ITC Blocking Under Rule 86A: Where Limits Clash with Authority

Imagine logging into your GST portal, expecting to use your Input Tax Credit (ITC) to offset your tax liability—only to find that your credit is suddenly blocked. No prior notice, no immediate explanation, just a restriction that leaves you scrambling to understand what went wrong. This is the reality many businesses face under Rule 86A of the CGST Rules (“Rule 86A”), a provision that allows tax authorities to restrict ITC if they suspect fraudulent claims.

The introduction of Rule 86A was not arbitrary—it was a response to large-scale tax evasion through fake invoices. However, its implementation has raised critical concerns. How does the rule work? What safeguards exist to prevent misuse? And what remedies are available if your ITC is unfairly blocked?

This article unpacks the origins, legal framework, and impact of Rule 86A, while also addressing the judicial scrutiny and the measures taxpayers can take if they find themselves at the receiving end of an ITC freeze.

Why Rule 86A Was Introduced – The GST Council’s Rationale

Rule 86A was introduced to tackle fraudulent ITC claims, a growing challenge under the GST system.

The issue gained prominence during the 38th GST Council meeting, where investigations revealed large-scale misuse of ITC through fake invoices.

The Principal Commissioner, GST Policy Wing (CBIC), highlighted cases where ITC was availed without actual purchases.

A major challenge was the self-assessment nature of GSTR-3B, which made it difficult to track whether ineligible ITC was reversed as required under Section 16 of the CGST Act.

Some State tax officers had already been using an ITC blocking facility on the GST portal across 25 States/UTs.

To ensure uniform enforcement and stronger tax administration, the GST Council recommended Rule 86A, granting specified tax authorities the power to block ITC utilization in cases of suspected fraud.

Rule 86A was formally inserted into the CGST Rules, 2017, via Notification No. 75/2019 dated 26.12.2019, allowing authorities to restrict the use of ineligible or fraudulently availed ITC.

Understanding Rule 86A: Blocking ITC to Prevent Misuse

Rule 86A empowers the Commissioner or any officer authorized by the Commissioner, not below the rank of an Assistant Commissioner, to block any taxpayer from debiting the electronic credit ledger if they have reasons to believe that the credit has been fraudulently availed or is otherwise ineligible. This power can be exercised for the following reasons:

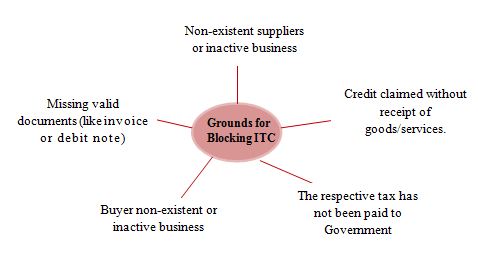

ITC availed on invoices from non-existent suppliers or the supplier is not conducting the business from the registered place.

ITC availed on invoices without receipt of goods or services or both.

ITC availed on invoices in respect of which tax has not been paid to the government.

ITC availed by a taxpayer who is non-existent or not conducting business from the registered address.

ITC claimed without possessing a valid tax invoice or debit note or any other document (specified under Rule 36)

In such cases, authorities may restrict the taxpayer from utilizing ITC to offset liabilities or claim refunds. However, this restriction is temporary and must be lifted once the conditions for blocking no longer exist, with an automatic expiry after one year.

But wait—doesn’t this rule serve the same purpose as Sections 73 and 74 of the CGST Act? The purpose is to recover ITC that has been availed or utilized either fraudulently or is otherwise ineligible. However, these sections and Rule 86A differ in their approach.

Sections 73 and 74 provide a structured adjudication process to determine tax liabilities. They ensure that before any recovery action is taken, taxpayers get a chance to present their case, respond to notices, and contest claims through a well-defined legal framework. The outcome is a demand order specifying the tax payable, interest, and penalties, if applicable.

Rule 86A, on the other hand, operates as a preventive measure. It enables tax authorities to block ITC even before any adjudication under Sections 73 or 74 is completed. While both ultimately result in denying ITC, the process under Rule 86A is administrative and discretionary, lacking the procedural safeguards of an adjudication process.

Key Issues Emerging from Rule 86A

While Rule 86A was introduced to curb fraudulent ITC claims, its implementation has raised several concerns among taxpayers. The discretionary nature of ITC blocking, coupled with the absence of procedural safeguards, has led to various legal challenges. Judicial scrutiny has highlighted the following key issues:

Issue 1: Lack of "Reason to Believe," Inadequate Recording of Reasons, and No Personal Hearing

Issue 2: ITC Blocking Beyond One Year

Issue 3: Negative Blocking of ITC

These issues have been extensively challenged before various High Courts, leading to important jurisprudence that clarifies the scope and limits of Rule 86A. The following sections will discuss these issues in detail, examining key judicial precedents and their implications.

