Mr.X has paid back the refund to the government along with interest.

Now, if the export proceeds are realised subsequently then what would be the

situation? Whether the exporter Mr.A would receive back the amount of refund

paid by him? What about the interest amount paid by him earlier? Whether said

interest paid by him would also be received back from the government?

Rule 96B(2) has the answer:

Sub rule 2 of Rule 96B states

that where the sale proceeds are realised by the applicant, in full or part,

after the amount of refund has been recovered from him and the applicant

produces evidence about such realisation within a period of three months from

the date of realisation of sale proceeds, the amount so recovered shall be

refunded by the proper officer, to the applicant to the extent of

realisation of sale proceeds.

Accordingly, when the export proceeds are realised subsequently, then as per Rule 96B(2) the exporter on producing the evidence would be eligible to receive back the said amount which was recovered from him earlier. Since as per the wordings of Rule 96B(2) the amount so recovered shall be refunded by the proper officer to the exporter.

The exported goods are

received back due to non receipt of consideration or for any reason:

Generally, when the exported goods are rejected by the foreign customer due

to quality issues or any other reason, then the exporter does not show any

interest in receiving back those goods since it can increase the cost of

exporter. However, when the exporter wants to receive back the goods the

important question that comes to mind is whether such exporter would be liable

to pay various duties which were otherwise payable for importing such goods.

Attention is invited to the Notification No.45/2017-Customs which provides an exemption to re-import of goods exported under duty drawback, rebate of duty or under bond on or after the 1st July 2017. The said notification exempts the goods when re- imported into India, from so much of the duty of customs leviable thereon and integrated tax, compensation cess leviable thereon u/s 3(7) and 3(9) of Customs Tariff Act, as is in excess of the amount specified therein.

Thus when the export proceeds are not realised from the foreign customer and the exporter wants to receive back these goods in India, in such situation no custom duties, integrated tax & compensation cess would be payable subject to the conditions specified in the NN 45/2017 Customs.

Conclusion:

Disclaimer: The information given in this article is solely for purpose of understanding the law. It is completely based on the interpretation of the author and cannot be constituted as a legal advise, the author of this article and Lawcrux team is not responsible for any legal issues if arises on the basis of the interpretation given above.