GST Roadblocks: Procedure for Interception of Conveyance

With the introduction of the GST regime and the mandatory implementation of the e-way bill, there have been several instances where vehicles transporting goods are detained due to discrepancies in the documentation. This article seeks to outline the key sections and rules that authorize the interception and detention of vehicles, along with the penalties that can be levied on the owners of both the goods and the vehicle.

Section 68 of the CGST Act, 2017, along with Section 129 & 130, and Rule 138B of the CGST Rules, 2017, grants officers the authority to intercept vehicles, inspect goods, and detention, release and confiscation of such goods and conveyances. Specifically, Section 68 outlines the responsibilities of the person in charge of a conveyance carrying goods valued above a specified amount, requiring them to possess certain prescribed documents. If intercepted, the proper officer can request these documents for verification.

Rules 138 to 138D elaborate on e-way bill requirements, stating that the person in charge must carry the relevant invoice or delivery challan and a physical or electronic copy of the e-way bill. This bill can also be linked to a Radio Frequency Identification Device (RFID) on the conveyance.

Furthermore, Section 129 addresses the detention and release of goods in transit, while Section 130 covers confiscation and penalties for non-compliance.

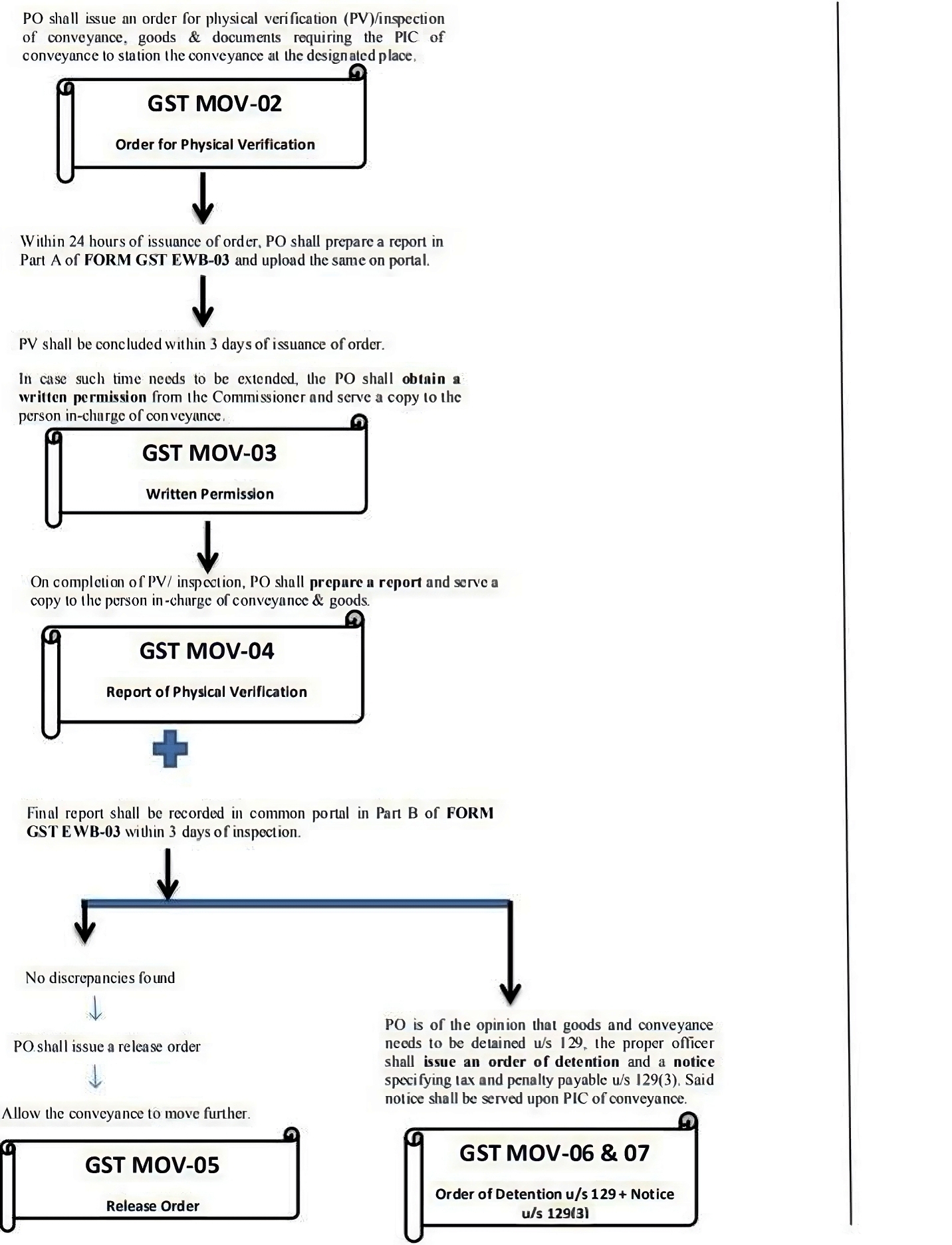

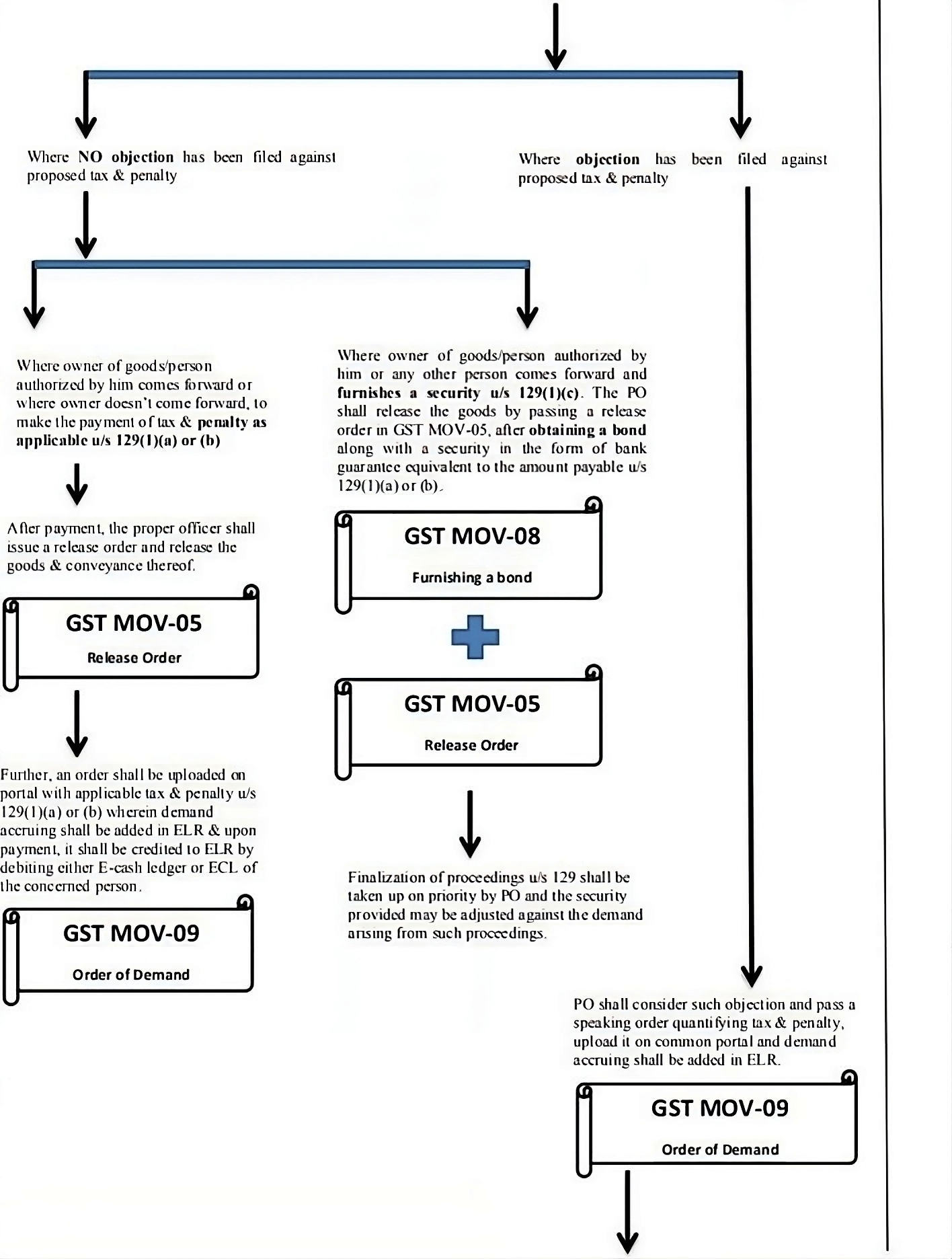

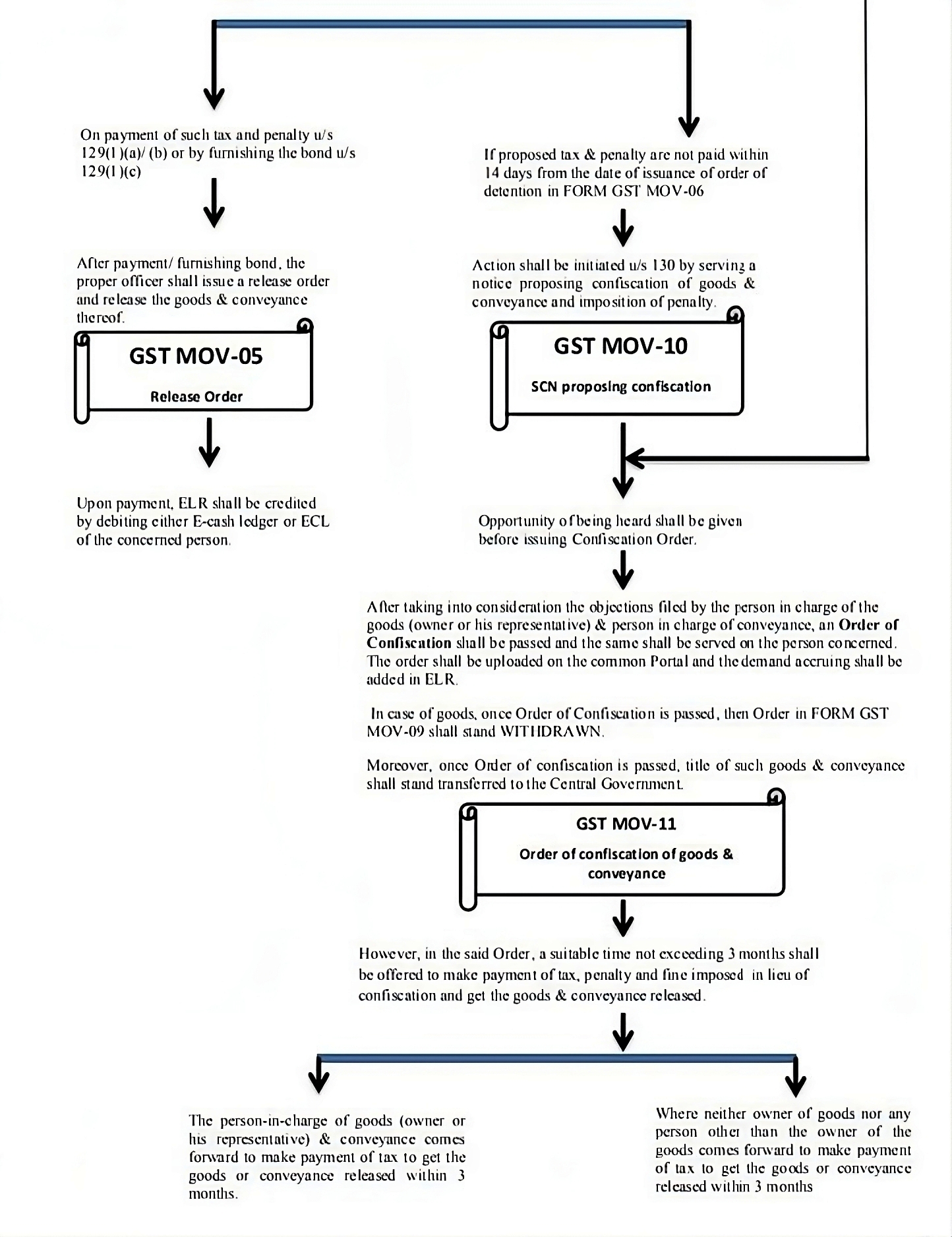

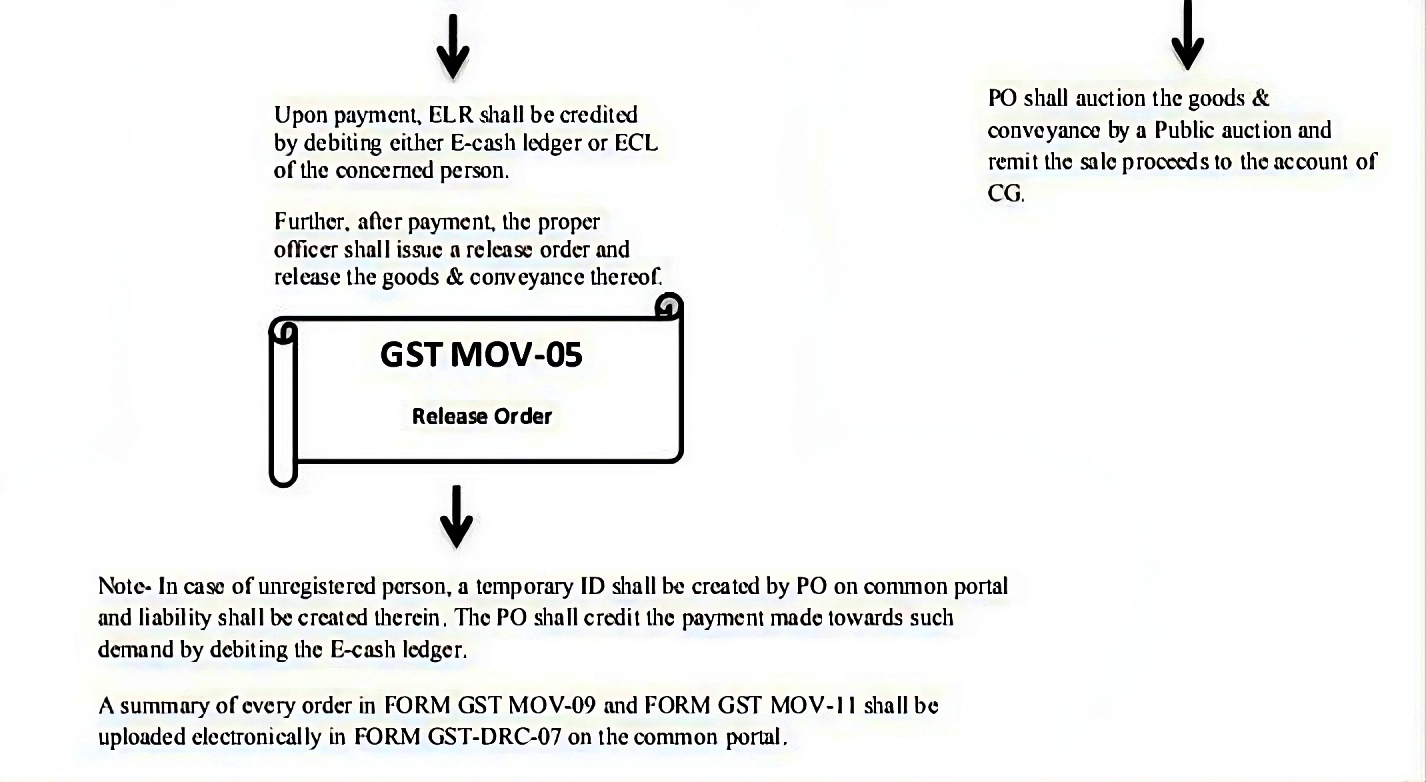

The subsequent procedures for interception or detention of goods or vehicles are outlined in Circular No. 41/15/2018, dated 13.04.2018, and are summarized below in a flow chart for ease of understanding.

|

|

|

|

|

|

|

|

|

|

In light of the strict penalty provisions outlined in Section 129 of the CGST Act 2017, the CBIC received multiple representations concerning the imposition of fines for minor inconsistencies in e-way bill details. Even when invoices accompanying the goods were accurate, penalties were still being enforced. Following a thorough review, the CBIC issued a Circular No. 64/38/2018-GST on September 14, 2018. This circular addresses minor technical and clerical errors related to e-way bills.