ITC Blocking: Flimsy Reasons, No Justification—And No Chance to Defend Yourself

Rule 86A vests tax officers with substantial authority when they have "reason to believe" that certain transactions or invoices are dubious. This belief must be grounded in objective evidence and not merely on speculation or conjecture. Given that "reason to believe" is inherently subjective; its interpretation may vary from one officer to another, potentially leading to inconsistencies in its application. Secondly, recording of reasons is a must before blocking e-credit ledger. These broad discretionary powers has raised serious concerns, as judicial scrutiny has revealed cases where ITC blocking was done arbitrarily, often without independent reasons recorded by the officer.

The Gujarat High Court, in the case of M/s S.S. Industries vs. Union of India[2020(12)LCX0107], laid down key conclusions in Para 65 regarding the invocation of Rule 86A which are as follows:

✓ that ITC blocking under this rule is justified only when there is credible material indicating fraudulent transactions, such as fake invoices.

✓ Mere suspicion or weak evidence is insufficient to invoke this power.

✓ Given the drastic nature of ITC blocking power, the Court emphasized that it should be exercised sparingly and only on strong, objective grounds.

✓ The Court cautioned against misuse, warning that it should not be used as a tool to harass taxpayers or cause irreversible harm to businesses.

✓ The Court distinguished between availing and utilizing ITC, stating that availing ITC does not create a vested right—the right becomes vested only after lawful utilization.

✓ Finally, the Court urged the government to establish clear guidelines to regulate the application of Rule 86A and prevent arbitrary actions that could adversely impact businesses.

CBIC Guidelines on Rule 86A: Key Takeaways

In this regard, CBIC issued detailed guidelines CBEC-20/16/05/2021-GST/1552 dated 2.11.2021 for the officers exercising powers under Rule 86A. These guidelines clarify:

➢ Grounds for disallowing debit from the e-credit ledger,

➢ Proper authority for Rule 86A,

➢ Procedure for blocking credit and

➢ Allowing debit of disallowed/restricted credit under Rule 86A(2)

Let's break down each of these points.

Grounds for Blocking ITC

Rule 86A allows blocking ITC if there is reason to believe that credit has been fraudulently availed or is ineligible. Grounds include:

|

|

Before blocking ITC under Rule 86A, the authority must carefully assess all relevant facts, including the nature and amount of fraudulent or ineligible ITC, and determine if such action is necessary to protect revenue. This power should not be exercised mechanically but must be justified by credible evidence rather than mere suspicion. Given its extraordinary nature, ITC blocking should be applied cautiously and only to prevent wrongful use of ineligible credit.

Proper Authority for Rule 86A

The Commissioner or authorized officers, depending on the amount of disputed ITC, can block ITC. Monetary limits are set for different officer ranks:

|

Total amount of ineligible or fraudulently availed input tax credit |

Officer to disallow debit of amount from electronic credit ledger under Rule 86A |

|

Not exceeding Rs.1 crore |

Deputy Commissioner/Assistant Commissioner |

|

Above Rs.1 crore but not exceeding Rs.5 crores |

Additional Commissioner/Joint Commissioner |

|

Above Rs.5 crore |

Principal Commissioner/Commissioner |

Procedure for Blocking ITC

✓ Officers must ascertain, based on material evidence, whether the ITC was fraudulently availed or ineligible before blocking it under Rule 86A.

✓ The Commissioner or an authorized officer, within prescribed monetary limits, must form a reasoned opinion on the necessity of blocking ITC to prevent misuse or revenue loss.

✓ The reasons for blocking ITC must be documented in writing before taking action.

✓ The amount blocked should not exceed the suspected ineligible ITC.

✓ The registered person must be informed of the action via the GST portal, along with details of the officer responsible.

Lifting ITC Block (Rule 86A(2)) &Timely Investigation and Adjudication

If ITC was blocked if suspected of fraud or ineligibility, the Commissioner/ officer either on his own or based on taxpayer submissions with evidence, may review the case.

If ITC is found eligible (fully or partially), the restriction can be lifted with proper documentation.

The block automatically expires after one year, allowing credit use unless further action is taken.

Investigations should be completed within one year to protect revenue and taxpayer’s working capital.

Despite the issuance of the guideline, the subjected issues persisted, and it did not provide for personal hearings or address this concern.

In K-9 Enterprises v. State of Karnataka [2024(04)LCX0582], the Hon'ble Karnataka High Court held that the pre-decisional hearings prior to blocking of Electronic Credit Ledger are mandatory. Further, ‘reasons to believe' have to be strictly complied by the authorized authority. Further, the decision in K-9 Enterprises was followed by the Hon'ble Karnataka High Court in The Lead Factory vs. Assistant Commissioner of Commercial Taxes [2024(10)LCX0014].

Additionally, in the case of Tvl J M Traders vs. The Deputy Commissioner (ST) [2024(02)LCX0148], the Madras High Court held that Rule 86A allows officers to block ITC if they believe it was claimed fraudulently or is ineligible. The officer must provide written reasons for this action to the taxpayer. Although the Rule does not stipulate a prior notice, providing written reasons at the time of blocking is essential. In this case, only the supplier’s name was mentioned in the ledger, with no reasons provided. Consequently, the petitioner is entitled to the unblocking of the ITC.

ITC Blocking Beyond One Year: Unlawful and Unjust

Further, Rule 86A(3) explicitly states that ITC blocking is permissible for a maximum period of one year. However, in some instances, the department continues to restrict taxpayers from debiting their Electronic Credit Ledger even after this period expires. Such actions unjustly deprive taxpayers of their rightful ITC utilization.

Several judicial rulings have addressed this issue. In Barmecha Tax Fab Pvt. Ltd. vs. Commissioner [2022(01)LCX0087], the Gujarat High Court categorically held:

“4. The rule itself has provided that the Electronic Credit Ledger can be blocked for a period of one year. On expiry of a period of one year, it would automatically get unblocked. In fact, it was the duty of the authority concerned to permit the assessee, i.e. the writ-applicant, to avail the input credit available in his ledger. Once the statutory period comes to an end, the authority has no further discretion in the matter, unless a fresh order is passed. In the case on hand, it is very unfortunate to note that despite the fact that the period of one year elapsed, the authority did not permit the writ-applicant to avail the credit available in his ledger. Even representation was filed in this regard but the authority thought fit not to pay heed to such representation.

5. We may further note that the authority did not permit the writ-applicant to avail the input credit available in his ledger for about more than two and a half months after the statutory life of the order came to an end.

6. We make it clear that next time if we come across such a case, then the concerned authority would be held personally liable for the loss which the assessee might have suffered during the interregnum period.”

A similar stance was taken in M/s Aegis Polymers vs. Union of India &Ors. [2021(07)LCX0093] and Advent India PE Advisors Private Limited vs. Union of India &Ors. [2021(12)LCX0003], where the courts reaffirmed that ITC blocking under Rule 86A cannot exceed one year. Once this period lapses, the ledger should be automatically unblocked unless fresh proceedings are initiated.

The Issue of Negative Blocking: A Legal Overreach?

One of the most glaring issues with Rule 86A is Negative Blocking. A closer look at the rule’s precise wording leaves no room for doubt—blocking ITC beyond the available balance is simply not permitted.

1. "Credit of input tax available in the electronic credit ledger has been fraudulently availed or is ineligible."

This opening phrase alone demolishes any argument for negative blocking. The rule explicitly applies only to ITC that is available in the electronic credit ledger. Let’s break it down:

First, ITC must be available—how can authorities block something that doesn’t even exist? It’s like trying to freeze a bank account with a zero balance!

Second, the entire restriction under Rule 86A is intrinsically tied to the actual ledger balance. Its application cannot extend beyond what’s present.

And most importantly, if the legislature had intended to allow negative blocking, it would not have confined the provision to available credit. The deliberate wording is crystal clear—blocking beyond the existing balance was never the intent.

2. "Not allow debit of an amount equivalent to such credit in electronic credit ledger."

The phrase "equivalent to such credit" is key. The words "such credit" directly reference the earlier phrase "credit of input tax available in the electronic credit ledger." This linkage is critical—it unequivocally establishes that ITC blocking is capped at the amount actually present in the ledger.

Blocking more than what exists would create a negative balance, a concept that has no legal foundation under Rule 86A. If the law had meant to permit negative blocking, it would have said so explicitly—but it doesn’t.

Simply put: Negative Blocking has no legal basis. The law does not support it, the rule does not allow it, and the legislature never intended it. Any attempt to enforce negative blocking is not just overreach—it’s outright unlawful.

Despite this clear restriction, tax officers have, in some cases, attempted to block more than the available balance, leading to disputes. Courts have repeatedly intervened, reinforcing that such actions exceed the scope of Rule 86A and amount to an overreach of power."

The Hon'ble Gujarat High Court in Samay Alloys India Pvt Ltd [2022(02)LCX0062], clarified that Rule 86A can only block existing credit (with written reasons), not future credits. The relevant extract is reproduced below;

“57. For all the foregoing reasons, this writ application succeeds and is hereby allowed. The respondents are directed to withdraw negative block of the electronic credit ledger at the earliest. We rule that the condition precedent for exercise of power under Rule 86A of the GST Rules is the availability of credit in the electronic credit ledger which is alleged to be ineligible. If credit balance is available, then the authority may, for reasons to be recorded in writing, not allow the debit of amount equivalent to such credit. However, there is no power of negative block for credit to be availed in future. The writ applicants are also entitled to the refund of Rs.20 Lakh deposited by them to enable them to file their return. The respondents shall refund this amount of Rs.20 Lakh to the writ applicants within a period of two weeks from the date of the receipt of the writ of this order.”