Paragraph 5 of Circular No. 64/38/2018-GST specifies that if a consignment is accompanied by an invoice or any other designated document along with an e-way bill, proceedings under Section 129 may not be initiated in certain situations, including:

(a) Spelling errors in the names

of the consignor or consignee, provided the GSTIN is accurate;

(b) Incorrect pin codes when the addresses of the consignor and consignee are

correct, as long as the error does not extend the e-way bill’s validity;

(c) Errors in the consignee’s address where the locality and other details are

accurate;

(d) Minor inaccuracies in one or two digits of the document number on the e-way

bill;

(e) Mistakes in the HSN code at the 4 or 6 digit level, provided the first two

digits and the tax rate are correct;

(f) Errors in one or two digits/characters of the vehicle number.

In conclusion, the GST regime, alongside the mandatory e-way bill system, has significantly transformed the transportation of goods, promoting compliance and reducing tax evasion. Circular No. 41/15/2018 outlines the procedures that officers must follow during the interception of conveyances, providing clarity for the person in charge. This guidance enables individuals to assess their situation effectively, decide whether to make a payment or pursue an appeal, and ensures they are not deprived of their rights. Additionally, taxpayers can evaluate whether the officer has followed the necessary steps and issued the correct FORM at the appropriate stage, empowering them to make informed decisions. Understanding these regulations and procedures are essential for businesses to navigate the complexities of GST compliance while safeguarding their interests and maintaining a smooth supply chain.

Disclaimer: The information given in this article is solely for purpose of understanding the law. It is completely based on the interpretation of the author and cannot be constituted as a legal advise, the author of this article and Lawcrux team is not responsible for any legal issues if arises on the basis of the interpretation given above.