Reaffirming this stance, the Hon’ble Gujarat High Court in PMW Metal and Alloys Pvt Ltd [2024(09)LCX0440] held that credit in the Electronic Credit Ledger cannot be blocked if there is no sufficient balance available. The court directed the respondents to withdraw the negative block of Rs. 2,44,05,567/- at the earliest. Any remaining balance in the Electronic Credit Ledger, after removing the negative block, was restricted from use by the petitioner until a show cause notice, if any, was issued under Sections 73 or 74 of the GST Act. The ruling allowed the petitioner to file returns with the appropriate tax, penalty, and interest once the negative block was lifted, as determined in accordance with law.

Similarly, the Hon’ble Telangana High Court in the case of Laxmi Fine Chem [2024(03)LCX0372], held as under:

“7. Taking into consideration the decision of the Division bench of Gujarat High Court which has also been relied upon by this High Court and by this very Bench in yet another writ petition i.e., W.P. No. 31039 of 2023, decided on 20.11.2023, we find that the action on the part of the respondents in passing an order of negative credit to be contrary to Rule 86(A). In the event, if no input tax credit was available in the credit ledger, the rules does not provide for insertion of negative balance in the ledger and therefore what was permissible was only to the block the electronic credit ledger and under no circumstances could there had been an order for insertion of negative balance in the ledger. If there is a credit balance available, then the authorities concerned in terms of provisions of Rule 86(A) may for reasons to be recorded in writing not allowed the credit of the said amount available equivalent to such credit. However, there is no power conferred upon the authorities for block of the credit to be availed by the petitioner in future.”

Expanding on this principle, the Hon’ble Delhi High Court in the Best Crop Science Pvt Ltd [2024(09)LCX0139], held that Rule 86A is not a recovery mechanism but an emergent measure to protect revenue by temporarily blocking the debit of ITC in the electronic credit ledger (ECL) if the Commissioner or authorized officer believes it was wrongfully availed. Importantly, Rule 86A(1) does not allow negative blocking, i.e., it cannot require a tax payer to replenish their ECL with valid ITC to offset past credits believed to be fraudulent or ineligible. Such an interpretation would effectively turn Rule 86A into a recovery tool, which is not its purpose and increasing the taxpayer’s cash outflow and denying them the use of validly availed ITC.

Further, while adjudicating on this issue, the court expressly disagreed with the rulings in Basanta Kumar Shaw [2022(07)LCX0086] and R.M. Dairy Products LLP [2021(07)LCX0157], observing that:

"62. We are, respectfully, unable to concur with the aforesaid interpretation for the reason that it is not in conformity with the opening line of Rule 86A(1) of the Rules. The words "credit of input tax available in the electronic credit ledger" plainly refers to the credit which is at the given point of time available in the taxpayer's ECL. If the same had already been utilized in payment of tax, penalties or other dues or has been refunded, the same would not be available in the ECL."

Conclusion: Striking a Balance Between Prevention and Protection

Rule 86A of the CGST Rules was introduced as a necessary measure to curb fraudulent ITC claims, but its implementation has raised significant legal and procedural concerns. While the rule empowers authorities to block ITC in cases of suspected fraud, judicial pronouncements have repeatedly emphasized that this power must be exercised judiciously, with due process and adherence to clear safeguards. Courts have ruled that ITC blocking cannot be arbitrary, must be based on credible evidence, and cannot exceed the statutory period of one year.

Additionally, the issue of "negative blocking" has been decisively addressed—ITC can only be restricted to the extent available in the electronic credit ledger, not beyond. These rulings reinforce the principle that while revenue protection is important, taxpayers' rights cannot be trampled upon in the process.

As litigation around Rule 86A continues to evolve, it is evident that stricter guidelines and procedural safeguards are necessary to prevent misuse. Until then, taxpayers must remain vigilant, challenge arbitrary ITC blocking, and ensure that authorities adhere to legal principles before restricting their working capital. The balance between preventing fraud and protecting genuine businesses must not be tilted disproportionately in favor of unchecked administrative discretion.

Disclaimer: The information given in this article is solely for purpose of understanding the law. It is completely based on the interpretation of the author and cannot be constituted as a legal advise, the author of this article and Lawcrux team is not responsible for any legal issues if arises on the basis of the interpretation given above.